Investing in Government and Municipal Bonds

Government bonds are a crucial part of the financial system. They form the bedrock of the investment portfolios of financial institutions (such as asset managers and pension funds) around the world. However, they can also be an important asset for retail traders too.

We look into government bonds and aspects such as yields, risk and maturities. We look at how you can invest in government bonds, what move bond prices and a few pros and cons of investing in them.

What are government bonds?

Government bonds are investment products that are issued by governments. They are a loan to a government in return for interest in the form of coupon payments. If the bond is held to its full maturity, then the government (the bond issuer) will pay back the principal amount borrowed from the investor.

Government bonds are loans over a fixed duration at a specific interest rate. Subsequently, they are fixed-income assets.

Governments tend to spend more money than they raise in taxation. The difference is raised through issuing bonds. Investors loan the government money which can then be used to spend on infrastructure projects, war or just day-to-day spending needs.

Similarly, municipal bonds are issued by local or regional governments, often to raise money for spending projects. They are popular investment products in the US. “Munis” carry a higher yield than government bonds (although this does also come with an increased risk of default).

Government bonds – an ultra-low-risk investment (sometimes)

On the spectrum of investment risk, government bonds are almost as low risk as you can get. Only cash is considered to be a lower risk than government bonds. However, the level of risk will vary depending upon the government that you are buying bonds from, or to put it more accurately, lending your money to.

Some government bonds come with such low risk that they are considered “risk-free”. The bonds that are issued by the US Government are considered to be the lowest investment risk available. The US is the largest economy in the world and its government issues enormous amounts of Treasury bonds to cover enormous spending requirements. It is widely accepted that the US Government will never default on its debt payments, so its bonds are considered to be risk-free.

The rate that Treasury bonds pay out is considered by the investment community as being the “risk-free rate”. This is the rate at which all other investment grades are priced from.

However, the same is not true of all government bonds. Some government bonds are riskier than others. Ultimately, it is one of the reasons why the coupon rates (bond yields) that you can get on government bonds of the same duration can vary significantly from country to country.

For example, the bonds of governments that have an elevated risk of default (such as Argentina) will need to pay a far higher interest rate (coupon payment) than those of the US Government. The US will not default on its debt, but Argentina might. Subsequently, the Argentinian government will need to entice investors with the promise of much larger coupon payments to tempt investors into lending to it.

A quick look at a bonds price versus its yield

A government bond is a fixed-income asset. It always pays the same coupon. However, the price that the bond trades at in the secondary market (see later) can change. If the bond is trading above the par value it is said to be selling at a premium. If it is below par value then the bond is at a discount.

So if the coupon stays the same and the price changes, therefore the yield on the investment (the coupon compared to the market price) will change. The yield therefore will go down if the value of the bond goes up. Hence why bond prices and their yields have a perfect inverse correlation.

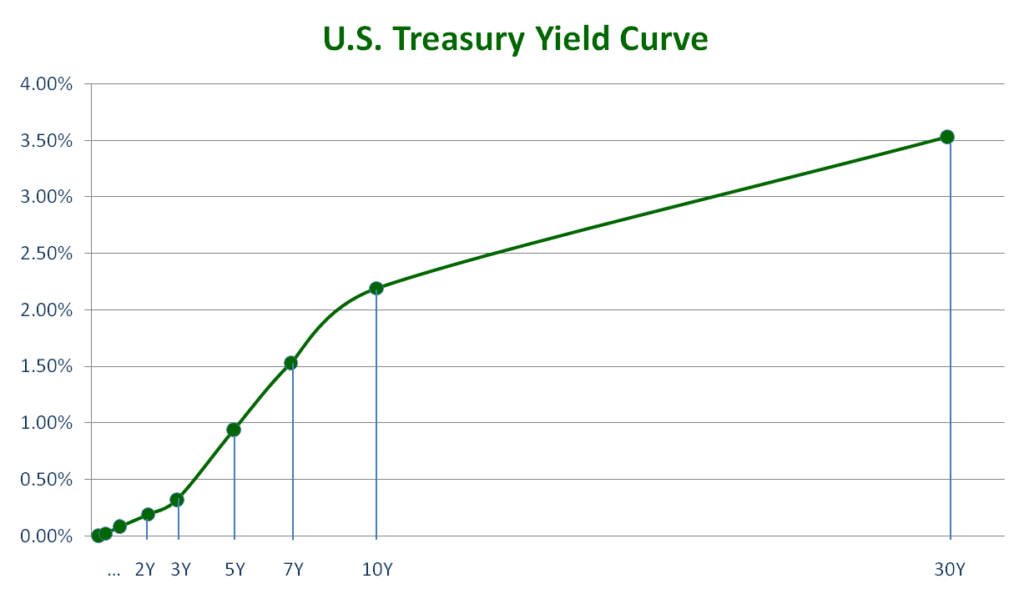

Bond maturities, duration and the yield curve

Governments issue bonds of varying maturities. This is so that all of their debt does not come up for maturity at the same time. This means that governments have bonds of a duration that can be from as little as 3 months to often as long as 30 years. The varying yields (the market price representation of the interest due for each maturity) can be plotted on a graph known as a yield curve.

The Primary and Secondary bond markets

There are two markets for bonds, the Primary Market and the Secondary Market. The government raises money for its funding directly by selling bonds on the primary market. Most of the players in this market will be financial institutions, although individual investors can also take part.

Once the bonds have been issued and bought on the primary market they will be used by investment companies and pension funds for their proprietary investing purposes. However, they can also then become available for their clients to invest in too. This then opens up a secondary market of government bonds. This is the open market for bonds and is how bond prices develop a price different to the “par value”.

