Macroeconomic/ geopolitical developments

- US and global equity markets declined over the week as renewed concerns over elevated AI-driven technology valuations weighed on major indices, with tech and communication stocks leading losses in the US and similar caution spreading across European and Japanese markets, even as Chinese equities found support from easing US–China trade tensions.

- The US government shutdown has entered its sixth week (longest in history), with political gridlock halting federal funding, disrupting key public services and data releases, straining households reliant on government pay or support, and adding to economic and market uncertainty as no clear resolution is yet in sight.

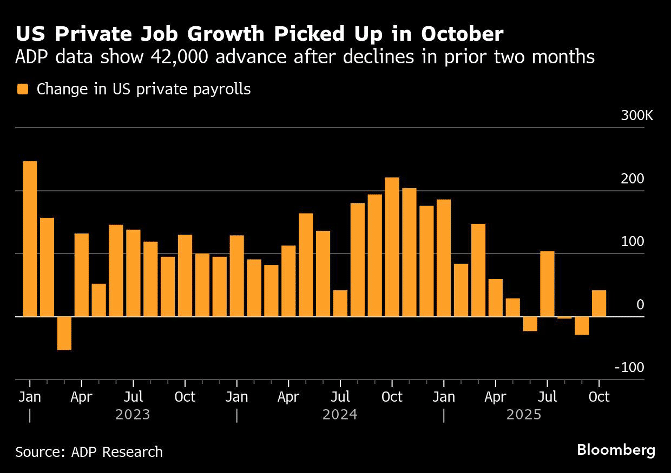

- October private-sector data showed modest job gains concentrated in large firms, while small businesses and key sectors shed workers, signaling a cooling US labor market amid persistent economic uncertainty and early impacts of AI adoption.

- October’s ISM data showed a rebound in services activity while manufacturing contracted for the eighth straight month, reflecting overall economic resilience tempered by weak employment and subdued business confidence amid ongoing data gaps from the government shutdown.

Global financial market developments

- US and global equity averages were notably lower.

- US and European bond were choppy and little changed.

- The US Dollar Index moved to a multi-month high, before a setback.

- Gold futures were in a narrow range, sideways consolidation.

- Oil futures prices dipped through the week.

Key this week

Central Bank Watch: It is a relatively quiet week for central banks, but markets will be watching speeches from Fed, ECB and BoE officials throughout the week for policy signals.

Macro Data Watch: With the US government shutdown now the longest on record, US economic data remains limited, and although CPI is scheduled for release on Thursday, followed by PPI and Retail Sales on Friday, these are unlikely to be published, unless there is a shutdown breakthrough. Key non-US data releases include the UK Employment Report on Tuesday, UK GDP on Thursday, and both EU GDP and Chinese Retail Sales on Friday.

Earnings Watch: The US earning season is slowing down, attention this week turning to results from Cisco on Wednesday, followed by Walt Disney and Applied Materials Thursday.

| Date | Major Macro Data |

| 11/10/2025 | Chinese CPI and PPI; EU Investor Confidence |

| 11/11/2025 | UK Retail Sales and Employment Report; US ADP Employment Change (4-week average) |

| 11/12/2025 | German HICP |

| 11/13/2025 | Australian Employment Report; UK GDP, Manufacturing and Industrial Production; EU Industrial Production |

| 11/14/2025 | Chinese Retail Sales and Industrial Production; EU Employment Change and GDP |