Macroeconomic/ geopolitical developments

- Global equities ended the holiday-shortened week mixed but resilient, with the S&P 500 and Nasdaq edging higher near record levels, Europe and China lagging, and Japan and Hong Kong advancing as investors weighed softer US jobs data, Fed rate-cut hopes, and ongoing growth concerns.

- Markets now widely expect the Federal Reserve to begin cutting rates at its September meeting (likely by 25 basis points) with two or more reductions possible by year-end as policymakers respond to a weakening labor market despite lingering inflation pressures.

- August ISM surveys showed manufacturing remained in contraction for a sixth month despite a rebound in new orders, while services activity strengthened to its highest level since February, highlighting resilience in consumer demand but ongoing pressures from costs, tariffs, and weak industrial output.

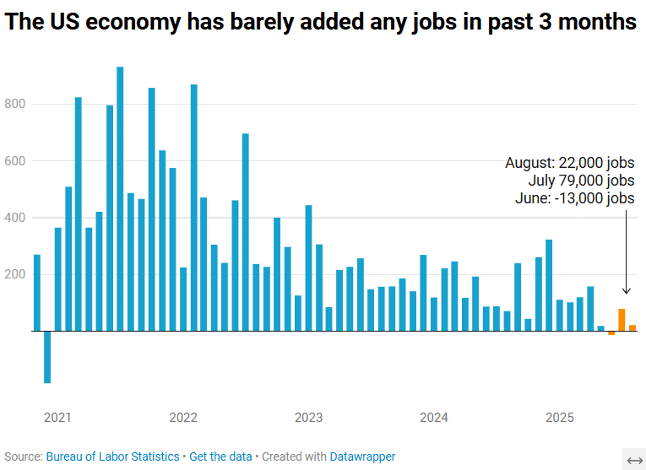

- US labor market data showed only 22,000 jobs added in August, alongside rising unemployment and weaker private payrolls and job openings, reinforcing signs of a slowdown and bolstering expectations for a Fed rate cut this month.

- Key inflation data in the US this week will help shape expectations for the Fed’s September 17 rate decision, while the ECB is widely expected to hold policy steady, with attention shifting to updated projections and political developments in Europe.

Global financial market developments

- US and global equity averages were higher.

- US and European bond were notably lower on the week

- The US Dollar Index moved to a multi-week low, closer to July’s multi-year low.

- Gold futures surged higher to a record high.

- Oil futures prices sold off, close to a multi-month low.

Key this week

Central Bank Watch: The spotlight this week falls on the European Central Bank, which will announce its Interest Rate Decision and hold a Press Conference on Thursday.

Macro Data Watch: Markets will be focused on the US CPI due Thursday, but attention will also turn to China’s inflation data and the US PPI on Wednesday, and Michigan Consumer Sentiment to close out the week Friday.

| Date | Major Macro Data |

| 09/08/2025 | Japanese GDP; Chinese Trade Report; German Industrial Production |

| 09/09/2025 | UK Retail Sales |

| 09/10/2025 | Chinese CPI and PPI; US PPI |

| 09/11/2025 | US CPI; ECB Monetary Policy Statement, Press Conference and Interest Rate Decision |

| 09/12/2025 | German HICP; UK GDP, Industrial and Manufacturing Production; US Michigan Consumer Sentiment Index |