Atlas Lithium (NASDAQ: ATLX) could be one of those rare and truly grand investing opportunities in the junior mining space. Someone does, after all, have to find the motherlode sometimes otherwise where would the very phrase come from? One the other hand it’s possible – as some allege – that Atlas Lithium is an over-hyped OTC share that will fade back substantially.

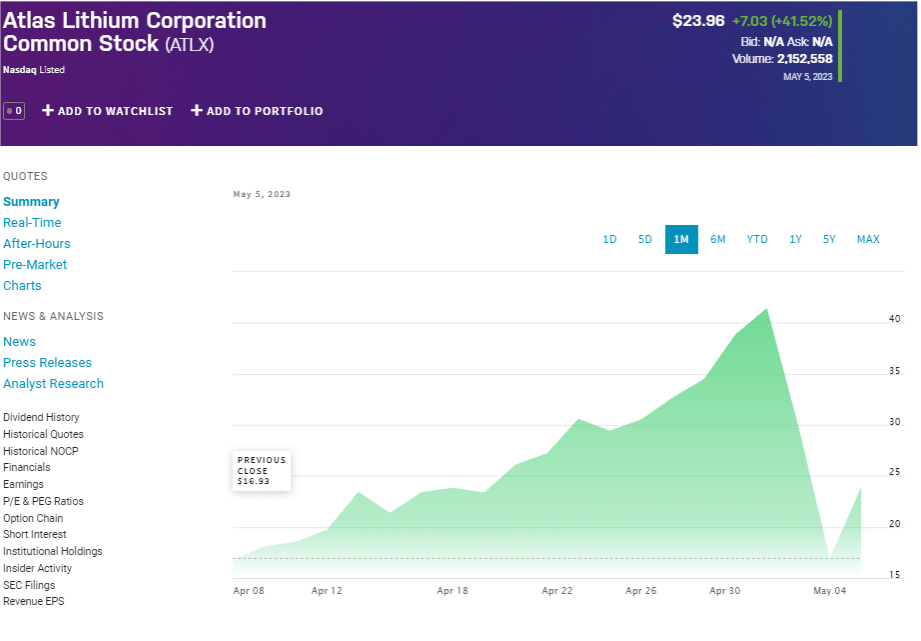

Atlas Lithium stock price from NASDAQ

Note that chart is just for this past month – $15 to $40 back to $15 again. It was $7 back in March.

Lithium explorers like Atlas are junior miners

This is, of course it is, why people like trading junior miners – junior here means not actually producing anything yet. The price swings can be wild – as can the risks of course. The reason prices are so volatile is that along the pathway from “Oooh, that’s a nice mountain of rock” to “Here’s a producing mine” there are a number of valuation, validation, points. We have shown there are resources, we have proven those resources into reserves, we’ve proven the processing technology, we’ve gained offtake partners, have raised industry finance and so on. Passing any one – and usually every and each of them – is one of those valuation points. For passing each stage is a validation of the project. To get to have an actual mine which is digging something up and producing revenue each of those stages does have to be passed. By far the majority of exploration projects fail in that they get stuck just before one of those necessary points.

So, Atlas Lithium. Exciting little company in an exciting field. The exploration area is in a part of Brazil where it is absolutely known there are lithium deposits. Some of them, close by (those owned by Sigma Lithium, for example) have passed near all of those stages.

The economics of the market Atlas Lithium is in

The biggest stage in this sort of lithium mining (from spodumene, also known as “hard rock” mining) is getting a deal with one of the processors of the output (the standard output is a 6% lithium concentrate, which then has to go to a specialist processor). That deal usually provides both the offtake – the guaranteed customer for the output – and the capital to build the plant. Sigma has this, so Atlas is right on the road to success, right?

Well, maybe. Atlas Lithium looks like it has one of those offtake/financing contracts. But detailed examination says that it’s got one on a “if” basis. If the exploration turns up resources which are then proven into reserves then there’s an offtake/financing deal. So, to some it will look like Atlas has that validation when, well, no it doesn’t really, not yet.

That royalty deal

Atlas has also negotiated a royalty deal – this is another form of early mine finance. The royalty company offers money now in return for a slice of the cash from future output – a percentage of the minehead sales price. OK, this is pretty standard but at what rate? The 3% royalty rate on this deal would provide a 90% annual return to the royalty company if – if – the Atlas mine opens at currently predicted size. That’s not, to put it politely, someone investing in a near certainty, that’s someone taking a bet on a significant risk.

Then, there’s the short sellers report from Bleeker Street Research. Which basically claims the whole thing’s a con-job typical of penny stock investing. Other analysts are suggesting it is undervalued at these prices.

We’re not making a prediction about Atlas, this is about the lithium market

Now who is right here isn’t our point at all. We have no view at all. What we want to do is use this as an example. There are pumps and dumps in this junior mining space. We know of several. Precisely because there are those valuation points it’s easy enough to convince that one is about to happen, the share price pops and then those pumping can sell. The validation never actually comes through though. The reason this can be done is because there really are companies that do extremely well by developing a mine. There are even those who fail at a mine then the next owners make a fortune (Altura went bust, Piedmont has made a fortune out of the same mine a couple of years apart. The lithium price changed in between).

That is, exactly because this is an exciting and high-risk game, these junior miners, it’s possible for the unscrupulous to play off those and rook, cheat even, investors. Just as there are honest people running companies as best as can be done. And, of course, some find deposits that are in fact developed into mines. For absolutely every large-scale mining company around, every mine, started off as one of these junior miners trying to raise a bit of cash to investigate these interesting rocks.

Junior miners as a sector – have a portfolio

Our actual point here isn’t about Atlas Lithium at all – that’s just the example. Junior mining stocks can be highly volatile for sensible and practical reasons, that’s just the nature of the process. There’s also a certain attraction of the sector for the less than scrupulous. The end result of which is that eggs and baskets rules operate here. The risks are such that we are not really engaging in investing here, this is speculation. Portfolios of positions will, over time, work better than individual positions. Risk should be limited to losses that can be afforded – for over a portfolio there absolutely will be losses.

Finally, a warning. Mining sectors do become fashionable. Back in 2010 rare earths were all the rage. By one count there were 420 rare earth projects at various stages of looking for investment at that time. Two of them went into production within the next 7 years.

Junior miners are a risky game, one that’s played wisely can indeed work for the investor.