Current Market Analysis

The analysis of markets is a critical part of the trading decisions of any trader or investor. The individual trader or trading group may have a preference for: Macroeconomic Analysis, Microeconomics Analysis, Fundamental Analysis, Behavioural Analysis, Quantitative Analysis and Technical Analysis. But whichever approach is employed, it is through this analysis that the trader decides:

- If to buy or sell an asset

- At which levels to enter a trade

- At which level to put the target to hopefully take profit on the trade

- Or, if the analysis proves incorrect, when and where is the trade wrong and at which level to exit the trade.

In this section we provide daily, real time market views including currency pairs forecasts, primarily through the approach of Technical Analysis, but also by utilising other approaches to market analysis. Many of our analyses also contains a video explaining the analyses. Click here for all video analyses and here for all forex news.

Global stock averages retreat with higher oil price and Fed rate cut worries

Macroeconomic/ geopolitical developments Global financial market developments Key this week Central Bank Watch: The most important central bank activities this week are the FOMC Minutes on Wednesday ECB Monetary Policy Decision and Statement on Thursday. We will also observe the RBNZ and BoC Interest Rate Decisions and Statements Wednesday. Macro Data Watch: Global CPI data … Continued

Stocks Stay Strong Ahead of PMI and US NFP Reports

Macroeconomic/ geopolitical developments Global financial market developments Key this week Central Bank Watch: No Central Bank activity of note, but we are watching for further indications for the path of future US interest rates from FOMC speakers. Macro Data Watch: Global PMI data is released through the week, with the US ISM PMI data of … Continued

Global Stocks Stay in Bull Mode as Global Central Banks Gear Up for Rate Cuts

Macroeconomic/ geopolitical developments Global financial market developments Key this week Central Bank Watch: No Central Bank activity of note, but we do get the Bank of Japan Monetary Policy meeting minutes on Monday. This should give further insight after last week’s interest rate hike. Plus, after last week’s Fed meeting we are watching for further … Continued

Warmer US Inflation Data Puts Focus on the Fed’s Dot Plot Chart This Week

Macroeconomic/ geopolitical developments Global financial market developments Key this week Central Bank Watch: A busy week for Central Banks highlighted by interest rate decisions from the BoJ and RBA Tuesday, the PBoC and FOMC Wednesday and the BoE Thursday. Macro Data Watch: Lots of data to be released this week with the focus being global … Continued

US Industrial Production and Michigan Consumer Sentiment Expectations – 15th March

What to expect from US Industrial Production data Scheduled for release at 14:15 GMT on Friday, March 15, the US Industrial Production data for February is highly anticipated by economists, policymakers, and investors. This report provides crucial insights into the performance and trends within the manufacturing, mining, and utility sectors, offering valuable indications of economic … Continued

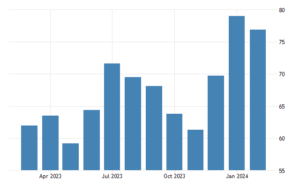

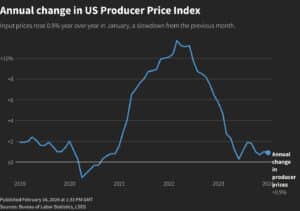

US PPI and Retail Sales Preview – 14th March

What to expect from US PPI data The upcoming US Producer Price Index (PPI) report, scheduled for release on Thursday, March 14th at 13:30 GMT, is poised to offer critical insights into inflationary pressures within the economy, particularly at the producer level. Analysts’ consensus estimates for February’s PPI report indicate expectations for modest inflationary growth. … Continued

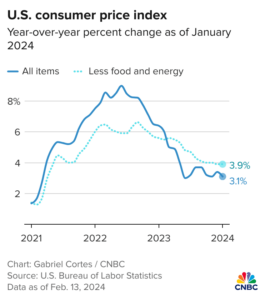

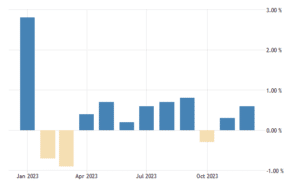

US CPI Report Preview – 12th March

What to Expect from the US CPI Report Scheduled for release on March 12th, 2024, at 12:30 GMT, the US Consumer Price Index (CPI) report for February is poised to attract significant attention from economists, policymakers, and investors alike. This report offers crucial insights into inflationary trends, guiding monetary policy decisions and shaping market expectations. … Continued

