This is not exactly a new question – what should I do with my investments in this market? For markets always change, so what should be done in them changes as they do. This is, from the grander economic point of view, rather the point of using markets in the first place – things change, we must react to those changes. That’s also not a grand guide to what we as investors should do in the current markets of any specific time. It’s rather, too hand wave to be directly useful as a guide to what we should do, precisely.

What we’d like, given this market, is a little more accuracy about what we should do with our current investments. The following three companies, Made.com (LON: MADE), Imperial Brands (LON: IMB) and Rivian (NASDAQ: RIVN) are not suggestions, they are examples. This is not a prediction about which of these shares will do well, it is to use them as examples of how we should be thinking when we reallocate our current investments in this market.

What Can Go Wrong?

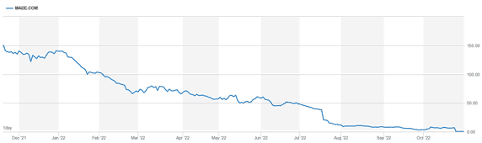

So, Made.com. That’s easy, it’s bust, the shares no longer trade, the company is in administration. So, not only don’t we want to be there, but we also can’t be. And yet it’s still a good example. What went wrong with Made.com?

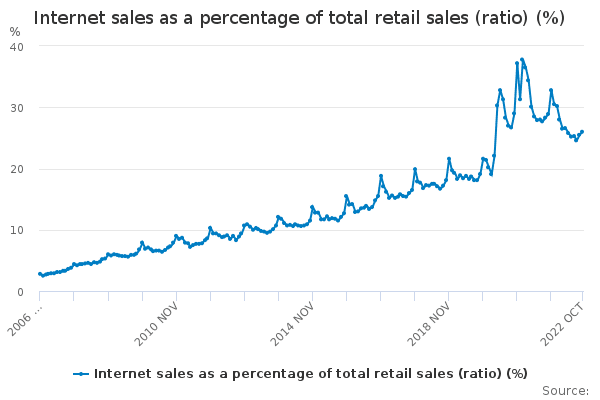

If we leave aside the details of what management did or did not do it’s the Office for National Statistics who can tell us. Below is the chart of online as a percentage of all retail sales.

We can see that there was a vast leap during lockdown – obviously. But then comes the question. We know that online is eating bricks and mortar, even for furniture. So, will that step change during lockdown remain? Or will we see a slump back to trend of perhaps that 1% a year being munched?

Well, we could run either way with that and reality is what would, in time, tell us the right answer. As it turned out it was a slump back to trend. So, those who were valued as if it was a leap forward suffered. Those who – like Made perhaps – ran the business as if it was, went bust. Well, shrug for that one. But for us out here that’s an important lesson. Reversion to the mean – things go back to roughly how they were before a big event – is a real thing. We should thus be looking more than a little askance at those insisting that some specific event really proves they’re in the right.

Macroeconomic Factors

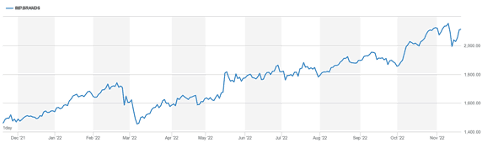

The other two are useful examples of how the macroeconomic situation has changed. Rising interest rates and rising inflation make relative prices and values change. Imagine that Rivian succeeds in making their vans the EV of choice for delivery folk. No, go on, do that for a moment. Imagine also that Imperial simply continues to sell cancer sticks to people. Imagine, just for our model, that there’s no change in their businesses at all, we’re merely looking at the effects of inflation and interest rates.

Imperial rises in value as against Rivian. Nothing to do with how well each market performs and so on, purely because of those big wider economic changes in inflation and interest rates.

The reason is that Rivian might, maybe, build that grand new business. But there’s risk there – obviously – and it’s going to eat capital getting there. The money put in today is worth something. But the money we get back in that possible future is going to be worth less – inflation and interest. On the other hand, Imperial is throwing off a 7 or 8% dividend each year. That’s close to what the inflation rate is. So, we can preserve value by being in Imperial in a manner we can’t in Rivian – unless, of course, Rivian really does win.

The Investment Takeaway

Again, this isn’t advice about which specific shares or stocks to be in. This is sectoral advice, not specific. Inflation and higher interest rates change the relative values of business plans. They lower the value of attempts to conquer future markets and raise those of those who are throwing off the profits and dividends of having mastered old ones.

Of course, a cigarette maker like Imperial breaches every ESG concept we might think about. But then again that brings ESG concepts into the foreground. What do we actually care about, money or morals? Something we each need to think about for ourselves.