Macroeconomic/ geopolitical developments

- US stocks pushed to fresh records led by gains in the S&P 500, Dow and small caps, while rising oil and precious metals and strong advances across Europe and Asia underscored broad-based optimism that the global bull market is rolling into 2026.

- Geopolitical tensions are rising as the US military’s capture of Venezuelan President Nicolás Maduro and assertions of interim control over the country’s governance and oil resources have unsettled global relations, while renewed US interest in acquiring or exerting influence over Greenland has sparked pushback from Denmark and other allies, reflecting broader strain in international alliances and strategic competition in key regions.

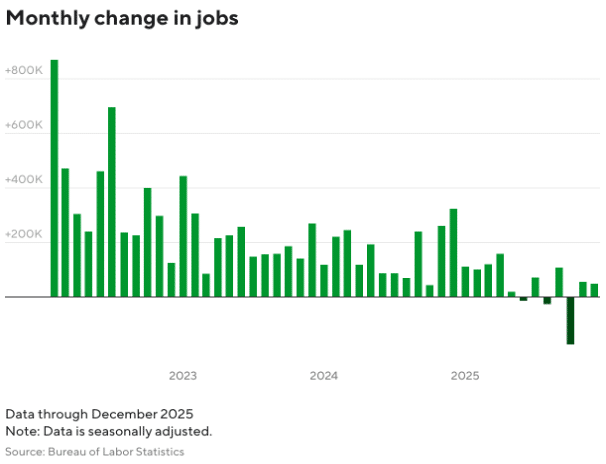

- The US Employment, ADP and JOLTS reports all point to a cooling labor market, with payrolls rising by just 50,000 in December, well below expectations, alongside subdued private-sector hiring and a drop in job openings. Together, the data underline easing demand for workers even as the unemployment rate edged slightly lower.

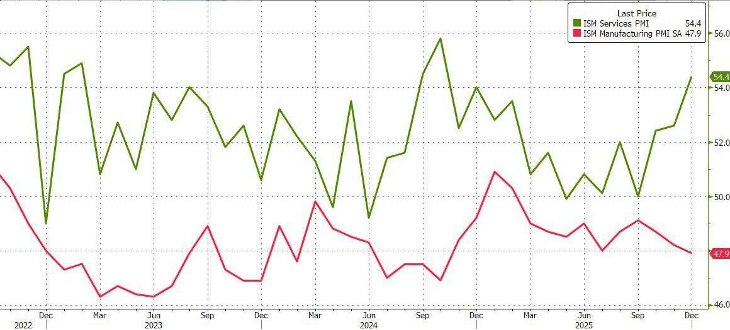

- December’s ISM data showed a split US economy, with manufacturing contracting for the 10th month at 47.9 amid weak production and employment, while the services sector expanded strongly to 54.4, supported by rising new orders and business activity.

- Investors this week will focus on December’s CPI release for signs of inflation trends ahead of the Fed’s January meeting, while the start of Q4 earnings season, led by major banks and including a key report from Taiwan Semiconductor, will provide insights into consumer health and broader economic momentum.

Global financial market developments

- US and global equity averages were lower, in some places hitting record levels.

- US and European bond yields were little changed, but slightly lower on the week

- The US Dollar Index moved higher.

- Gold futures surged higher, closing in on the record high.

- Oil futures prices rallied through the week, back within a multi-week range.

Key this week

Central Bank Watch: It is a relatively quiet week for central bank activity, attention will be focused on speeches from Fed, BoE and ECB members throughout the week.

Macro Data Watch: This week’s macro focus is on the US CPI report on Tuesday, with additional key releases including the UK Employment data the same day, US Retail Sales and PPI figures on Wednesday, and Chinese GDP on Friday.

Earnings Watch: US fourth-quarter earnings season gets underway this week, led by the major banks, with JPMorgan reporting on Tuesday, followed by Bank of America and Citigroup on Wednesday, and Goldman Sachs and Morgan Stanley on Thursday.

| Date | Major Macro Data |

| 01/12/2026 | EU Investor Confidence |

| 01/13/2026 | UK Retail Sales and Employment Report; US CPI (Dec), New Home Sales Change, Monthly Budget Statement and ADP Employment Change 4-week Average |

| 01/14/2026 | Chinese Trade Report; US PPI (Oct and Nov), Retail Sales (Nov) and Existing Home Sales Change |

| 01/15/2026 | Chinese Retail Sales and Industrial Production; UK GDP, Industrial and Manufacturing Production; EU Industrial Production; US Initial Jobless Claims |

| 01/16/2026 | Chinese GDP; EU HICP; US Industrial Production |

| Date | Major Earnings Data |

| 01/12/2026 | WaFd Inc; Platinum Group Metals; Lifecore Biomedical |

| 01/13/2026 | JPMorgan; Bank of New York; Delta Air Lines |

| 01/14/2026 | Bank of America; Wells Fargo&Co; Citigroup |

| 01/15/2026 | Taiwan Semiconductor; Morgan Stanley; Goldman Sachs; BlackRock |

| 01/16/2026 | Nothing of note |