Macroeconomic/ geopolitical developments

- Major U.S. and global stock indexes rose last week, driven by strong corporate earnings, easing trade tensions, and stimulus hopes, with the S&P 500, Nasdaq, and MSCI World Index nearing or hitting record highs.

- Despite a positive call between Presidents Trump and Xi, renewed tensions and stalled negotiations have cast doubt on the fragile U.S.-China trade truce, raising fears of renewed escalation.

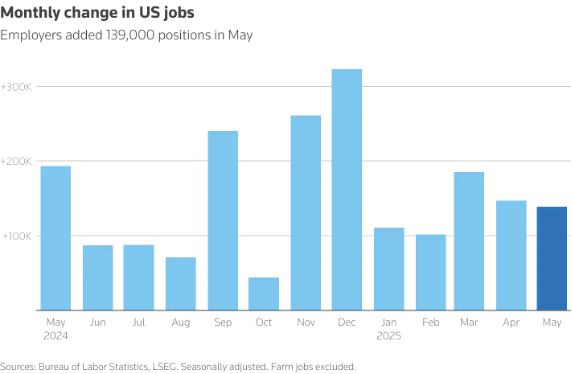

- The U.S. labor market added more jobs than expected in May, with steady unemployment and rising job openings signaling resilience despite signs of cooling and ongoing economic uncertainty.

- Both U.S. manufacturing and services sectors unexpectedly contracted in May, highlighting weakening demand, persistent inflationary pressures, and growing uncertainty amid trade and policy volatility.

- The European Central Bank delivered its eighth rate cut since mid-2024, lowering the deposit rate to 2% amid cooling inflation and trade pressures, while signaling a possible pause as policymakers adopt a data-driven approach.

- Markets are bracing for Wednesday’s CPI report, which could sway Fed policy ahead of its June meeting, as investors weigh the inflation impact of tariffs and fragile trade dynamics.

Global financial market developments

- US and global equity averages moved to multi-week/-month/ all-time highs.

- US and European bond yields were higher on the week

- The US Dollar Index marked time in consolidation mode.

- Gold futures were also little changed on the week.

- Oil futures prices were higher at multi-week highs.

Key this week

Central Bank Watch: Central bank activity is light this week with Fed officials in their blackout period before the June meeting, with the main focus on speeches from ECB members throughout the week.

Macro Data Watch: The main macro data release this week is the US CPI data on Wednesday. Some other releases of note are the UK GDP data and US PPI data both released on Thursday and the US Michigan Consumer Expectations and Sentiment Index released on Friday.

Earnings Watch: As Q1 2025 US earnings come to a close, this week’s main earnings are from GameStop, Oracle, and Adobe which highlight a sparse week of quarterly releases.

| Date | Major Macro Data |

| 06/09/2025 | Japanese GDP; Chinese CPI, PPI and Trade Report |

| 06/10/2025 | UK Retail Sales and Jobs Report |

| 06/11/2025 | US CPI |

| 06/12/2025 | UK GDP, Industrial and Manufacturing Production; US PPI |

| 06/13/2025 | German CPI; EU Industrial Production; US Michigan Consumer Expectations and Sentiment Index; US Consumer Inflation Expectations |