Macroeconomic/ geopolitical developments

- U.S. and international equities ended the week broadly lower, with tariff uncertainty, weak economic data, and disappointing earnings driving the steepest U.S. losses since April and synchronized declines across European and Asian markets.

- Strong earnings from major US tech firms, led by AI-driven growth at Meta and Microsoft, boosted markets despite mixed results and cautious outlooks from Apple and Amazon, highlighting rising AI investments and cloud competition as key factors shaping the sector’s near-term outlook.

- The Fed kept rates steady in July as tariff-driven inflation pressures pushed core PCE above target and labor market signals softened, leaving markets eyeing a possible September cut but policymakers emphasizing patience.

- The U.S. finalized new trade agreements with key partners like the UK, Japan, South Korea, and the EU while imposing higher tariffs averaging 18% on many others, with these changes set to increase goods inflation and impact consumer demand as the new rates take effect on 7th August.

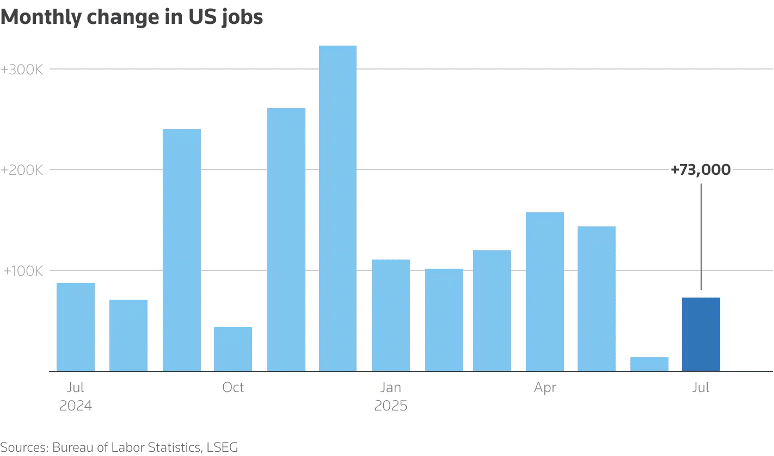

- The July report showed payroll growth of just 73,000 with sharp downward revisions to prior months, pushing unemployment to 4.2% and signaling a broad labor market slowdown that has boosted expectations for a Fed rate cut.

Global financial market developments

- US and global equity averages were notably lower.

- US and European bond yields were lower on the week

- The US Dollar Index rallied, before a sell off Friday.

- Gold futures sold off before a firm rebound higher Friday.

- Oil futures prices rallied through the week, then sold off Thursday-Friday.

Key this week

Central Bank Watch: The main central bank activities this week are the Bank of Japan Monetary Policy Meeting Minutes on Tuesday and the Bank of England Minutes, Interest Rate Decision and Monetary Policy Report on Thursday.

Macro Data Watch: Macro data is light this week, the main macro data releases to look out for are the Global Composite and Service PMI on Tuesday, EU Retail Sales on Wednesday and Canadian Jobs Report on Friday.

Earnings Watch: This week’s US Q2 earnings calendar is relatively light, featuring Berkshire Hathaway’s report on Monday, followed by Walt Disney and Uber Tech on Wednesday, and Eli Lilly on Thursday.

| Date | Major Macro Data |

| 08/04/2025 | EU Investor Confidence; US Factory Orders; UK Retail Sales |

| 08/05/2025 | BoJ Monetary Policy Meeting Minutes; Global Composite and Service PMI; EU PPI |

| 08/06/2025 | German Factory Orders; EU Retail Sales |

| 08/07/2025 | Chinese Trade Report; German Industrial Production; BoE Minutes, Interest Rate Decision and Monetary Policy Report; US Initial Jobless Claim, Nonfarm Productivity and Unit Labor Costs |

| 08/08/2025 | Canadian Jobs Report; US Consumer Inflation Expectations |

| Date | Major Earnings Data |

| 08/04/2025 | Berkshire Hathaway B; Palantir; MercadoLibre; Vertex |

| 08/05/2025 | AMD; Caterpillar; Amgen; Eaton; Arista Networks; Pfizer; BP |

| 08/06/2025 | McDonald’s; Walt Disney; Uber Tech; Shopify Inc; Applovin; DoorDash; Airbnb |

| 08/07/2025 | Eli Lilly; Gilead; ConocoPhillips |

| 08/08/2025 | Nothing of note |