Funding Circle (LON: FCH) started out as what seemed like a great idea. Let’s go revolutionise the small business lending market! We all know that British banks don’t lend to business, even when they do it’s only against security, there’s a ripe market for the picking there.

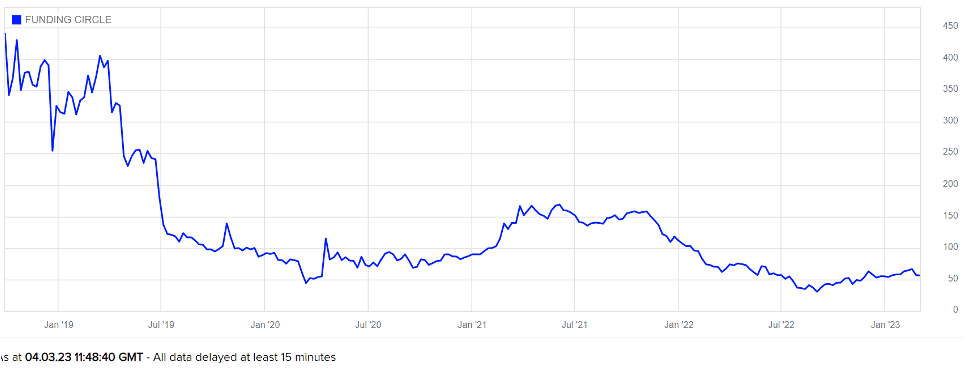

Since then, the share price has gone from 440p to 50p-ish so clearly there’s a problem with that story.

Yes, clearly there is a problem but what is it?

Innovators Like Funding Circle Need to Solve the Actual Problem

Let’s leave aside the details here. Yes, it’s true they’ve gone back into loss in their latest accounts. They’ve in fact only made a profit once since the flotation back in 2018 and that was in the pandemic affected year of 2021. Those emergency loans that they helped dish out are being repaid so the loan book is shrinking. So, what is actually the problem?

It’s in the basic offering of Funding Circle itself. Or, OK, my contention is that it is if we’re to have to be accurate here. Funding Circle’s pitch is that here’s a new way of lending money. Of gaining access to money to lend. Which isn’t the banking problem at all. There is a reason that there appears to be a gap where Lloyds, NatWest and the rest don’t lend. That reason being that the gap isn’t, not really, there. Not as a profitable gap that is.

Banking’s Problem Is Finding Borrowers

This is something that afflicts everyone who attempts to upset the banking industry. Thus, it’s a lesson we need to apply to everyone attempting to upend the banking industry. This is true whether we’re talking about new banks, or shadow banks, or new business loan banks and so on. It’s even laid out for us back in Adam Smith’s Wealth of Nations. The people really hot to borrow money aren’t the people you want to lend money to. Those who will pay the highest interest rates are those without sensible plans to deploy those borrowed funds – which makes it unlikely the loan will be repaid.

Now of course, this is not an absolute. But it is true that the basic banking problem is not gaining the funds to lend out. That’s trivially easy in fact, just borrow from the wholesale markets. Nor is it some new and groovy method of lending the money out. The actual problem is the shortage of people it’s worth lending money to.

Banking Has Been Around for Centuries After All

Another way to think through this is to consider that the major banks – the Lloyds, Barclays and so on – grew by merger in the 20th century. But their precursors go back a couple of centuries. There’s therefore an awful lot of institutional knowledge about past experimentation bound up in those firms. If we are to claim that there’s an entirely new body of creditworthy borrowers out there, then we are also claiming that money-hungry capitalists have missed this for the past two centuries.

There are times when we can believe this. Say, the application of AI to consumer credit borrowing. That might work, cheaper rules-based decision making could uncover those on the edge of the old rules but who are still profitable. But business lending isn’t like that at all. It’s not a few hundred here and there and make up the credit losses on the higher interest rates. Business lending is large chunks of money dependent upon that creditworthiness.

Peer To Peer Lending Suffers the Same Problem

This is what has afflicted near all of the peer-to-peer lending companies among other new entrants into the banking market. Peer to peer can be seen as a new method of raising the funds to lend. Great, except that’s not the banking problem. Peer to peer, just as Funding Circle, faces a different problem, the paucity of those creditworthy enough to lend to. Move beyond that small group possibly ill-served by current arrangements (for there will always be some marginal cases not well served by any system) and credit losses soar.

There’s a much larger issue for us to think about here too. Anyone claiming to revolutionise a market. OK, fine, that’s great. But what, exactly, is it that is being revolutionised? Is it the thing which actually causes the problem that is?

So, we’ve the banking point, which is that it’s finding people worth lending to which is the problem to be solved. And that observation needs to be applied to all upstarts and innovators. Is the innovation something that solves the sectoral problem or not?