GENinCode’s share price may have risen sharply, but the long-term prospects for the biotech stock could leave it undervalued even now.

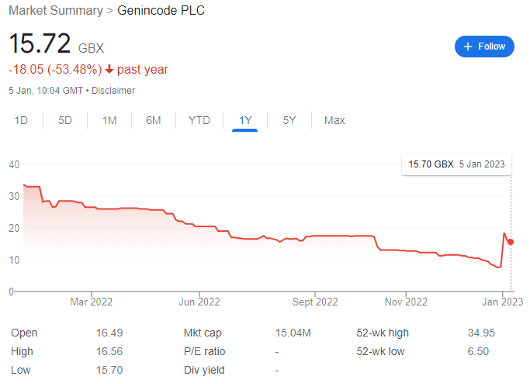

GENinCode (LON: GENI) launched its IPO near the height of the growth stock bubble in July 2021, pricing shares at 44p apiece. Raising £15.3 million net cash, the company began public life with a market cap of £42.2 million — but saw its share price diminish to 7.5p by 29 December 2022 as confidence exited the market.

However, the FTSE AIM share rocketed by 180% to 21p per share during intra-day trading on 3 January, before correcting to 15.7p today.

For context, this simply brings the biotech company back to the same valuation as in mid-October 2022; but its prospects are vastly improved by recent developments and a high-risk opportunity may now be presenting itself.

GENinCode shares: science in brief

GENinCode is a specialist in risk assessment and prediction of cardiovascular disease (CVD) and familial hypercholesterolemia. CVD covers a variety of diseases from mild angina to heart attacks, to stroke and hypertension.

Importantly, it’s the leading cause of death and disability worldwide accounting for 25% of deaths in the US in any given year, 31% of deaths worldwide, and is expected to cost the global economy over $1 trillion annually by 2030. It’s not hard to see where medical advances could be converted to profits.

GENI operates within the personalised medicine space, providing advanced genomic technology to help clinician decision-making. The sector has seen incredible advances in recent years- as an example (not GENI) many will remember reading last month about a girl with previously incurable leukemia being treated with base edited T-cells to cure her cancer.

GENinCode’s portfolio includes four key products.

Cardio inCode is a personalised medicine genetic test that measures the risk of a patient suffering a cardiovascular event by combing genetic factors with traditional risk factors, and which then proposes recommendations to reduce any risks.

Lipid inCode is a diagnostic test which analyses the genes associated with familial hypercholesterolemia and helps to provide a definitive diagnosis in what has been a difficult to diagnose disease in the past. Similarly, Thrombo inCode helps to diagnose thrombophilia, analyses the risk of developing thrombosis, and proposes treatment and prevention measures.

Finally, Sudd inCode analyses several genes associated with sudden cardiac death to check for variants responsible for genetic heart disease. The company has also developed an online reporting system — SITAB — which integrates clinical and genetic data for review by healthcare practitioners.

Recent developments

The most recent available financial figures for GENI were for H1 2022, where GENinCode grew revenues by 11% to £700,000, while its adjusted EDITBA loss more than doubled to £2.3 million. However, this increased loss reflects the rising investment in its portfolio development. And it retains £12.4 million in cash from the IPO, leaving it with a fair cash runway.

The company has already conducted the first Cardio inCode pilot implementation study in Spain and commissioned a new UK lab operation and UKAS accreditation submission for Lipid inCode to support NHS implementation. And it’s acquired Abcodia Ltd, including the rights to its Risk Assessment of Ovarian Cancer Algorithm (ROCA) test, marking GENI’s first step into the oncology space.

But its recent share price spike was caused by news on 3 January of the California state licensing approval and CLIA certification of its Irvine laboratory, enabling the provision of its products for the risk assessment of CVD to patients across almost every state in the United States.

The ‘major milestone in the commercialisation’ of the Cardo inCode and Lipid inCode products means that GENI can now expect to generate revenue in the US starting this year. Indeed, CEO Matthew Walls has hailed the ‘tremendous work effort to deliver these approvals representing a major advance in the Company’s commercial programme.’

At 15.7p, a fundamental share price re-rate could be on the cards. However, I consider two steps to be critical for this to happen. The first could be a US listing on the NASDAQ, and it would be surprising if this option were not being discussed despite the weak IPO environment and out-of-favour atmosphere for biotechs.

The second is full FDA approval, which is not a short process — and could take until 2025 based on standard timeframes (though given the state licensing there is a huge amount of leeway here). There’s also a reasonable chance of a buyout, given the war chests held by both private equity and blue-chip pharma companies. This makes timing an entry point on GENI complex as the share price drifts downwards again.

Of course, this is a very brief rundown of a lesser-known biotech stock. However, at 15.7p per share the company looks undervalued as a speculative investment, given the potential of its CVD tech and size of the potential target market.

But volatility is likely in the near term as the market catches up to GENI’s true value.

This article has been prepared for information purposes only by Charles Archer. It does not constitute advice, and no party accepts any liability for either accuracy or for investing decisions made using the information provided.

Further, it is not intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.