How do I invest in government bonds?

There are several ways to invest in government bonds. Let’s look at how.

1. Directly from the government (the primary market)

As we mentioned earlier, individual investors can buy government bonds directly through the primary market. In the UK, this is done via the Debt Management Office. Investors can apply to become a member of the Approved Group of Investors. They can then buy and sell UK Government bonds. Investors can also buy US Government bonds directly through the US Treasury.

2. Through an investment manager intermediary (the secondary market)

Investors can also buy and sell government bonds in the secondary market. Clients of investment management firms can buy government bonds for their portfolios.

It is also possible to buy bonds over the counter through some trading platforms. Furthermore, some brokers offer spread betting or bond CFDs where you can buy (go long) or sell (go short) synthetic bond products and trade on margin. However, it is important to remember that these are higher-risk products than traditional government bonds. Also for these synthetic products, you are not owning the underlying government bonds.

3. Bond funds

It is possible to invest in bonds through funds such as Exchange Traded Funds (ETFs), mutual funds or unit trusts. A bond ETF is a security that you can buy and sell (similar to a stock), however, the purpose of the fund is that it invests in bonds. Unlike bond CFDs, with bond ETFs, there are real bonds underlying the investment. The value of the bond ETF moves on changes in the value of the underlying bonds in the fund.

There are several options of bond ETFs to choose from, making them an increasingly popular way to get exposed to government bonds. A bond ETF might track one bond or a basket of bonds. It might have exposure to one country, or several countries (such as emerging markets). A basket might have exposure to a specific duration, such as shorter-dated (0 to 5 years) or longer-dated (10 to 20 years). The ETFs of government bonds tend to often come with very low expense ratios, making them an inexpensive and simple way to get exposure to the asset class, without the fuss of you having to manage the investment.

What moves government bonds?

Several factors will influence the outlook for government bonds. Here are some of the important ones to consider:

Interest rates – The central bank interest rate is the primary driving force behind how bonds move. If the central bank changes interest rates higher or lower, it will determine whether the bond’s (whose coupon is fixed) price will either increase or decrease. If interest rates are falling, fixed income will be more valuable. The bond price will fall and the yield will rise. The opposite will happen if a central bank raises interest rates. The opportunity cost of holding the fixed income bond increases, the bond is perceived to be less valuable (you can get better yield elsewhere). Selling pressure increases, the bond price falls and the yield rises.

Credit rating – If the country (and therefore the government) has its credit rating changed, then the perceived risk of holding the bonds will change. A better credit rating will likely drive the price higher. A credit rating downgrade increases the risk of default (albeit marginally), making the fixed-income bond less valuable, and the price falls.

Market conditions – broad market conditions and risk appetite will influence the outlook for government bonds. If risk appetite improves, traders will be selling bonds to move funds towards higher-risk assets that can get a better return. Government bonds tend to perform well during times of negative risk appetite, where bonds are seen as a safe haven.

The benefits of investing in government bonds

We will now look at some of the pros and cons of investing in government bonds. Interestingly, some of the pros can also be seen as cons too.

We will start with some of the pros:

1. A steady and assured income stream

Government bonds (especially ones with a strong credit rating) can add a steady stream of income to a portfolio. The income from government bonds is more assured than with equities (companies can always choose to cut or stop dividend payments).

2. Very low-risk investment

As we mentioned earlier, government bonds tend to be seen as the lowest-risk investment asset class. This can work well for a portfolio during times of economic crisis and economic slowdown (although even bonds can be sold off when investors panic).

3. A highly liquid market

The market for government bonds is highly liquid. This means that trading at current market prices is simple, with little slippage and a large pool of buyers ready to take the other side of the trade if you need to sell quickly.

4. Add diversification to a portfolio

Investors sometimes struggle with diversification. Being overinvested in one asset class (as can happen with stocks) can impact the long term performance of a portfolio. Government bonds add diversification and help to add long-term stability to investments.

The risks of investing in government bonds

Some of the risks of government bonds come hand in hand with the benefits. It sometimes just depends upon what type of investor you are as to whether it is a pro or a con.

Here are a few cons:

1. A very low-risk investment

Although the low-risk element of government bonds brings stability, it can also be a drag on your portfolio. The potential returns can be limited. The opportunity cost of better returns elsewhere can be frustrating, especially in bull market conditions. Very careful consideration needs to be given to exactly how much of the portfolio should be weighted in government bonds.

2. Fixed income loses out in an inflationary environment

Opportunity cost is a key problem for owning government bonds. If economic conditions remain benign, with low inflation and low interest rates, government bonds can be a solid source of income. However, if inflation starts to rise then the opportunity cost of holding bonds increases. Inflation erodes the value of fixed-income products (you are always going to get the same amount on the coupon). However, inflation-protected bonds are available to counter this issue.

3. Fixed income loses when interest rates increase

This is an extension of the inflation problem. If interest rates rise, then the opportunity cost of owning fixed income rises. You could be getting better returns on your investments elsewhere.

Government and Municipal Bonds Investing Takeaways

Although they might be seen as dull and boring investment opportunities (especially compared to cryptocurrencies), government bonds are an extremely important asset class for the global financial system. Everyone that has a government pension will be exposed to them to some degree.

However, they are also an asset class that can be beneficial for investors. They add diversification and stability to a portfolio in addition to a secured income stream. The primary disadvantages lie in their low-risk status and the opportunity cost of missing out on potentially higher returns elsewhere.

There is plenty to consider when choosing whether to invest in government bonds. As ever though, if you are unsure, we suggest speaking to an independent investment advisor.