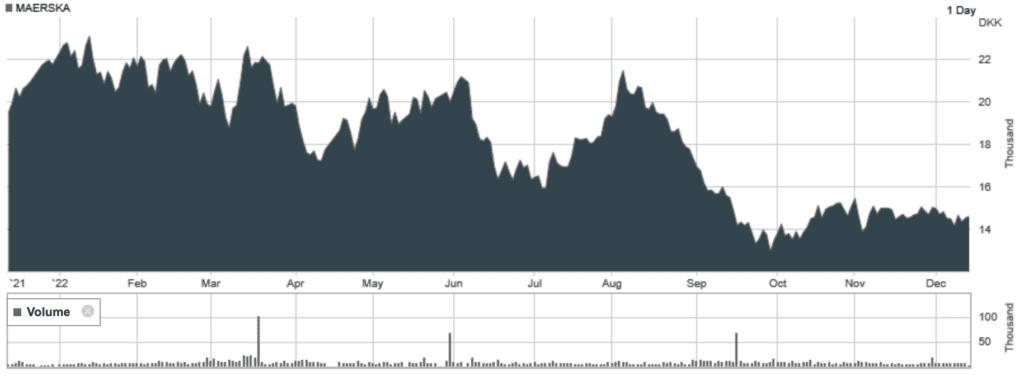

All too often we think of “the shipping industry” without thinking it through properly – it’s actually a series of different industries. Precisely because it is that series different parts of shipping can be at entirely different points in the cycle. For example, Moller Maersk (NASDAQ: MAERSKA) (LON: 0O77) did very well out of the container chaos that followed lockdown. But as we can see from the container freight index that boom has largely disappeared – we’re back to container rates being what they were several years ago. The easy profits generated by lack of supply (it was really that all the containers were stuck in Europe, not in the Far East where they were needed) have gone that is.

Well, OK, these things happen. Cycles come and go in sectors and in shipping more than most. At any one time the supply of shipping is largely fixed. Changes in the fleet come from the retirement and scrapping of vessels and the building of new ones. Fleet capacity can be expanded, a bit, by delaying scrapping but it takes several years to build new ones. So, prices vary wildly as in the short to medium term highly variable demand meets a near fixed supply. It’s only in that long term that supply can be changed.

But precisely because shipping is a series of different markets this return of the container market to normality doesn’t mean the same for the others. We don’t, in fact, really have a “general shipping fleet” anymore. We have bulk cargo ships (grain, possibly minerals and so on), tankers, container and so on. A ship built and specialised for one of those markets cannot be shifted across into one of the others. This means that supply and demand can be wildly different in different sectors.

Take, say, Navigator Holdings (NYSE: NVGS) which largely runs LNG (liquefied natural gas) tankers. Given the Russian events this market is not just booming it’s entirely booked out. It’s not just the increase in European demand for LNG, there’s a restriction on how much can be unloaded in Europe at any one time – to the point that stuff is being unloaded in Wales then piped to France etc. So, LNG ships are sitting off Europe – racking up daily rentals – awaiting the ability to unload. This particular sector of the shipping business is booming.

Now there’s another factor about to hit a third part of the market. That idea of a price cap upon Russian oil. This is, if we’re frank about it, a fairly stupid idea – a tax upon the import of Russian oil would both have raised revenue and also done the same job, lowered the price of Russian oil. But there we are, that’s politics. The thing is though this is going to lead to a rerouting of much of the world’s oil trade.

Russian oil will still be pumped, still be exported and still be used somewhere. It’s just that the European places which used to take it won’t. Instead, Europe will be feeding off Latin American, or African, or even Far East, oil. The Russian oil will be going to those places which aren’t imposing the price cap – those places that Latin, African and Far East oil used to go to. Given that the earlier distribution system was optimised for time and distance at sea the new one will not be. That requires more tanker capacity – each journey will now require more days at sea, that means we need more sea days of tankers. But supply, as above, in the short to medium term is fixed. So, prices are going to rise. As they already have done in anticipation in fact.

This is all on top of the previous bans on imports of Russian refined fuels – diesel and so on – which is affecting that part of the shipping market. So, stocks like DHT Holdings (NYSE: DHT) are worth looking at.

The point here is not to say that any of the above are great trades – nor bad ones in the case of Maersk. It is though to insist upon two things. Firstly, shipping is not some monolithic industry, it’s made up of separate parts. While those parts are all subject to some of the same economic constraints – near fixed supply in the short term, therefore wildly variable pricing, for example – they also operate entirely differently. It’s entirely possible for one sector – containers – to be on the downward slope of the price curve while tankers are on the upward. Secondly, factors like the price cap on Russian oil can make prices vary wildly – and as traders we like that. For trading is that process of gaining from price changes.

Given the complexity and fragmentation of the markets it’s necessary to do the homework to construct a winning position. But they are there, given that economic structure and the interference of the real world in the trade.