Macroeconomic/ geopolitical developments

- US equities delivered a mixed weekly performance as the S&P 500 rose 0.34% and briefly broke above 7,000 for the first time, while the Nasdaq slipped 0.17% and the Dow Jones Industrial Average fell 0.40%, with gains in energy and value stocks offsetting weakness in growth shares against a backdrop of a modest yield-curve steepening, a surge in oil prices, and softer gold.

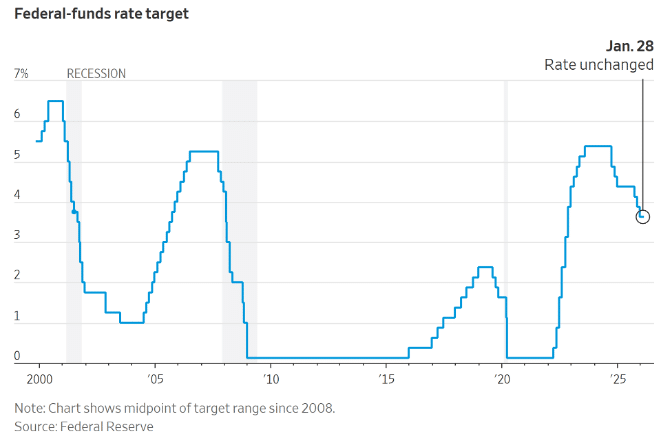

- The Federal Reserve held rates at 3.50%–3.75% after a 10–2 vote, citing solid economic growth and still-elevated inflation while signalling a patient, meeting-by-meeting approach, as attention turned to President Trump’s nomination of former Fed governor Kevin Warsh to succeed Jerome Powell, a move that could modestly influence the policy outlook pending Senate confirmation.

- Tech giants Meta, Apple and ASML showed mostly strong results, driven by AI demand and robust iPhone and advertising sales, while Microsoft and Tesla faced execution and margin pressures, highlighting both growth opportunities and near-term challenges in the sector.

- Markets face a pivotal week as investors assess results from tech heavyweights Alphabet and Amazon for signs that AI-driven spending is boosting cloud growth and profits, while Friday’s US Jobs report is expected to show modest hiring and steady unemployment, shaping expectations for the Federal Reserve’s policy path.

Global financial market developments

- US and global equity averages were mixed on the week.

- US and European bond yields were mixed, with EU yields lower, and the UST yield curve steepening.

- The US Dollar Index moved to a multi-year low, before a bounce.

- Gold futures plunged Friday, having surged in January to a new record high.

- Oil futures prices surged through the week to a multi-month peak.

Key this week

Central Bank Watch: It is an active week for central bank activities, with key Interest Rate Decisions, Monetary Policy Statements, and Press Conferences due from the Reserve Bank of Australia on Tuesday, followed by the Bank of England and the European Central Bank on Thursday.

Macro Data Watch: The key macro data releases this week include Global PMI readings on Monday and Wednesday, followed by the closely watched US Jobs report on Friday. Additional data of interest includes Retail Sales figures from Germany and the Eurozone, Eurozone HICP Inflation, and Canada’s Employment report.

Earnings Watch: US fourth-quarter earnings season continues this week, highlighted by results from two Magnificent Seven names, with Alphabet reporting Wednesday and Amazon following on Thursday. Other key releases from Palantir, Walt Disney, AMD, Merck & Co, PepsiCo and Eli Lilly which will also help shape the corporate narrative.

| Date | Major Macro Data |

| 02/02/2026 | Global Manufacturing PMI; German Retail Sales |

| 02/03/2026 | RBA Monetary Policy Statement, Press Conference and Interest Rate Decision; US JOLTS Job Openings; ECB Bank Lending Survey |

| 02/04/2026 | Global Service and Composite PMI; EU HICP and PPI; US ADP Employment Change |

| 02/05/2026 | German Factory Orders; EU Retail Sales; BoE Monetary Policy Statement, Interest Rate Decision and Minutes; ECB Monetary Policy Statement, Press Conference and Interest Rate Decision; US Initial Jobless Claims |

| 02/06/2026 | German Industrial Production and Trade Balance; Canadian Jobs report; US Jobs report; Michigan Consumer Sentiment Index and Consumer Inflation Expectations |

| Date | Major Earnings Data |

| 02/02/2026 | Palantir; Walt Disney |

| 02/03/2026 | AMD; Merck&Co; PepsiCo; Amgen; Pfizer; Eaton; Chubb; PayPal; Nova Nordisk |

| 02/04/2026 | Alphabet; Eli Lily; AbbVie; Qualcomm; Boston Scientific |

| 02/05/2026 | Amazon; Linde PLC; ConocoPhillips; Shell |

| 02/06/2026 | Philip Morris |