Investing In Exchange Traded Funds

What is an Exchange Traded Fund?

An Exchange Traded Fund or “ETF”, provides a vehicle for an investor to gain exposure to a wide range of instruments i.e. bonds, stocks or commodities etc in a single package.

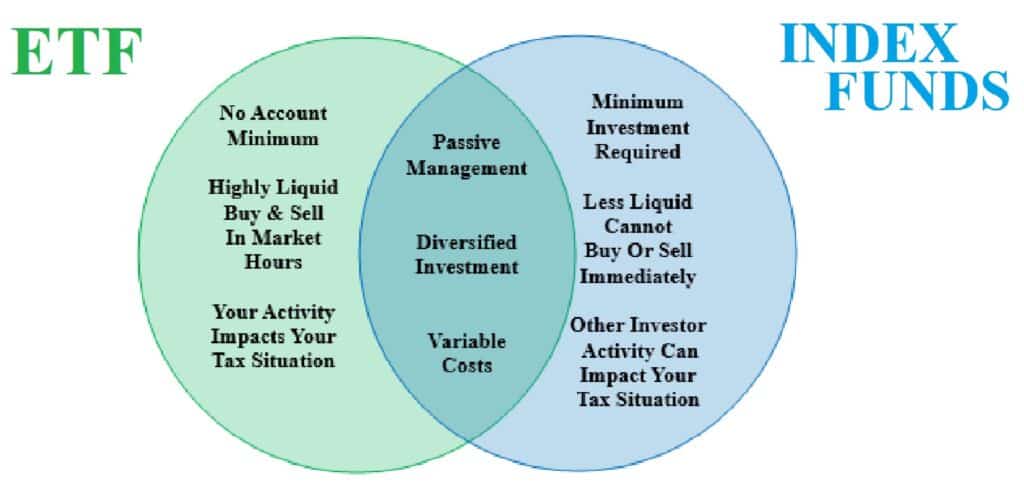

Given they are designed to track a specific underlying benchmark they are in some respects similar to index funds. The differences are seen in he way they are traded, and the fees involved.

Trading:

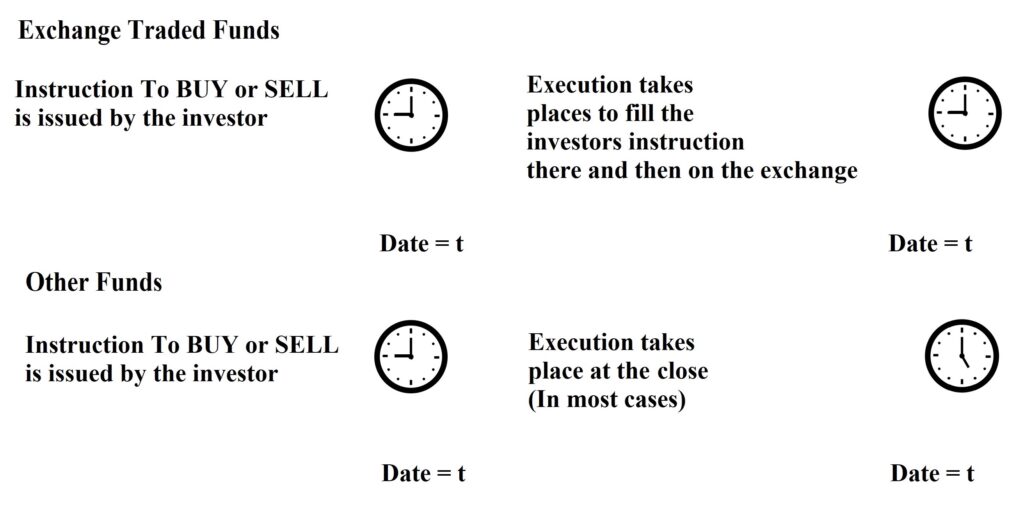

ETFs are traded on the stock market, (hence the name), which is not the case for other funds. The implication of that is one can buy or sell them at any time during the trading hours of the exchange.

In contrast, most other funds will only trade once a day and that trade window may not coincide with when one has submitted a trade instruction, see Figure 1.

