Macroeconomic/ geopolitical developments

- The S&P 500 fell 0.44%, the Nasdaq Composite dropped 0.95% and the Dow Jones Industrial Average declined 1.31% for the week amid AI and trade concerns, while February saw the S&P 500 lose 0.86% and the Nasdaq slide over 3%, even as the Dow edged up 0.17% to extend its winning streak, with defensives outperforming and Treasury yields moving lower.

- Investor fears over AI-driven disruption have pressured US equities, hitting software, financial, and real estate sectors, while a speculative Substack post from Citrini Research, warning of mass white-collar job losses and economic strain by 2028, has intensified market volatility despite debate over the scenario’s realism.

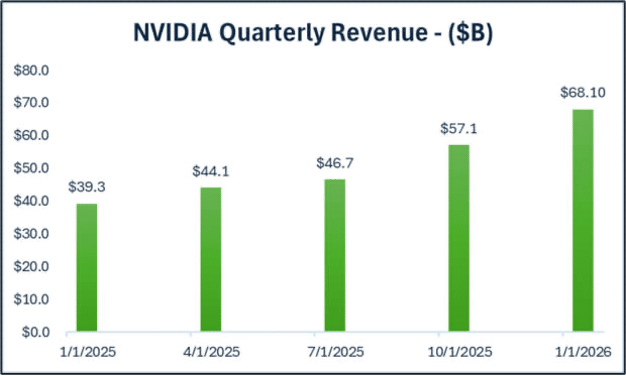

- Nvidia reported a standout quarter with revenue surging 73% year-on-year to $68.1 billion, data centre sales up 75% and upbeat guidance of around $78 billion, yet the stock fell more than 5% as investors grew wary over stretched valuations, the durability of AI spending and uncertainty surrounding its potential partnership with OpenAI.

- The United States and Israel launched a large-scale joint offensive against Iran, killing Supreme Leader Ali Khamenei and senior officials in strikes targeting nuclear and military infrastructure, prompting Tehran to retaliate with missiles and drones aimed at Israel and US bases across the Gulf, fuelling fears of wider regional escalation and disrupting global markets and oil shipments.

- Global PMI surveys will provide an early read on the strength and regional divergence of economic activity, while Friday’s US Non-farm Payrolls report will test whether January’s hiring surge was sustainable, shaping expectations for growth, inflation and the next move from the Federal Reserve.

Global financial market developments

- US and global equity averages were lower.

- US and European bond yields were lower on the week.

- The US Dollar Index moved to a multi-year low, before a bounce Friday.

- Gold futures pushed higher on the week.

- Oil futures prices rallied to a multi-month high.

Key this week

What’s Ahead

Central Bank Watch: Central bank activity is light this week, with the spotlight on scheduled remarks from officials at the European Central Bank, Federal Reserve and Bank of Japan throughout the week.

Macro Data Watch: The focus this week will be on Global PMI readings due Monday and Wednesday, alongside the US Jobs Report on Friday. Additionally, attention will be on EU HICP, Retail Sales and GDP data, as well as US Retail Sales.

Earnings Watch: US fourth-quarter earnings season is coming to an end, with standout updates expected from Target on Tuesday, Broadcom on Wednesday and Costco on Thursday.

| Date | Major Macro Data |

| 03/02/2026 | Global Manufacturing PMI; German Retail Sales |

| 03/03/2026 | Japanese Unemployment Rate; EU HICP |

| 03/04/2026 | Global Composite and Service PMI; EU PPI and Unemployment Rate; US ADP Employment Change |

| 03/05/2026 | EU Retail Sales; ECB Monetary Policy Meeting Accounts; US Initial Jobless Claims, Nonfarm Productivity, Unit Labour Costs and Challenger Job Cuts |

| 03/06/2026 | German Factory Orders; EU Employment Change and GDP; US Retail Sales and Job Reports; Fed Monetary Policy Report |

| Date | Major Earnings Data |

| 03/02/2026 | Nothing of note |

| 03/03/2026 | Target; Best Buy |

| 03/04/2026 | Broadcom |

| 03/05/2026 | Costco |

| 03/06/2026 | Nothing of note |