Macroeconomic/ geopolitical developments

- Global equity markets ended the week lower and volatile as oil prices surged, pushing US crude oil to around $99 per barrel and Brent briefly above $100, heightening concerns over energy-driven inflation and economic growth. In the US, the S&P 500 fell 1.60%, the Nasdaq Composite declined 1.26%, and the Dow Jones Industrial Average dropped 1.99%, as rising energy costs and higher Treasury yields weighed on risk sentiment across global markets.

- The Middle East conflict has driven oil prices to multi-year highs, pushing US and European bond yields higher and reigniting fears of stagflation as growth slows and inflation rises. Even if the crisis eases, elevated energy costs could keep inflationary pressures persistent, limiting central banks’ ability to cut rates and sustaining market caution.

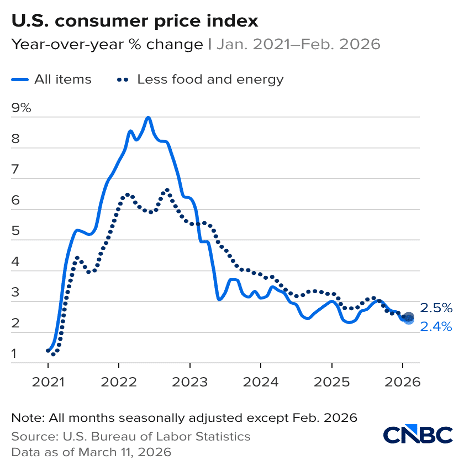

- US inflation data sent mixed signals, with February Consumer Price Index (CPI) matching expectations at 0.3% month-on-month and 2.4% year-on-year, while core CPI held at 2.5%, suggesting underlying price pressures are gradually easing. However, the Personal Consumption Expenditures (PCE) Price Index, the Federal Reserve’s preferred gauge, remained firmer, with core PCE rising 0.4% in January and 3.1% annually, indicating persistent inflation even as US fourth-quarter GDP growth was revised down to 0.7%.

- This week, markets focus on the Federal Reserve’s penultimate meeting under Chair Jerome Powell, as policymakers weigh sticky inflation, a softening labor market, and soaring oil prices driven by the Iran conflict. With the Strait of Hormuz effectively blocked, energy disruptions are adding pressure on inflation and growth, making Powell’s comments and updated projections critical for gauging the Fed’s next moves.

Global financial market developments

- US and global equity averages were lower.

- US and European bond yields were notably higher on the week.

- The US Dollar Index moved to a multi-month high.

- Gold futures were slightly lower in a consolidation range.

- Oil futures prices spiked to a multi-year peak.

Key this week

Central Bank Watch: It is a packed week for central bank activity, headlined by the Federal Reserve’s Monetary Policy Statement, Interest Rate Decision, and Press Conference on Wednesday. Other key events include the Reserve Bank of Australia’s policy update on Tuesday, the Bank of Canada’s decision on Wednesday, and back-to-back statements from the Bank of Japan, Bank of England, and European Central Bank on Thursday, followed by the People’s Bank of China’s Rate decision on Friday.

Macro Data Watch: Macro releases are relatively light this week, with key highlights including China’s Industrial Production and Retail Sales on Monday, the US PPI on Wednesday, and the UK Employment Report on Thursday.

| Date | Major Macro Data |

| 03/16/2026 | Chinese Industrial Production and Retail Sales; Chinese CPI; US NY Empire State Manufacturing Index, Industrial Production and Monthly Budget Statement |

| 03/17/2026 | RBA Monetary Policy Statement, Interest Rate Decision and Press Conference; US ADP Employment Change 4-week average and Pending Home Sales |

| 03/18/2026 | Japanese Trade Report; EU HICP; US PPI, Factory Orders and Interest Rate Projections; BoC Monetary Policy Statement, Interest Rate Decision and Press Conference; Fed Monetary Policy Statement, Interest Rate Decision and Press Conference |

| 03/19/2026 | BoJ Monetary Policy Statement, Interest Rate Decision and Press Conference; UK Employment Report; BoE Monetary Policy Summary, Interest Rate Decision and Minutes; US Initial Jobless Claims, Philadelphia Fed Manufacturing Survey and New Home Sales Change; ECB Monetary Policy Statement, Interest Rate Decision and Press Conference |

| 03/20/2026 | PBoC Interest Rate Decision; German PPI; Canadian Retail Sales; Fed Monetary Policy Report |