Macroeconomic/ geopolitical developments

- US stocks rebounded strongly last week, with the Nasdaq jumping 3.9% to a record high as tech and growth shares led global markets higher, while Treasury yields ticked up, oil fell, and gold briefly hit a new peak.

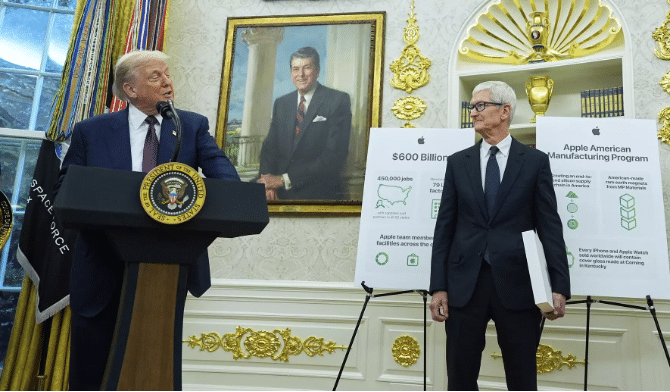

- Apple has pledged an additional $100 billion to its American Manufacturing Program, bringing its total U.S. investment to $600 billion over four years to expand domestic production, create 20,000 jobs, and build a resilient end-to-end tech supply chain while reducing reliance on overseas manufacturing.

- Following the end of the tariff pause on August 7, the U.S. raised import duties on goods from over 90 countries—some as high as 100% on semiconductors—causing near-term cost increases but prompting only a subdued market response amid hopes that trade talks may ease longer-term inflation risks.

- Markets now see nearly a 90% chance of a September Fed rate cut, driven by weaker labor data, dovish policymaker comments, and President Trump’s nomination of Stephen Miran, though internal divisions remain over inflation risks.

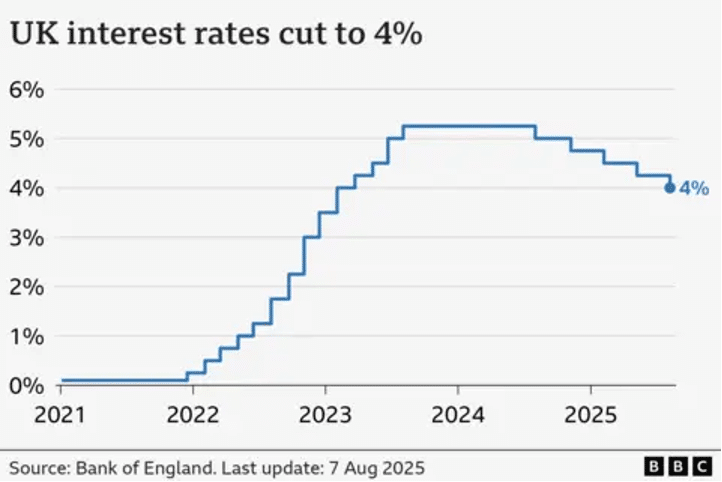

- The BoE reduced its key interest rate to 4% in a narrow 5–4 vote, citing slowing growth despite persistent inflation, prompting market caution and political debate over the move’s timing.

- Investors await Tuesday’s July US CPI report, expected to show a third straight monthly inflation rise, alongside key US data and Fed speeches, while Friday’s Trump–Putin summit in Alaska could influence markets amid efforts to broker a Ukraine ceasefire.

Global financial market developments

- US and global equity averages were higher.

- US and European bond yields were little changed, but slightly higher on the week.

- The US Dollar Index moved slightly lower for the week.

- Gold futures moved higher, closing in on the record high.

- Oil futures sold off 5% to a two-month low.

Key this week

Geopolitics Watch: President Donald Trump is set to meet Russian President Vladimir Putin in Alaska on Friday.

Central Bank Watch: Central bank activity is limited this week, with the key event being the Reserve Bank of Australia’s Monetary Policy Statement and Interest Rate Decision on Tuesday.

Macro Data Watch: This week’s key macro data releases include US CPI on Tuesday and US Retail Sales on Friday. Other notable reports are EU and UK GDP on Thursday, US PPI on Thursday, and the Michigan Consumer Sentiment Index on Friday.

Earnings Watch: US Q2 earnings season is winding down this week, with highlights including Cisco’s results on Wednesday and Applied Materials’ report on Thursday.

| Date | Major Macro Data |

| 08/11/2025 | UK Retail Sales |

| 08/12/2025 | RBA Monetary Policy Statement and Interest Rate Decision; UK Employment Report; US CPI |

| 08/13/2025 | German CPI |

| 08/14/2025 | UK GDP, Industrial and Manufacturing Production; EU Industrial Production and GDP; US PPI and Initial Jobless Claims |

| 08/15/2025 | Presidents Trump/ Putin meet in Alaska; Japanese GDP; Chinese Industrial Production and Retail Sales; US Retail Sales, Industrial Production and Michigan Consumer Sentiment Index |