US Stock Averages Hit New Records, After Mixed Messages From Powell; US CPI In Focus This Week

Macroeconomic/ geopolitical developments Global financial market developments Key this week Central Bank Watch: Nothing of note from central banks this week, but as ever Fed speakers must be watched. Macro Data Watch: The standout data for the week will be US CPI on Tuesday, plus we also get the UK Employment report and German CPI … Continued

US Employment Report Preview – 8th March

What to Expect from the US Employment Report As anticipation builds for the release of the US Employment Report, economists and market analysts are closely scrutinising various indicators to gauge the health of the labour market and broader economy. Here’s what to expect from the upcoming report based on recent data and expert forecasts. Economists … Continued

UK Spring Budget 2024 Recap

The UK Spring Budget is a pivotal event in the nation’s fiscal calendar, where the Chancellor of the Exchequer outlines the government’s taxation and spending plans for the upcoming financial year. This annual presentation typically occurs in March and serves as a platform for the Chancellor to address Parliament and the public, detailing key economic … Continued

Fed’s Powell to Testify Before Congress

Current Climate: US Economy and Fed Speakers Outlook Federal Reserve officials have recently conveyed a cautious stance regarding the possibility of swift interest rate cuts, reflecting their assessment of the current state of the US economy. Governor Michelle Bowman, among others, emphasised the importance of maintaining the policy rate steady, citing potential risks to inflation … Continued

UK Budget Report Preview – 6th March

What to Expect from the UK Budget Report The UK Budget Report, scheduled for presentation by Treasury Chancellor Jeremy Hunt on Wednesday, 6th March at 12:30 GMT, is poised to address critical fiscal and economic matters impacting the nation. Traditionally, the Budget serves as a roadmap for the government’s financial plans for the upcoming fiscal … Continued

Nasdaq Hits Record High; Powell and US Employment in the Spotlight

Macroeconomic/ geopolitical developments Global financial market developments Key this week Central Bank Watch: A notable week for central banks, as we see the Bank of Canada (BoC) interest rate decision Wednesday, followed by the European Central Bank (ECB) Interest Rate decision, Statement: and Conference Thursday. Plus, an important focus will be as Fed Chair Jerome … Continued

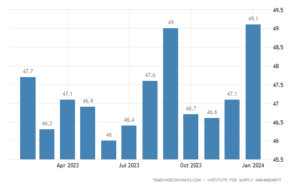

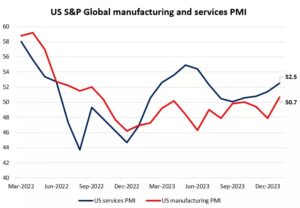

Global Manufacturing PMI Preview – 1st March

What to Expect from US PMI data The upcoming release of US PMI data is highly anticipated by analysts and investors, providing crucial insights into the performance of the manufacturing sector. S&P Global is set to release its Manufacturing PMI for February at 2:45 GMT, with expectations hovering around 51.5, matching the flash estimate reported … Continued

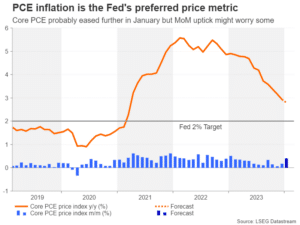

US PCE Preview – 29th February

What to Expect from the US PCE Data The upcoming US Personal Consumption Expenditures (PCE) data release, scheduled for 13:30 GMT on Thursday, February 29th, is expected to provide insights into the trajectory of inflation in the United States. Economists anticipate that the report will confirm January’s setback in the battle against rapid cost-of-living increases. … Continued

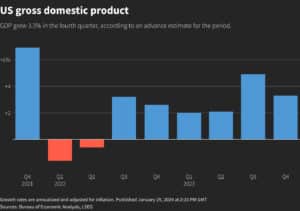

US GDP and EU Consumer Confidence Preview – 28th February

What to expect from the US GDP data The upcoming first revision of Q4 US GDP data, scheduled for Wednesday, February 28th at 13:30 GMT, is highly anticipated as it provides a comprehensive assessment of the nation’s economic performance during the fourth quarter. This data, released by the US Bureau of Economic Analysis, offers insights … Continued

