Copper demand will skyrocket this decade. Supply is falling, and inventories are at near-record lows. For the long-term investor, it’s merely a waiting game.

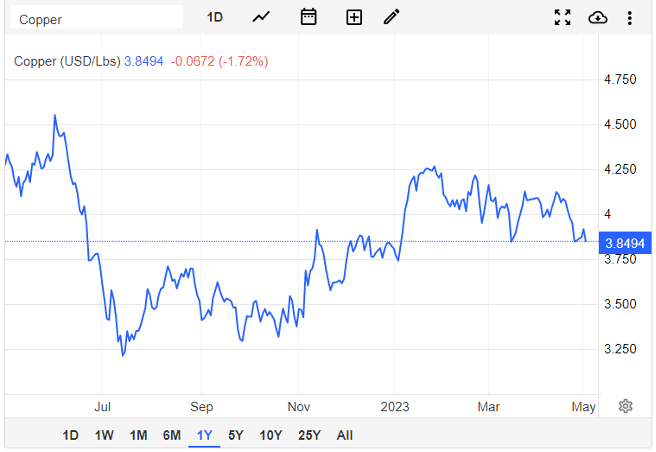

In early November 2022, I wrote up an article covering the growing consensus surrounding the emerging copper supply gap. Simply put, copper demand is growing exponentially, and supply is drying up. And this is going to send copper’s price to the stratosphere.

Of course, this is only my opinion.

Despite a slight overall rise, copper prices haven’t made much headway since then. Indeed, copper was worth far more between May 2021 and April 2022, and a breakout to new record highs seems unlikely in the very near future.

Fortunately, I’m a patient person.

In 2021, the shortage gap — the difference between copper mined and demand — came to just 2% of production, enough to push up copper prices by 25%. And decarbonisation will only happen if enough of the metal is mined, processed, and built into the global infrastructure.

But inflation has driven production costs up by 30%, and the cyclical nature of commodities mean that investors wary of falling demand aren’t prepared to invest in new mines that could in theory be unprofitable while in development. Instead, miners are taking the certainty of dividends and share buybacks that are always popular with investors.

With mine supply growth set to peak in 2024, the world could see a deficit of 10 million tons in 2035 according to S&P Global. Primarily, this is because global demand is set to double from 25 million metric tons today to about 50 million metric tons by 2035.

Bloomberg Intelligence goes one step further, seeing that the gap will hitting 14 million tons by 2040. It estimates that demand for refined copper will grow by 53% by 2040, but mine supply will rise by only 16%.

Meanwhile, London Metal Exchange inventories have already spent weeks below the 2005 low watermark of 56,000 tonnes.

Production and grades collapse

Goldman Sachs research shows that miners need to collectively invest $150 billion in the next decade to plug the copper gap, while also noting that regulatory approval for new copper mines has fallen to the lowest in a decade. Goldman expects copper prices to rise by 67% to $15,000 a tonne by 2025.

In a recent note emailed to clients, Goldman analyst Nicholas Snowdon argues that ‘Copper is sleepwalking towards a stockout…we believe higher prices are an inevitability’.

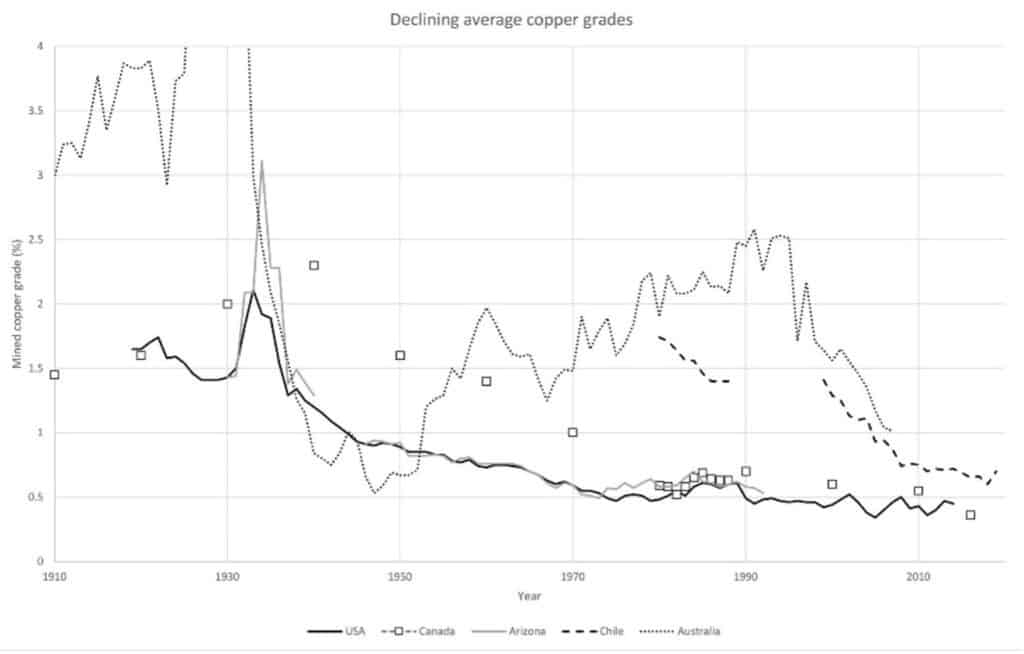

Above is a graph showing the declining grades of copper from the world’s largest producers over the past century. Forget the fact that we need to mine more copper, even if we do, new mines simply do have the same ore quality.

