Genedrive is financially almost out of runway, but its tech makes it a reasonable buyout target.

Genedrive (LON: GDR) is a FTSE AIM company out of which many investors have fallen in love. The molecular diagnostics biotech company spiked multiple times through the pandemic-induced meme hysteria, reaching a record 173p per share in May 2020.

Having fallen to 8p in early December 2022 after disappointing full-year results, it then recovered to 29.5p by 27 January — a 269% rise with seemingly with no catalyst at all — and has now fallen back to 21.4p.

What’s going on? There are three possibilities: a fat-finger trade or an insider information leak both look unlikely; fat fingers are usually resolved very quickly, while there seems to be no further information available beyond that published on the RNS.

This leaves the third possibility — the market is currently pricing the company and isn’t sure what it’s worth.

Genedrive in brief

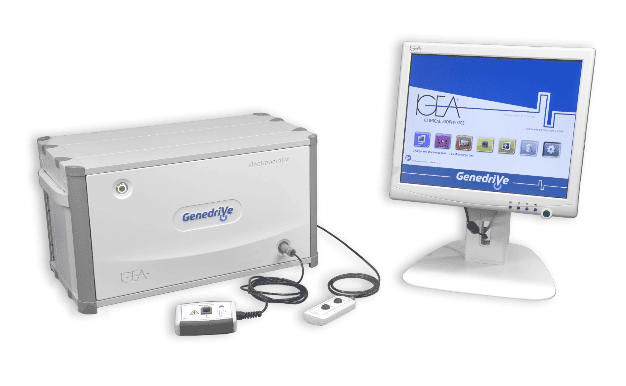

Genedrive offers a patented ‘Genedrive’ device, a rapid point-of-need molecular diagnostics platform for use in genotyping, pathogen detection, and infectious disease detection.

The company has developed tests for detecting Antibiotic Induced Hearing Loss in neonates, confirmation of HCV infection prior to drug administration, pathogen detection of biological military threats and a point-of-care for COVID-19 detection system for use in areas such as healthcare, workplace screening, travel requirements, or confirmation of antigen tests.

The company is now focusing on emergency medicine, as the company believes that the delivery of genetic information more quickly than is possible with rival platforms gives it a competitive advantage. For context, GDR was the first British company to install a commercial genetic test into an emergency care setting.

Full year-results

On 21 November, GDR released results up to 30 June 2022 that were poorly received by the markets. Headline earnings were poor; revenue came in at just £50,000, down from £690,000 in the 2021 financial year. Accordingly, the FTSE AIM company suffered a loss of £4.7 million, up from £700,000 in the prior year.

Usually with biotechs, increasing losses can be justified by additional spend on Research and Development, for which there are excellent tax credits and the chance of huge growth; however, spending on R&D fell by £600,000 to £3.9 million. Worse, the £1.2 million R&D tax credit it claimed for the year could be lower in this financial year due to rule changes announced in the Autumn budget.

While the company was at the time debt free, with cash of £4.6 million, this implied a cash runway of just less than a year, with virtually no revenue coming in. And this was the financial position as of six months ago. This makes the likelihood of a placing fairly high — but it remains to be seen whether the £20 million company would be able to sell placing shares even at a steep discount.

Indeed, while the company says it is ‘confident in gaining commercial traction and securing significant revenues,’ the ‘time required to achieve this’ means they will ‘will require additional funding in our 2023 financial year.’ This leaves it with ‘a material uncertainty that may cast significant doubt on the Group and Company’s ability to continue as a going concern.’

But its patented tech does appear to have value.

Genedrive tech

A huge part of the company’s problems is that it spent too much time focusing on its covid-19 POC test, which was only granted regulatory approval in May 2022 after lengthy delays. The pandemic is all but over, so this huge financial and temporal effort was utterly pointless.

However, operational highlights over the past year have included a JAMA Paediatrics’ PALOH paper supporting the implementation of the Genedrive MT-RNR1 test in the Neonatal Intensive Care setting, and the first NHS deployments and sales of the Genedrive System for Antibiotic Induced Hearing Loss within several Manchester hospitals. This could be the springboard to wider deployment if shown to be both successful and cost-effective.

There was also the launch of the second generation Genedrive system to support strategy focus of assay development to emergency care settings, with a National Institute of Clinical Excellence (NICE) accelerated evaluation of the company’s proprietary MT-RNR1 ID test.

Further, the company has started a new product development programme for the use of its Genedrive Point-of-Care device for ischaemic stroke treatment, again for use in emergency care settings. And it’s filed a US FDA pre-submission for the MT-RNR1 ID product range.

The company needs cash and would struggle to raise it. But it owns patents to valuable tech and is just suffering from a temporary cash flow issue. This raises the possibility of a buyout.

With private equity and larger biotech giants on the prowl, it could be worth a speculative punt — but would-be investors will rest uneasy in the knowledge that the company has a hard deadline in June.

This article has been prepared for information purposes only by Charles Archer. It does not constitute advice, and no party accepts any liability for either accuracy or for investing decisions made using the information provided.

Further, it is not intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.