US Durable Goods and Consumer Confidence Preview – 27th February

What to expect from the US Durable Goods data Investors and economists eagerly await the release of the US Durable Goods data, scheduled for 13:30 GMT on Tuesday, February 27th. The report by the US Census Bureau provides crucial insights into the health of the manufacturing sector and broader economic activity in the United States. … Continued

US and global stock averages hitting record levels, with Nvidia surging again

Macroeconomic/ geopolitical developments Global financial market developments Key this week Central Bank Watch: A very quiet week for central banks, but we do see the Reserve Bank of New Zealand interest rate decision Wednesday. Macro Data Watch: The focus this week will be on German Gfk Consumer Confidence, Retail Sales, Unemployment and CPI, US Durable … Continued

Global Manufacturing, Services and Flash PMI Preview – 22nd February

What to Expect from the US S&P Global PMI Releases As the U.S. S&P Global PMI releases approach, scheduled for 14:45 GMT on Thursday, February 22nd, 2024, analysts are anticipating crucial insights into the country’s economic performance. Consensus forecasts suggest a slight moderation in the S&P Global Services PMI for February, with expectations set at … Continued

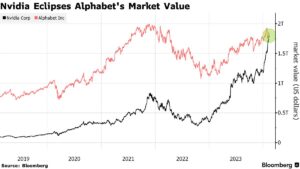

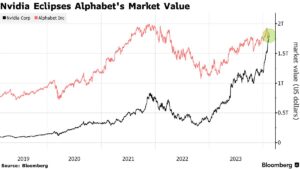

Nvidia Earnings Preview – 21st February 2024

What to expect from Nvidia’s Earnings Nvidia’s forthcoming Q4 2023 earnings call, scheduled for Wednesday, February 21st, 2024, is anticipated to be a pivotal event not only for the company itself but also for the broader technology landscape, particularly in the realm of artificial intelligence (AI). As the third most valuable company on Wall Street, … Continued

Walmart and Home Depot Earnings Preview – 20th February 2024

Why are Walmart’s Earnings so Important? Walmart, the world’s largest retailer by revenue, is a multinational retail corporation headquartered in Bentonville, Arkansas, USA. Founded in 1962 by Sam Walton, Walmart operates a chain of hypermarkets, discount department stores, and grocery stores across the globe. With a presence in 27 countries and e-commerce operations in 10 … Continued

Stocks rebound after sell off in the wake of warmer than expected US CPI data

Macroeconomic/ geopolitical developments Global financial market developments Key this week Holidays: As Asian markets return from the Lunar New Year holidays last week, the US President’s Day holiday is on Monday 19th February. Central Bank Watch: A relatively quiet week for central banks, but we do see the PBoC Interest Rate Decision Tuesday. Macro Data … Continued

NatWest 2023 Q4 Earnings Preview – 16th February 2024

What to Expect from NatWest’s Earnings Investors eagerly anticipate NatWest’s 2023 Q4 earnings call, scheduled for release on Friday, February 16th, 2024. With a market cap of £17.851B, the bank faces high expectations following its recent challenges and amidst significant market competition. In light of the forecasted Q4 EPS of £0.07 and revenue forecast of … Continued

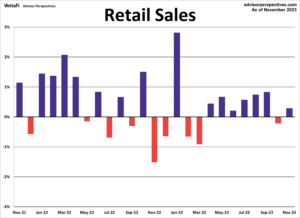

US and UK Retail Sales Previews – 15th and 16th February 2024

As investors gear up for the upcoming Retail Sales data releases in the United States and the United Kingdom on February 15th and 16th, respectively, anticipation is high for insights into consumer spending trends. These releases serve as vital economic indicators, offering a glimpse into the pulse of consumer activity and broader economic conditions. What … Continued

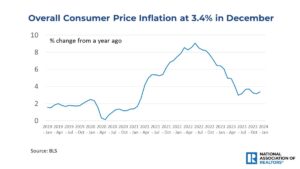

February 13th 2024 US CPI Release Preview

US CPI Expectations As anticipation builds for the upcoming release of the US Consumer Price Index (CPI) on February 13th, market participants are bracing for critical insights into the state of inflation. This data arrives amidst a backdrop of heightened attention following a robust January jobs report and the Federal Reserve‘s cautious stance on inflation. … Continued

