Macroeconomic/ geopolitical developments

- Major US equity indexes posted a second weekly decline, with the S&P 500 and Dow Jones Industrial Average down 0.35% and the Nasdaq easing 0.06%, with early tariff-driven volatility, while strength in energy, materials, oil and gold contrasted with weakness in financials and real estate amid steady Treasury yields.

- Markets faced heightened uncertainty as President Trump’s initial tariff threats on eight European nations over Greenland and on Canada over potential China trade deals sparked volatility, though the risks eased after he reversed course following diplomatic engagement. Tensions with Iran remained elevated, with US naval deployments to the Gulf and Tehran signalling readiness to defend against any attack, underscoring persistent geopolitical risks that continue to influence global markets.

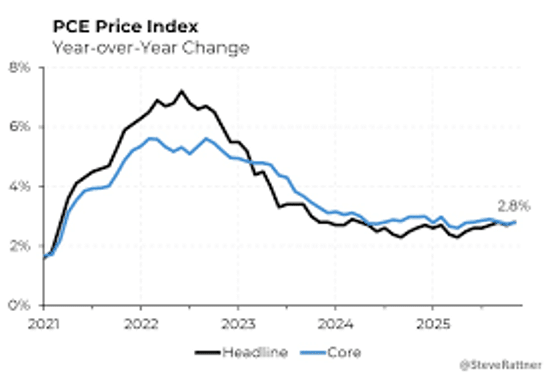

- US GDP growth was stronger than expected in Q3 at 4.4% annualized, driven by broad gains in spending, investment, and exports, while inflation remained elevated at 2.8% year-over-year, highlighting a mix of robust growth and persistent price pressures.

- Markets face a pivotal week as investors await the Federal Reserve’s widely expected decision to hold rates steady while parsing Chair Powell’s guidance, alongside key earnings from four Magnificent Seven members, Microsoft, Meta, Tesla and Apple which will help shape near-term market sentiment.

Global financial market developments

- US and global equity averages were modestly lower.

- US and European bond yields were higher on the week

- The US Dollar Index moved to a multi-year low.

- Gold futures surged up to a new record high.

- Oil futures prices rallied, close to a multi-month peak.

Key this week

Central Bank Watch: It’s a busy week for central bank action, highlighted by the Federal Reserve’s Monetary Policy Statement, Interest Rate Decision, and Press Conference on Wednesday, where rates are widely expected to remain unchanged. The Bank of Canada will also announce its Policy Statement, Rate Decision, and hold a Press Conference on the same day, making Wednesday a key day for Global Monetary Policy updates.

Macro Data Watch: Macro data is relatively light this week, with the key releases to watch being the US PPI, German CPI, and Eurozone GDP, all scheduled for Friday.

Earnings Watch: US fourth-quarter earnings season gathers pace this week, with four members of the Magnificent Seven set to report, as Microsoft, Meta Platforms and Tesla release results on Wednesday, followed by Apple on Thursday. Elsewhere, notable updates from ASML ADR, Caterpillar, Boeing, Visa, Mastercard, Exxon and Chevron will add further colour across technology, industrials, financials and energy.

| Date | Major Macro Data |

| 01/26/2026 | US Durable Goods Orders |

| 01/27/2026 | US ADP Employment Change 4-week average, Housing Price Index and Consumer Confidence |

| 01/28/2026 | BoJ Monetary Policy Meeting Minutes; German Consumer Confidence; BoC Monetary Policy Statement, Interest Rate Decision and Press Conference; Fed Monetary Policy Statement, Interest Rate Decision and Press Conference |

| 01/29/2026 | EU Consumer Confidence, Business Climate and Economic Sentiment Indicator; US Initial Jobless Claims, Nonfarm Productivity, Factory Orders and Unit Labor Costs |

| 01/30/2026 | Japanese CPI, Retail Trade and Unemployment; German CPI, GDP and Unemployment; EU GDP and Unemployment; Canadian GDP; US PPI |

| Date | Major Earnings Data |

| 01/26/2026 | Nothing of note |

| 01/27/2026 | UnitedHealth; RTX Corp; Boeing; Texas Instruments; General Motors |

| 01/28/2026 | Microsoft; Meta Platforms; Tesla; ASML ADR; Lam Research; IBM; Amphenol; GE Vernova LLC; AT&T; Danaher; ServiceNow Inc; Progressive; Starbucks; ADP |

| 01/29/2026 | Apple; Visa A; Mastercard; Caterpillar; Thermo Fisher Scientifc; KLA Corp; Blackstone; Honeywell; Lockhead Martin |

| 01/30/2026 | Exxon Mobil; Chevron; American Express; Verizon |