In the 1990s, copper exploration grassroots budgets ranged from 50-60% of overall copper annual budgets; this had fallen to just 34% by 2021. And it takes 16 years — on average, according to an estimate of sources — to discover and develop a new copper mine.

Companies are instead laser-focused on buying up established assets. Multi-billion-dollar deals are ongoing to reduce costs and bring producing mines on board. BHP bought ASX copper producer Oz Minerals for a hefty premium, Newmont’s record bid for Newcrest may bring gold synergies but also huge copper deposits, and Glencore is desperate to buy out Teck Resources — which very sensibly, is playing hard to get.

But it doesn’t matter who owns the mines. It’s shuffling deckchairs on the titanic — there’s still only so many lifeboats (or producing copper mines).

Ivanhoe founder Robert Friedland famously thinks that more than 700 million mt of copper will need to be mined in the next 22 years just to maintain typical 3.5% GDP growth, without even considering the electrification of the global economy. This is equivalent to all the copper ever mined in history.

Consider Rio Tinto’s new Oyu Tolgoi mine in Mongolia. Wood Mackenzie analysts estimate that the equivalent of 12 new equivalent copper mines will be needed to come online by 2030 to meet expected demand.

Yet Oyu is being touted as one of the most important copper deposits in the world, and development from bare earth to near production has been extremely hard. Construction has involved 200km of concrete tunnels to the open pit, miles and miles of roads, a new airport, massive spending on power transmission and water infrastructure, and substructure to accommodate 20,000 workers.

It still needs a power plant.

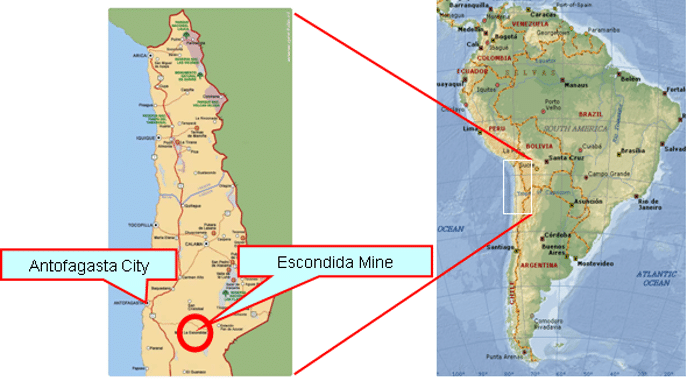

Let’s look at Chile — the world’s largest copper producer. It mined just 440,389 tonnes of copper in March 2023, a fall of 4.8% compared to the same month last year. BHP has cut production guidance at Escondida (the world’s largest copper producing mine) to 1.05-1.08 million mt from a previous range of 1.08-1.18 million mt. BHP’s Rag Udd has already argued that ‘demand is there. What I think potentially impacts it, is lack of supply.’

Meanwhile, MMG’s copper production fell by 13% in Q1 due to lower grades at the giant Las Bambas mine in Peru.

Budding copper countries with potentially higher ore grades come with their own set of problems. FQM’s copper production fell by 33% quarter-over-quarter to 139,000 tonnes in Q1 due to a severe rainy season in Zambia and Panamanian political problems. And in February, Freeport-McMoRan was forced to halt production at its titanic Grasberg mine in Indonesia for a fortnight after the mine was hit by floods.

Trafigura — the world’s largest copper trader — CEO Jeremy Weir recently noted at the World Copper Conference that ‘if we don’t have enough copper, it could seriously short circuit the energy transition.’ The International Copper Association thinks that while global supply is expected to jump by 26% to 38.5 million tonnes annually by 2035, it will likely still fall 1.7% short of demand — even assuming that recycling rates increase exponentially.

There simply won’t be enough copper next decade — and the copper price will shoot up.

UK-based investors can buy shares in small cap copper explorers to benefit hugely from near-term acquisitions (ARCM, TYM etc), and shares in the larger copper companies which now appear undervalued — assuming you agree with the bull copper thesis.

And given that every analyst, producing company, and dataset is in agreement, the world may only wake up when the copper pricing chart starts to shoot up.

Investors should prepare long before then.

This article has been prepared for information purposes only by Charles Archer. It does not constitute advice, and no party accepts any liability for either accuracy or for investing decisions made using the information provided.

Further, it is not intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.

… lange Rede ohne Sinn. No one is interested with cooper price in 2035 or 2040. Investor need to know what cooper price is gona be today, tomorrow, this year. Anyway thanks very much for putting your efford to write this prediction (?)