Risk On! S&P 500 break 5000, US CPI in the spotlight this coming week

Macroeconomic/ geopolitical developments Global financial market developments Key this week Other Events: Chinese New Year is this week, so mainland Chinese markets and other Asian markets will be closed, so Asian sessions could be particularly quiet. Central Bank Watch: A quiet week for central banks, Fed speakers always in focus. Macro Data Watch: A busy … Continued

UK Earnings Preview – Thursday 8th February

Why are AstraZeneca’s Earnings so Important? AstraZeneca is a leading global biopharmaceutical company renowned for its innovative medicines in areas such as oncology, cardiovascular, respiratory, and immunology. As one of the largest pharmaceutical companies worldwide, AstraZeneca’s earnings releases are highly anticipated and closely monitored by investors, analysts, and healthcare professionals. These releases provide critical insights … Continued

UK Earnings Recap – Vodafone and BP

Why are Vodafone’s Earnings so Important? Vodafone Group Plc, commonly known as Vodafone, is a global telecommunications company headquartered in London, United Kingdom. With operations spanning across Europe, Africa, Asia, and Oceania, Vodafone is one of the world’s largest telecommunications providers, offering mobile and fixed-line services, broadband, and digital television. The company’s earnings releases hold … Continued

Weekly US Earnings Outlook from February 6th 2024

The US 2023 fourth-quarter earnings season is in full swing, with 230 S&P 500 companies already reporting. Impressively, 80% of these companies have exceeded Wall Street’s expectations, as reported by LSEG. Last week was extremely busy, seeing the likes of Microsoft and Alphabet earnings Tuesday and Amazon, Apple and Meta reporting Thursday. This week will … Continued

Record Highs Again for US Stock Averages, Despite Fading March Rates Cut Hopes

Macroeconomic/ geopolitical developments Global financial market developments Key this week Central Bank Watch: A quiet week for central banks, with the Reserve Bank of Australia (RBA) Tuesday, plus as always, a focus on Fed speakers. Macro Data Watch: Also, a quiet week for data. The focus for the week will be Monday’s Services and Composite … Continued

Apple and Amazon Earnings Update – February 1st 2024

Updated 02/02/2024: Apple’s 2023 Q4 earnings call, unveiled on February 1st, 2024, showcased the tech giant’s financial prowess, with figures that slightly outperformed expectations. The reported earnings per share (EPS) stood at $2.18, surpassing the forecasted $2.1. The revenue for the quarter reached a remarkable $119.58 billion, exceeding the anticipated $118.06 billion. These robust financial … Continued

US Employment Data Preview – February 2nd 2024

What is the US Employment Report? The US Employment Report, a monthly release from the US Bureau of Labor Statistics (BLS), serves as an essential economic compass, offering in-depth perspectives on the dynamics of the nation’s labour market. This comprehensive report comprises several critical metrics, prominently featuring nonfarm payrolls, unemployment rates, and average hourly earnings. … Continued

Microsoft and Alphabet Earnings – January 30th 2024

Update 31/01/2024: Microsoft’s 2023 Q4 earnings call, released on January 30th, 2024, showcased a robust financial performance for the tech giant. According to data from investing.com, Microsoft reported an earnings per share (EPS) of $2.93, surpassing the forecasted EPS of $2.78. The company’s revenue for the quarter reached $62 billion, slightly exceeding the predicted revenue … Continued

Fed Interest Rate Decision Preview – 31st January

The Federal Reserve (Fed) Interest Rate Decision is a pivotal event in global financial markets, representing the central bank’s determination of the target range for the federal funds rate. This rate influences the cost of borrowing and lending throughout the economy, impacting various sectors, including consumer spending, business investment, and financial markets. The Fed typically … Continued

January Recap and a Heads Up for March

The Inflation Deflation and Economic Cycle Model measures the liquidity impulse from fiscal and monetary policies. This is how we determine what will occur with the ROC of inflation and economic growth. The current liquidity factors that must be measured are the Treasury General Account (TGA), Reverse Repurchase Agreement (RRP), Fed’s balance sheet, Federal Funds … Continued