The Fees & Other Costs

In most cases an ETF is cheaper to operate than other standard or generic funds. Like most things in life, that is not always the case, there are exceptions, so consideration of all pertinent costs on similar instruments should be made before a decision to invest is taken. However, in the main, the differences between the products provide ETFs with a cost advantage over mutual funds.

Why so? Mutual funds carry charges that are a combination of transparent and hidden costs that can start to sum to a large amount. It is based around the structuring and mutual fund managers will argue that the costs are necessary to cover their processing charges.

These funds will charge their investors for every single operating process, e.g., transaction fees or “load”, distribution charges as well as transfer costs. There is also an annual bill to be paid for capital gains.

One can see then that the fact that the investor is presented with a series of charges it implies the return on their investment will be diminished. Some managers will even impose an upfront fee for the privilege of having them manage one’s money! Please do not assume that ETFs are cost free. They also carry transparent and hidden fees, however, there are less of them. In addition, ETFs provide greater trading opportunity and are considered to be more transparent and tax efficient.

What Is The Load?

A “Load Mutual Fund” charges a sales charge or commission for the shares that are purchased. This can be expressed as a percentage of the amount one is investing or a flat fee. It will vary between providers.

Loads for mutual funds vary from 1% to 2%, and most of these are sold through brokers.

Financial advisors have their professional expertise rewarded in one of two ways:

- Commission

- By an annual percentage of one’s entire portfolio, usually between 0.5% and 2%.

If you don’t pay an annual fee, the load is the commission the financial advisor receives and should your broker gets paid by the load they may well not recommend ETFs for your portfolio because the commission that brokers receive for buying ETFs is less than the load.

ETF Costs

ETFs are traded directly on an exchange and as such can be subject to brokerage commissions; these can vary from one provider to another.

Naturally, the absence of a load fee is an advantage, however, keep an eye on brokerage fees. These may become substantial if an investor deposits small amounts of capital with a regular frequency. This may be the case if the investor is looking to build a certain exposure at say the average cost of the stock over three-months. This will involve frequent transactions and hence, incur costly brokerage fees.

It is good that ETFs expense ratios tend to be lower than mutual funds…especially cf. actively managed mutual funds. They will want to make a charge for the time spent on research and trying to achieve the optimum market timing.

Another advantage is the ETFs do not carry annual marketing fee called a “12b-1 fee”, named after a section of the 1940 Investment Company Act. For Index or Mutual Funds that can be as high as 0.25% in a front-end load fund and as high as 1% in a back-end load fund. In essence, it is another version of a broker’s commission.

Morningstar, a leading provider of independent investment research reported on July 12, 2022

“…Intensifying competition among asset managers and changes in

the economics of advice are two factors driving fees lower, …”

The asset-weighted average expense ratio for active funds fell to 0.60% in 2021 and for ETFs it was just 0.40%. Additional fees were found on “ESG” funds i.e., a “greenium” relative to investors in conventional funds. This is evidenced by these funds’ higher asset-weighted average expense ratio, which stood at 0.55% at the end of 2021.

