Investing In Money Market Funds

What Is The “Money Market”?

The Money Market is a space where short-term financial assets having liquidity of one-year or less are traded. Given the securities being traded in this market are highly liquid, the money market is generally considered as a safe place for investment.

This implies there is minimal time for any default to occur and as such the money market can be defined as a market for financial assets that are close substitutes for money.

Money market instruments are generally seen as:

Bank Accounts, including Term Certificates of Deposit (CD’s), Commercial Paper (CP); Interbank Loans (loans between banks), Money Market Mutual Funds (MMMF’s), Promissory Notes, Securities Lending and Repurchase Agreements (Repos) and Treasury Bills (TB’s).

The participants in this financial market are usually banks, large institutional investors, and individual investors.

What Are The Objectives Of The Money Market?

To provide borrowers with short-term funds at competitive rates. Investors or lenders are attracted as they will enjoy the benefit of liquidity as the securities in the money market are all classified as “short-term”.

As such it allows investors access to an active investment as against just holding idle cash balances.

The central banking authority in a given jurisdiction will oversee and regulate the money market of that region, e.g. Federal Reserve in the U.S., Bank of England in the U.K. and the European Central Bank in the Euro Zone. The central bank can sell Government or Treasury Bills to drain liquidity and so tighten the money market. Alternatively it can buy such papers to add/inject funds or liquidity to make policy a little easier.

The money market marshals the resources to the capital markets via the process of interest rate control. It helps the functioning of the banks by setting the cash reserve ratio and statutory liquid ratio for the banks who then know exactly what level of capital cushion hey require given the size of a loan book.

Many corporations around the world will have varying working capital requirements. As such the money market helps them have the necessary funds to meet their working capital requirements and grow their top and bottom lines.

One should never overlook that fact that this market is a vital source of finance for the government sector and private sectors for both national and international trade. In this regard it offers an excellent vehicle for banks to place any surplus funds to maintain money supply in the market.

What Is A Money Market Fund?

A money market fund is a low-risk investment that provides one with a place to “hold” rather than “grow” ones savings. However, they will offer a return that is slightly higher cash.

It invests in short-term debt; e.g. the Vanguard Sterling Short-Term Money Market Fund buys short-term debt from the U.K. governments, banks and companies that have robust balance sheets and high credit ratings. Given the short-term and high quality profile there is just a small return as interest.

In this regard a money market fund is a stable, low-risk investment as the short timeframe of exposure implies there’s less uncertainty. However, it does have greater diversification than holding cash at one bank.

However, one should note that there are different types of money market funds, which depend on the invested asset, maturity period and other factors. These are the most common types of money market funds:

- Prime money fund – invests in floating-rate debt and commercial paper of non-treasury assets, such as those issued by corporations, government agencies and other enterprises sponsored by the government

- Government money fund – invests at least 99.5% of its total fund in cash, government securities and repurchase agreements

- Treasury fund – invests in U.S. treasury debt securities, such as treasury bills, bonds and notes

- Tax-exempt money fund – invests in short-term debt obligations issued by tax-exempt entities. They usually have a very low rate of interest but offer tax-free income

Occasionally one will hear the expression “Money Market Unit Trust Investment”. A unit trust investment is done by either a monthly debit order or a lump sum amount. The investment manager then takes all the contributions from all the investors and buys the underlying asset classes such as money market products or shares, bond maybe property.

In return, the investor gets a unit in the fund. As the underlying asset class goes up and down, so does the unit price.

What Is A Money Market Trust?

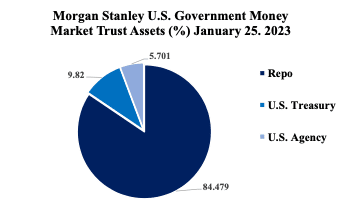

A U.S. Government Money Market Trust is a money market fund that seeks to provide security of principal, high current income and liquidity. For example, consider a product from Morgan Stanley. (Other investments are available).

This fund has a policy to invest exclusively in obligations issued or guaranteed by the U.S. Government and its agencies and in repurchase agreements collateralised by such securities in order to qualify as a “government money market fund” under federal regulations. The Fund may also hold cash from time to time.