“Risk On” Theme Extends, US Averages at Record Levels into a BIG Week

Macroeconomic/ geopolitical developments Global financial market developments Key this week Central Bank Watch: A significant week for central banks with monetary policy decisions on Wednesday from the Fed and on Thursday from the Bank of England (BoE). Macro Data Watch: Standouts this week are EU GDP (YoY, QoQ) on Tuesday, Japan Retail Trade and Sales … Continued

Caterpillar Earnings and US PCE Data Previews – 26th January 2024

Caterpillar Earnings Caterpillar Inc., a global leader in manufacturing construction and mining equipment, engines, and industrial gas turbines, holds significant importance in the financial landscape. Renowned for its iconic yellow machinery, Caterpillar is a key player in the machinery and equipment sector, providing essential tools for construction, resource extraction, and infrastructure development worldwide. Why are … Continued

ECB Monetary Policy Statement Preview – 25th January 2024

What is the European Central Bank? The European Central Bank (ECB) is the central banking authority responsible for formulating and implementing monetary policy within the Eurozone. Established in 1998 and headquartered in Frankfurt, Germany, the ECB plays a pivotal role in maintaining price stability and supporting sustainable economic growth across the member countries that share … Continued

24th January US Earnings Preview

In the ever-evolving landscape of financial markets, corporate earnings releases stand as pivotal moments, offering investors and analysts a lens into the financial health and strategic trajectories of major companies. Today, we continue to cover the ongoing US Earnings releases, having given a preview on 23rd January releases. This article will delve into the anticipated … Continued

23rd January US Earnings Preview

An earnings release, a critical financial document, is issued quarterly by publicly traded companies to disclose financial performance. Mandated by regulatory authorities like the SEC, it includes income statements, balance sheets, and cash flow statements. This report communicates a company’s financial health, operational achievements, and future outlook to investors and analysts. Investors analyse it closely … Continued

Stocks March Higher, Despite Fading Hopes of a Fed March Rate Cut

Macroeconomic/ geopolitical developments Global financial market developments Key this week Central Bank Watch: Although the Fed have entered their blackout period, a bust week elsewhere for Central Banks, as we get interest rate decisions from the People’s Bank of China (PBoC) Monday, the Bank of Japan (BoJ) on Tuesday, the Bank of Canada (BoC) on … Continued

Fed Enters Blackout Period – What and When is it?

What is a Fed Blackout Period The Federal Reserve, as the central banking system of the United States, plays a crucial role in shaping monetary policy and influencing economic conditions. The Fed’s communication is closely monitored by financial markets, and one notable aspect of this communication strategy is the “Fed blackout period.” A Fed blackout … Continued

Apple And TSMC Drive Tech Stocks Higher

TSMC Stocks Surge, with Positive 2024 Outlook due to Continued Apple Collaboration and AI Boom Who are TSMC? Taiwan Semiconductor Manufacturing Company (TSMC) stands as a global giant in the semiconductor industry, boasting a market capitalization of 486.28 billion and commanding a pivotal role in the manufacturing landscape. Established in 1987, TSMC has evolved into … Continued

US Earnings Release Preview – Friday 19th January

As we approach Friday January 19th the first full week of the US Q4 earnings season comes to a close. Investors are preparing for a flurry of corporate earnings releases that will provide key insights into the financial health of major companies. Among the notable players scheduled to announce their earnings on Friday are; Schlumberger, … Continued

US Retail Sales and US Industrial Production Releases – 17th January 2024 Preview

What are US Retail Sales US Retail Sales data releases are economic indicators that measure the total receipts of retail stores, providing a comprehensive snapshot of consumer spending on goods. These releases encompass a wide range of retail categories, including clothing, electronics, groceries, and other consumer products. The data is collected and reported by the … Continued

Earnings Releases and Macro Data Preview – January 16th

Earnings Releases Earnings releases from investment banks like Goldman Sachs and Morgan Stanley are vital for financial markets, serving as key indicators of the financial industry’s health, risk management, and overall economic conditions. These reports influence market sentiment, guide investment decisions, and provide insights into the banks’ adaptability to changing economic environments. There were multiple … Continued