ETF’s…Assets Under Management

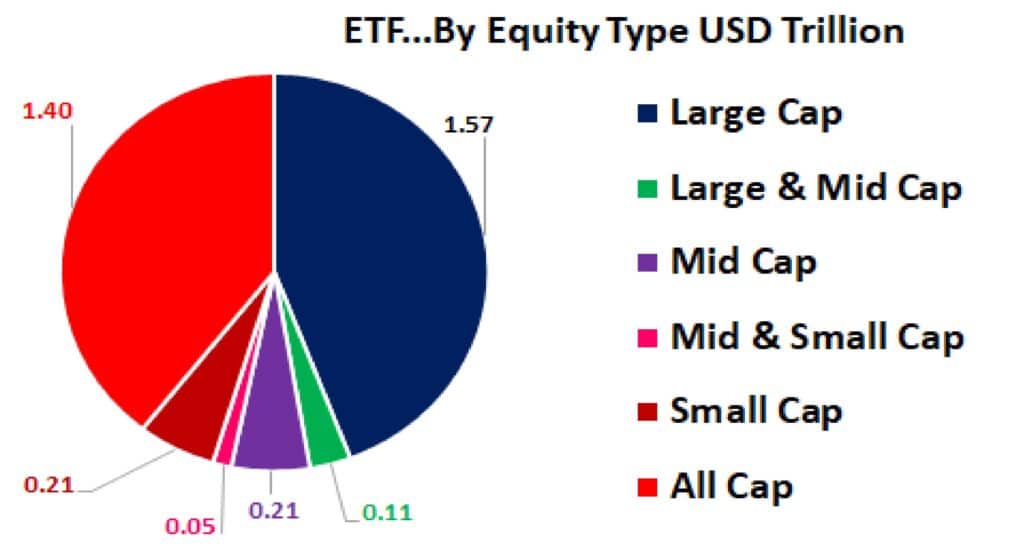

Blackrock has reported that the ETF universe has USD 5.75 Trillion in assets under management (AUM), that can give exposure to almost every asset class available. (Figure 3)

