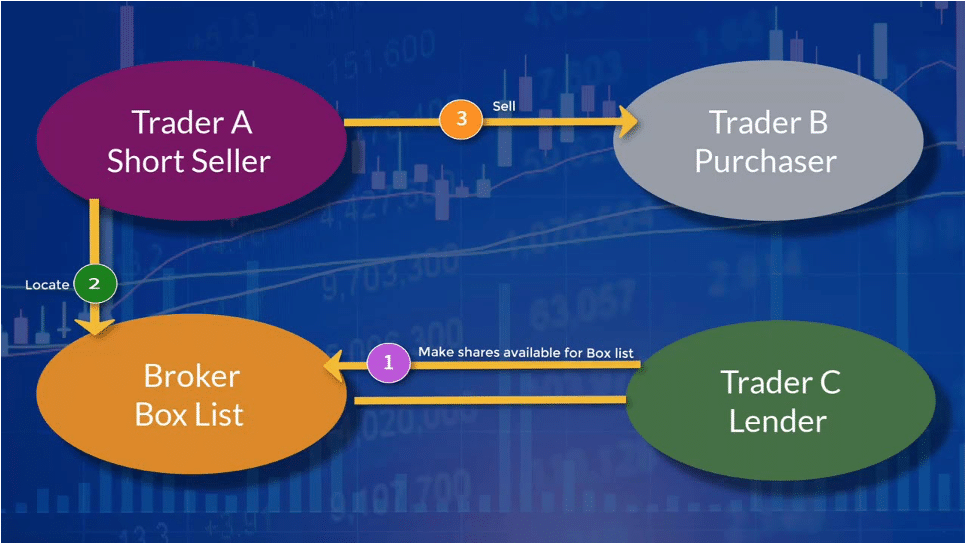

The Securities and Exchange Commission over in the US has decided that short selling is one of these nefarious attacks upon the integrity of the markets. At least that’s the usual Democratic Party response to the very idea of short selling. Which is, as we all know, selling something now in the hope of being able to buy it back cheaper in the future. Naked short selling is not really allowed – you have to borrow the stock or bond to be able to short sell it. You also pay a fee for doing so.

People don’t understand short sales

The misunderstanding of many is that there’s something wrong with the whole process – markets should be about investing, right? So therefore, this is just speculation and shouldn’t be allowed. But as Robert Shiller got his share of the Nobel for pointing out, markets aren’t, in fact, about investing. Financial markets are about the price at which investing should be done. We’ll only find the correct prices if those who think a price will fall are also able to trade their position. This is why Shiller’s proposal about the housing market was – in 2008, yes – that it should be possible to go short housing. Not because that would have helped in 2008, but because it should have prevented the price run up in 2004-07 and that movie, The Big Short, would never have been made.

OK, so some think that short selling is the very devil, Gary Gensler is from that wing of the D Party, therefore we’ve got new rules. But the new rules won’t make much difference, if any. There will be a short enough period – in the New Year when the wake effect – of adaptation to them. For what is going to happen is just that those going short will be reported. It won’t even be the short positions reported. Rather, the people lending out stock so that it can be shorted will have to report their lending the next day.

Short selling is entirely common

Short selling does happen in near all stock markets (and bond markets) and the economic effect is much like a put option or taking the downside of a future. It’s also possible to create much the same position in stock futures or even with contracts for difference brokers. Which is why short selling as an actual thing isn’t the problem that so many seem to think it is. If we’ve many ways of taking the same economic position – this is going to go down – then the existence or not of one more such method doesn’t really matter. Now, really, do the specific rules that are going to be in place.

Different markets do have different amounts of short selling, true. It’s much more important in New York than it is in either London or Australia for example. At the moment of writing the biggest short in London is ASOS, at 7.1% of the total issuance lent out. In Australia it’s Pilbara Minerals at 12.1% and it’s entirely normal to see some dog of a stock with a 40% short position. Actually, one of the funs at GameStop was precisely that the short position was more than the free float – not more than total issuance, but more than that held by non-strategic holders.

Ah, but the short squeeze

The grand danger of going short is the short squeeze, where some buying starts, this breaks the financing of some of those who have sold short, they have to buy to cover and close out their position. That buying then ticks the price up again, causing the same pain to more short sellers and so on up to, well, in theory an infinite price. There have even been examples where that theory nearly came true. At one point Porsche had more than 100% of VW via both stock and derivatives, meaning that those short should – again in theory – have had to pay an infinite price to close their positions. At which point someone sits everyone down around a table and forces reasonable to excessive, but not infinite, losses on the losers.

This is also why going short of a stock is not recommended for the retail investor – the losses are in theory infinite. Betting that the price will go down, via derivatives, CfDs, fine, but maybe not actively short the stock.

But, because enough Democrats don’t understand all of this they’ve long been against short selling. Thus, the change in the SEC rules. Those changes are, really, just that more information has to be provided faster about how much is short. The new information release will be a little more than London currently imposes – a daily report instead of within three days.

The new short rules are pretty milquetoast

But that’s pretty much it. Nothing to get very excited about, whatever we might see in the papers about it. A low volume stock, or a microcap, that we want to bet on going down directly short selling the stock might be the only way to do it (no stock futures on it say) and it’s an entirely valid if risky technique. And one of the ways that we can prove that the new SEC rules are a bit of not very much is that as the investor going short nothing will have changed. It’s the stock lenders, not short sellers, who have to report. Big hedge funds must report more directly.

In effect, one of those examples where lots of political pressure lead to not very much by economic or market standards.