Stock Averages Post Strong Rebounds, Despite Warm CPI and Middle Eastern tensions

Macroeconomic/ geopolitical developments Global financial market developments Key this week Central Bank Watch: Nothing of note from Central banks this coming week, but as ever we will be watching Fed speakers in the final week before they enter their blackout period. Macro Data Watch: The World Economic Forum in Davos runs all week from 15th-19th … Continued

US Q4 Earnings Begin – January 12th Financials Focus

Friday signalled a pivotal juncture with the kick off of the US Earnings Season, as notable companies disclosed their performance metrics. Investors, analysts, and market enthusiasts carefully analysed the data to inform their trading decisions and try to trade the news. This examination zeroes in on the releases from financial corporations that initiated the Q4 … Continued

US Q4 Earnings Season Kicks Off in Earnest

The stage is set, and the curtains are about to rise on the much-anticipated spectacle in the world of finance – the Q4 2023 US Earnings Season. These unique financial reports reveal valuable data that can send shockwaves through the markets and shape the investment landscape. Investors can trade the news to capitalise on profitable … Continued

January 11th US CPI Release Preview

What is the US CPI? The US Consumer Price Index (CPI) tracks the average change in prices paid by urban consumers for a variety of goods and services. It’s a dynamic basket that includes your morning coffee, the rent for your urban sanctuary, the cost of a new gadget, and even the indulgence of a … Continued

European Data Releases Review – January 9th

German Industrial Production Worse Than Expected Why is German Industrial Production Data Important? In the financial world, the German industrial production data is more than numbers; it’s the heartbeat of Europe’s economic engine. Here’s why it’s a focal point for trading economic news: Eurozone Foundation: Germany, the Eurozone’s economic powerhouse, lays the foundation. The data … Continued

Stocks and Bonds Plunge to Start 2024

Macroeconomic/ geopolitical developments Global financial market developments Key this week Central Bank Watch: No central bank activity of note, but as usual watching for Fed speakers. Macro Data Watch: US CPI on Thursday is the standout in a relatively light data week. Date Major Macro Data 01/08/2024 Eurozone Retail Sales (YoY & MoM) and Consumer … Continued

2024 Outlook

This year promises to be one of the most interesting years economically, politically, and market-wise in history. We have two significant global conflicts/wars ongoing, just as President Xi of China is reiterating his promise to annex Taiwan, and Kim Jong Un of North Korea threatens to wipe the US off the map. Meanwhile, we have … Continued

US Employment Report in the Spotlight – 5th January Preview

The US Employment Report and Why it Matters When looking at financial markets, few indicators carry the weight and influence of the US Employment Report. Released monthly by the Bureau of Labor Statistics, this comprehensive report provides a snapshot of the nation’s employment landscape, offering crucial insights into the health and direction of the economy. … Continued

Fed Minutes, Global S&P Global PMI and US ADP Employment Recap – 4th January 2024

Fed Minutes Recap: Uncertainty and Soft Landing Caution The recently released Fed minutes from the Dec. 12-13 meeting reveal a nuanced landscape of uncertainty among policymakers. Some express concerns about prolonged high rates, fearing a sudden job market downturn, while others advocate for a steady target rate. Richmond Fed President Tom Barkin, set to join … Continued

Fed Minutes Preview: 3rd January 2024

What Are The Fed Minutes? The Federal Reserve, often just called “the Fed,” is the gatekeeper of the U.S. economy. They act as the controlling force, pulling levers to control interest rates and monetary policy. Now, the Fed doesn’t operate in complete secrecy; it spills the beans through what we call “Fed Minutes.” Fed Minutes … Continued

DJIA Hits All Time High After Fed Dovish Pivot

Macroeconomic/ geopolitical developments Global financial market developments Key this week Central Bank Watch: A quieter week for Central Banks, we get the Reserve Bank of Australia (RBA) Meeting Minutes and Bank of Japan (BoJ) Monetary Policy decision, statement and conference on Tuesday, then the People’s Bank of China (PBoC) Interest Rate Decision Wednesday. Macro Data … Continued

S&P 500 hits 2023 High Ahead of US CPI and Four Major Central Bank Meetings

Macroeconomic/ geopolitical developments Global financial market developments Key this week Central Bank Watch: Four major central banks in play this week, with the main focus on the Fed decision Wednesday, then we get decisions from the Swiss National Bank (SNB), the Bank of England (BoE) and the European Central Bank (ECB) all on Thursday. Macro … Continued