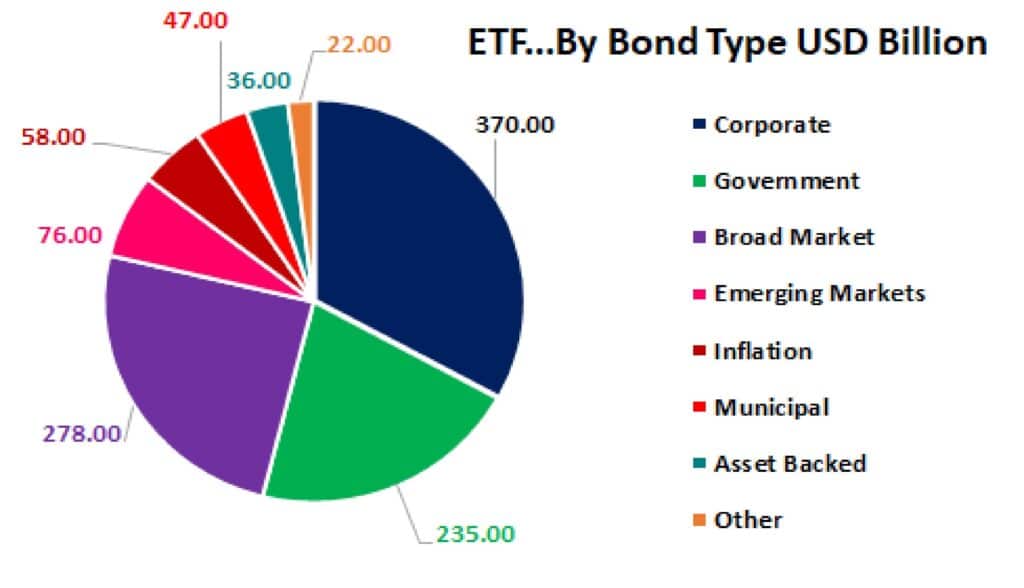

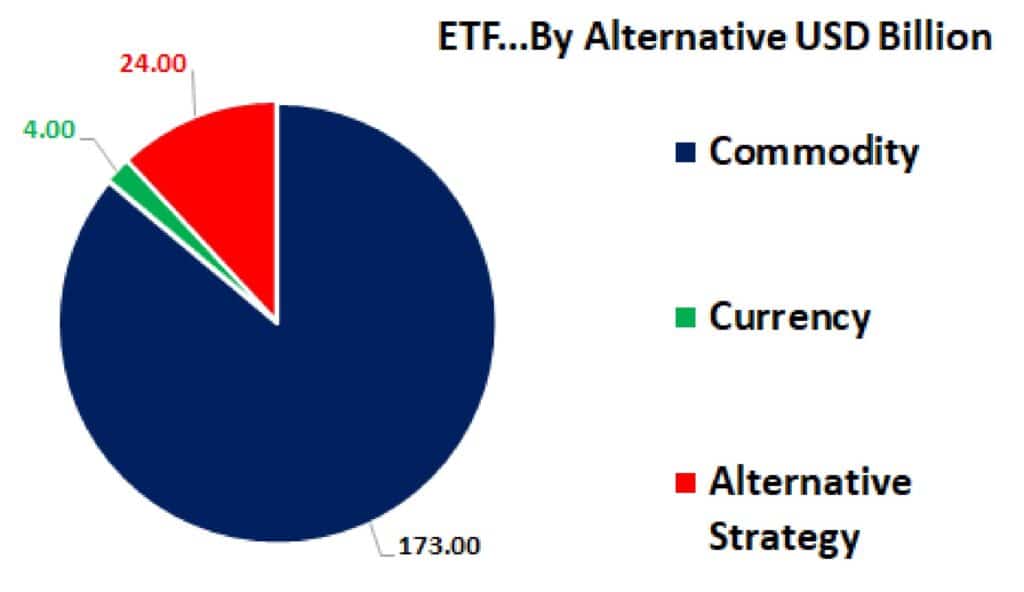

Equities are by far the largest world in the ETF universe at USD 4.4 Trillion making up 76.4% of all assets, however the fastest expanding areas are Fixed-Income bond ETFs that now stands at USD 1.12 Trillion, Figure 4 and Alternatives at USD 201 Billion.

Within the sectors shown in Figure 5 one finds the following sub-groups:

Commodities:

Energy: Biofuels, Carbon, Crude Oil, Gasoline, Heating Oil and Natural Gas

Metals: Aluminium, Copper, Gold, Iron, Lead, Palladium, Platinum, Silver, Tin, Uranium and Zinc

Agriculture: Cocoa, Coffee, Corn, Cotton, Lean Hogs, Live Cattle, Rice, Soya Beans, Sugar and Wheat

Currency:

Developed and Emerging Market, Broad Market, Crypto, AUD, CHF, EUR, GBP, INR, ILS, JPY, KRW, MEX, NZD, NOK, RUB, SAR, SGD, SEK and USD

Alternative

Strategy: Broad Market, Buy Write (a), Equity Long/Short, Global Macro, Merger & Arbitrage,

Multi Asset, Private Equity, Target Date (b), Target Risk (c), Volatility

- The Buy Write is an options investment strategy in which an investor simultaneously buys shares and writes a call option contract over an equivalent number of shares

- Target-date funds are structured to maximise returns by a specific date. Funds are designed to build gains in the early years by focusing on riskier growth stocks, then they aim to retain those gains by weighting towards safer, more conservative choices as the target date approaches

- Target-risk funds establish and maintain a specific level of risk exposure in its portfolio over time. These are often labelled from “conservative” to “aggressive” risk exposure. The investor chooses the risk profile that best suits their risk/return appetite.

EFT Growth & Trends

ETFs have grown rapidly over recent years and it is hardly surprising to find that the major players in this space fully expect the trend to continue.

In their paper, “ETFs 2026: The Next Big Leap” PwC surveyed 60 executives that account for 80% of global ETF assets. They said:

“…Over half of the respondents we surveyed believe that global ETF assets under management (AuM) will reach at least USD 18 Trillion by 2026. Representing a 14.6% CAGR between June 2021 and June 2026.

However, given global ETF AuM growth of 22% over the last five-years ending December 2020, combined with record inflows, new entrants, innovative products and distribution opportunities, we believe that a projection of over USD 20 trillion global ETF AUM by 2026 can be achieved, representing a 17% CAGR over the next five-years. …”

This represents a huge growth over the numbers Blackrock had, however, whilst we saw in Figures 3 and 4 that even though equity and fixed income products remain the dominant sectors in the ETF market, there is a drive toward innovation in Alternatives, Figure 5.

That is supported by PwC who contend that thematic, active, and crypto ETFs present potential sources of growth as many managers expecting to see heightened demand for these strategies out to 2026.

Costs will be coming under pressure as digital platforms will see more investors to switch to robo-advice and online platforms. This will also expand the reach of ETFs to less developed regions where local ETF expertise is thin or non-existent.

This will not be a “wild west” scenario. One should expect closer regulatory scrutiny that will expand in line with the market and the number of investing clients. In short, ETF activity will only flourish if investors who embrace market risk feel safe from financial malpractice.