A “government money market fund” is exempt from requirements that permit money market funds to impose a “liquidity fee” and/or a “redemption gate” that temporarily restricts redemptions.

In selecting investments, Morgan Stanley Investment Management Inc. (the “Adviser”) seeks to maintain the Fund’s share price at $1.00. The share price remaining stable at $1.00 means that the Fund would preserve the principal value of your investment.

The fund may also purchase securities issued by agencies or instrumentalities which are not backed by the full faith and credit of the United States, but whose issuing agency or instrumentality has the right to borrow, to meet its obligations, from the U.S. Treasury. Among these agencies or instrumentalities are the Federal National Mortgage Association (“Fannie Mae”), the Federal Home Loan Mortgage Corporation (“Freddie Mac”) and the Federal Home Loan Banks.

Further, the fund may purchase securities issued by agencies or instrumentalities which are backed solely by the credit of the issuing agency or instrumentality. Among these agencies or instrumentalities is the Federal Farm Credit System. The Fund may also invest in repurchase agreements.

Principal risks exist as there is no assurance that the Fund will achieve its investment objective.

“…You could lose money by investing in the Fund. Although the Fund seeks to preserve the value of your investment at $1.00 per share, it cannot guarantee it will do so. An investment in the Fund is not insured or guaranteed by the Federal Deposit Insurance Corporation (“FDIC”) or any other government agency. …”

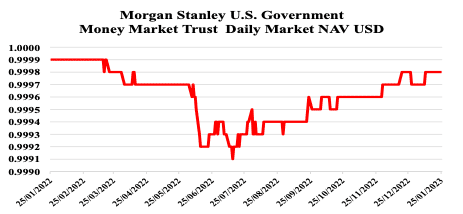

The daily net asset value of the Morgan Stanley U.S. Government Money Market Trust is shown below in Figure 1. As at the close of business on January 25, 2023, the following metrics were recorded.

Yield: 7-Day 3.97% Effective Yield: 4.05% Weighted Average Life: 47 days

Source: Morgan Stanley and Data Adapted by Pope Family Office

Source: Morgan Stanley and Data Adapted by Pope Family Office

Is This The Right Asset For You?

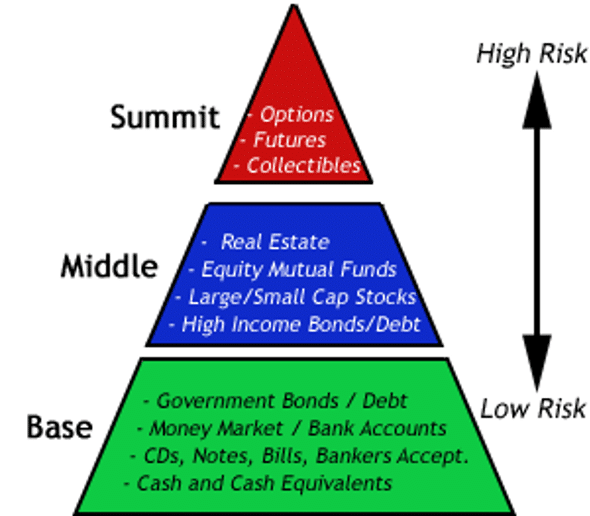

Money market funds work well for parking surplus cash and are as safe as one can ever be with any risk bearing instrument, the returns will be low. Figure 3 illustrates a pyramid of risk/reward.

One can clearly see the asset we have considered listed in the secure green zone on the base of the pyramid. Of course, Figure 3 is just illustrative, it is not a quantified or scientific chart. Just a guideline investors may bear in mind when considering likely destinations for their investment capital.

As one would expect, as one migrates to the upper portion of this chart are investments that have higher risks even though they offer investors a higher potential for above-average returns.

So whilst we now know a money market mutual fund is a type of account that invests in low-risk securities and generally offers lower returns than other market funds, they are popular as they tend to offer predictable, short-term returns.

The alternative that best fits one’s situation depends upon several factors, including how accessible one requires your funds to be and the amount of interest one will receive on the investment size. It boils down to what time horizon one has until the funds may be needed and what level of risk and/or volatility one can accept.