Fed Speakers Dovish Pivot, Short-End Yields Plunge, Stocks Gain

Macroeconomic/ geopolitical developments Global financial market developments Key this week Date Major Macro Data 12/04/2023 Nothing of note 12/05/2023 Australia RBA Interest Rate Decision; global S&P Global Services and Composite PMI, US ISM Services PMI 12/06/2023 Australian GDP; EU Retail Sales; BoC Interest Rate Decision and Statement; US ADP Employment Change 12/07/2023 China Trade Balance; … Continued

Quiet Thanksgiving Week. GDP, PCE, PMI and Powell Now in Focus

Macroeconomic/ geopolitical developments Global financial market developments Key this week Date Major Macro Data 11/27/2023 Nothing of note 11/28/2023 RBNZ interest rate decision, statement and press conference 11/29/2023 EU Consumer Confidence; German CPI; US GDP and PCE (QoQ) 11/30/2023 Chinese PMI; German Retail Sales; German Unemployment; EU CPI; US PCE (MoM and YoY); Canadian GDP; … Continued

US and UK inflation beat expectations => Risk On extends

US and UK inflation beat expectations => Risk On extends Macroeconomic/ geopolitical developments Global financial market developments Key this week Date Major Macro Data 11/20/2023 PBoC Interest Rate decision 11/21/2023 RBA Meeting Minutes; Canada CPI; US FOMC Meeting Minutes 11/22/2023 US Durable Goods; Michigan Consumer Sentiment 11/23/2023 US Thanksgiving holiday; global Flash PMI from S&P … Continued

Stocks Surge, Despite Hawkish Powell Tone

Macroeconomic/ geopolitical developments Global financial market developments Key this week Central Bank Watch: A very quiet week for CB with nothing of note apart from the US Fed speakers to stay in focus. Macro Data Watch: An important week for data with CPI data releases from the US (Tuesday), UK (Wednesday) and the EU (Friday), … Continued

Labor Market Starting to Crack

So far this year, companies have planned 604,514 job cuts, a 198% increase from the 209,495 cuts announced through September 2022. It is the highest January-September total since 2020 when 2,082,262 cuts were recorded. Apart from that COVID year it is the highest January to September total since 2009. The real story behind the labor … Continued

Stocks Rebound with Yields Down, After Slightly More Upbeat Fed

Macroeconomic/ geopolitical developments Global financial market developments Key this week General: US Daylight Saving Time ended at the weekend, so the time difference between the US and the rest of the planet is back to normal in most cases Central Bank Watch: A relatively quiet week for CBs, we get Bank of Japan (BoJ) Meeting … Continued

If Even Unilever’s Out Is This The End For Corporate ESG?

It’s possible to think that corporate ESG – environmental, social and governance – investing is a thoroughly good idea. Which is how fashionable society seems to see it right now. It’s also possible to think that corporate ESG is merely a passing fad and an expression of the agency problem – precisely because fashionable society … Continued

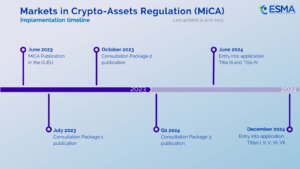

What MiCA is and What It Means for Crypto

The Markets in Crypto Assets is the EU’s regulatory framework for cryptocurrencies and digital assets. Through it, the European Union aims to centralize regulations governing the issuance and sale of digital assets, including bitcoin and various other cryptocurrencies. In addition to replacing a patchwork of national crypto regulations, MiCA will also clarify the playing field … Continued

CAB Payments – Don’t Trust IPOs From Private Equity Perhaps? Or Just West Africa?

