Macroeconomic/ geopolitical developments

- Global equities fell for a third week as mounting doubts over stretched AI valuations drove steep declines in tech-heavy US indices and sparked broad global sell-offs across, alongside rising volatility, falling Treasury yields, and further Bitcoin losses.

- Market expectations for a December Fed cut whipsawed last week as missing economic data and sharply conflicting signals from policymakers left investors uncertain about whether the central bank will ease again, with rate-cut odds sliding from near certainty to only 30% before rebounding above 70% on Friday.

- Nvidia posted blockbuster results and a strong outlook driven by exceptional AI-chip demand, but despite an initial surge, its shares reversed and closed lower as investors questioned lofty AI valuations and the durability of tech-sector momentum.

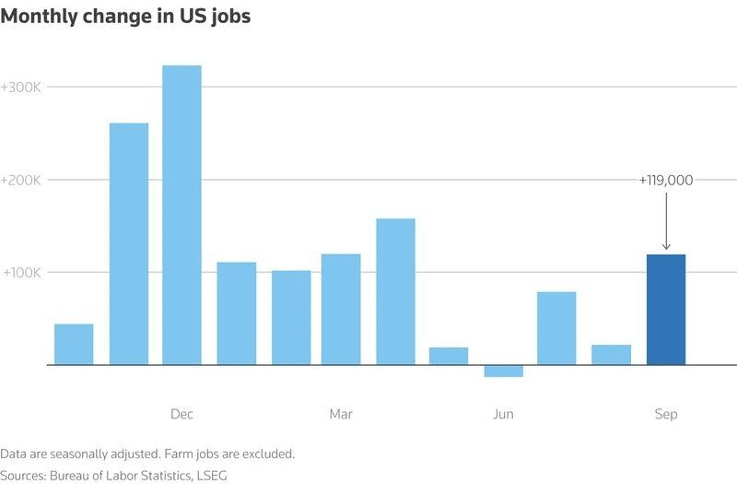

- The long-delayed September report showed stronger-than-expected payroll gains of 119,000 but a rising unemployment rate to 4.4%, reflecting conflicting signals in the labor market ahead of the Fed’s December meeting.

- A shortened trading week puts heightened attention on the delayed September Retail Sales report and November Consumer Confidence, with both set to guide market expectations for holiday spending.

Global financial market developments

- US and global equity averages were notably lower.

- US and European bond yields were slightly lower on the week

- The US Dollar Index moved higher, close to a multi-month high.

- Gold futures were little changed on the week.

- Oil futures prices moved lower, close to a multi-month low.

Key this week

Central Bank Watch: Central bank activity is quiet this week, though markets will watch Fed speakers in their last week before the blackout period.

Macro Data Watch: With the US government shutdown now lifted key US data includes September PPI, Retail Sales and Consumer Confidence on Tuesday. Notable non-US releases are German Retail Sales and CPI, and Canadian GDP, all released on Friday.

US Thanksgiving Holiday: Thursday 27 and Friday 28 November sees the US Thanksgiving holiday observed, with cash markets closed Thursday and a half day Friday, plus partial days for futures markets on both days.

| Date | Major Macro Data |

| 11/24/2025 | Nothing of note |

| 11/25/2025 | German GDP; US PPI (Sep), Retail Sales (Sep), Consumer Confidence (Nov) and Housing data (Sep) |

| 11/26/2025 | UK Budget; US Durable Goods Order (Sep) and Initial Jobless Claims |

| 11/27/2025 | US Thanksgiving holiday, cash markets closed, partial day for futures; German Consumer Confidence; EU Consumer Confidence |

| 11/28/2025 | US Thanksgiving holiday, half day for cash and futures markets; German Retail Sales, CPI and Unemployment; Canadian GDP |