CAB Payments was an IPO on the London market back only this summer. It’s also imploded already. Which is pretty good and matches the very worst performances from some of the Nasdaq despac operations. And IPO is supposed to be very much more verified than a Spac so this isn’t a grand advertisement for participating … Continued

Stocks Down, with Yields Up Again, after Mixed Data and Earnings

Macroeconomic/ geopolitical developments Global financial market developments Key this week General: UK and EU Daylight Saving Time ended at the weekend, so for this week there is only a 4-hour time difference between London and New York. Daylight Saving Time ends in the US next weekend, 4/5 November. Central Bank Watch: The Bank of Japan … Continued

Albemarle Drops Liontown Bid, The Bloom’s Truly Off The Lithium Boom

It is indeed true that Gina Rinehart has built a 20% position in Liontown Resources (ASX: LTR) and she’s long been known as a very canny strategic player in the metals business. But that’s not to say that she – or anyone else – is always right in this space. It’s equally possible to believe … Continued

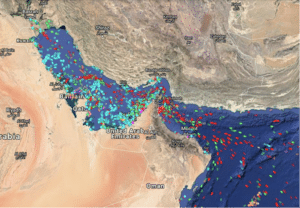

The Strait of Hormuz: everything you need to know

According to the US Energy Information Administration, the Strait of Hormuz is the world’s most important oil chokepoint. Here’s why. You will probably hear a lot about the Strait of Hormuz over the next few weeks, so I thought it would help to lay out the basics here. To start with, let’s consider Brent Crude … Continued

Rising interest rates kill the economics of renewables – Enphase and SolarEdge edition

The price of SolarEdge (NASDAQ: SEDG) dropped 27% in one day last week. That of Enphase (NASDAQ: ENPH) followed within minutes by falling 15%. The two companies are not directly related, they’re not – at least not particularly – supplier and customer, or partners. They are in the same sector though. Which is the thing … Continued

Optimizing Investment Strategies: A Guide into Fundamental and Technical Analysis Approaches

Investing in the financial markets requires careful analysis of stocks and securities in order to make informed decisions that will yield profitable results and the two main analysis methods used by investors are fundamental and technical analysis. Fundamental analysis focuses on a company’s intrinsic value, financial and growth outlook, on the other hand, technical analysis … Continued

Yields Surge Again, Stocks Down

Macroeconomic/ geopolitical developments Global financial market developments Key this week Central Bank Watch: The Fed is in its blackout period ahead of the November 1st interest rate decision. We get the Bank of Canada (BoC) and European Central Bank (ECB) interest rate decisions, statements and press conferences on Wednesday and Thursday respectively. Macroeconomic data Watch: … Continued

Novo Nordisk’s Semaglutide Just Killed The Dialysis Market – Or Did It?

Novo Nordisk (NYSE: NVO) just stopped a set of tests for semaglutide, their wonder drug. The share prices of the kidney dialysis companies all dropped 20% within hours. The big question is whether this is the right reaction, too much or too little? It’s entirely possible to argue any of those three cases but the … Continued

The SEC is Changing Short Selling Rules – Makes Darn Little Difference

The Securities and Exchange Commission over in the US has decided that short selling is one of these nefarious attacks upon the integrity of the markets. At least that’s the usual Democratic Party response to the very idea of short selling. Which is, as we all know, selling something now in the hope of being … Continued

Volatility Reigns With Heightened Geopolitical Tensions

Macroeconomic/ geopolitical developments Global financial market developments Key this week Central Bank Watch: A quiet week for central banks, though we do get Fed speakers through the week, which is the last week before the Fed speaker blackout period ahead of the early November FOMC Meeting. We get Reserve Bank of Australia (RBA) Meeting Minutes … Continued

Bond Market Chaos to Increase by March 2024

The major issue with the bond market right now is the overwhelming amount of bond issuance combined with the notable absence of the usual buyers. In other words, the illiquidity is already causing U.S. sovereign debt to trade like a microcap penny stock. This dysfunctional trading environment should become exponentially worse by the end of … Continued

Always hire an ugly fund manager – they’ll make you more money

The art of investing is the art of gaining an edge. We’re all aware – well, we all should be aware – that the gaining of a half a percent here, a full percentage point there, makes all the difference to the long-term outcome of a portfolio. This is why ESG investing may well not … Continued

Isn’t Diversification Good? Lithium Americas and Lithium Americas Argentina Split, But Why?

It’s a standard outcome of the standard investing theories that diversification is good. On the fairly obvious grounds that spreading your risks is a good thing to be doing. Yes, yes, this idea really is the killer and yet there’s always that possibility that something will come up to kill it. So, not all eggs … Continued