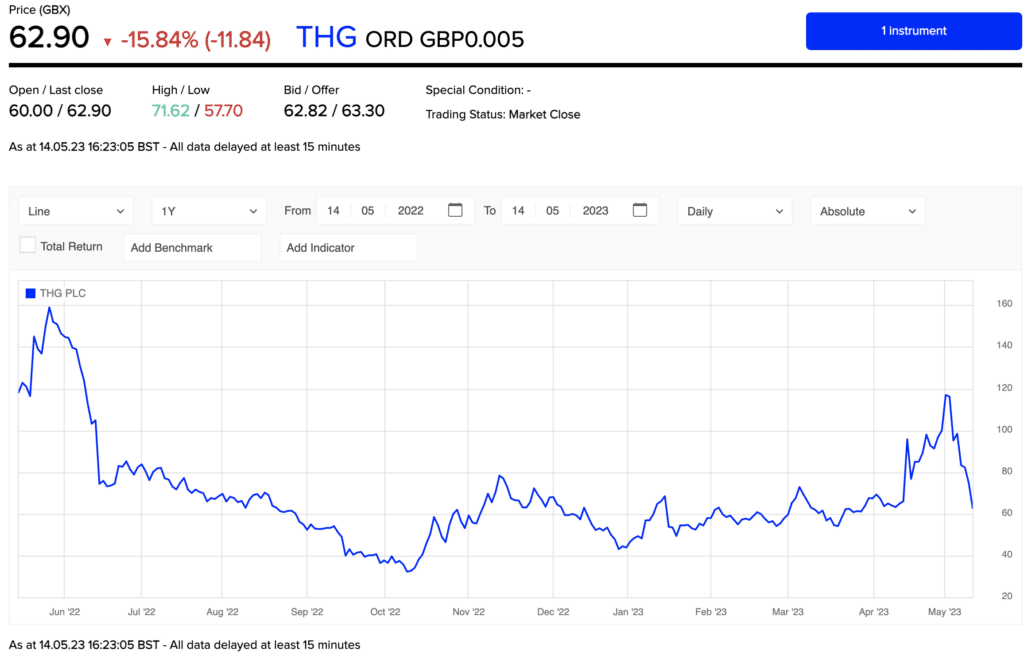

THG (LON: THG), what was formerly known as The Hut Group, fell near 50% last week. Only part of this was about the business itself, a goodly portion was really about Matt Moulding and his ideas. All of which does then lead to the question, well, what next?

117p to 62p really is near 50%, the sort of performance that would have many to most CEOs packing their briefcase – or at least worrying that they’d need to. This isn’t going to happen as Moulding is CEO, founder and controlling shareholder. But that then means that shareholders are locked into the performance of that one man. And it’s long been suspected that Moulding, while clearly an exceptional entrepreneur, perhaps isn’t the right person to be running a publicly listed company.

The actual business results aren’t looking good at THG

The start of the share price fall was the annual results. Revenue is up, yes, gross margins look good – and losses exploded out to half a billion – which is some 20% or so of gross revenue. It’s clearly possible to describe this as a success as management does so but it’s a little more difficult to think of it as such. After all, the point of a business is to produce cash for investors to enjoy – profits and dividends.

The real problem here, from the investor point of view, is that management doesn’t seem to be doing quite what investors would like – pursuing profit rather than investment into potential growth. Well, that’s usually solvable, get new management in. But that then runs up against Matt Moulding being secure in his position.

So, maybe a takeover of THG would work?

Well, OK, but what about a takeout? New investors come in and by buying the equity make themselves in charge of Moulding? That has indeed long been discussed. There have been a number of private equity approaches. But that then brings us to the second event which depressed the THG share price. A rejection of an indicative approach by Apollo. The announcement on that is here. All the usual stories, the bid’s too low, undervalues the company, we’ll be right soon enough and so on. It’s as if there’s a template pulled out when rejecting a bid.

For what happened after those results was the revelation that Apollo was thinking of just such a takeout bid, that drove the share price up again only to drop that near 50% when the news came through of the rejection.

But Matt Moulding

But that’s not all. Moulding gave a more direct view of matters on LinkedIn. Which contains, shall we say, interesting snippets. Like the claim that Numis led short attacks against THG when they failed to be made the nominated broker. Moulding has form here, blaming shorts for all sorts of things. Not realising – or not caring to realise perhaps – that short selling is an entirely valid tactic, one that informs the rest of the market of views held. Provides clarity to the market about investment views in fact.

But then his past complaints about short sellers – among other things – are precisely what has The City mulling whether he’s quite the guy to be running a public company in the first place. Entrepreneur, sure, he’s one of those. But the public face of a listed company not so much perhaps.

The Financial Times has been having some fun with THG claims about the future. They seem, umm, rather hopeful. General comment on the LinkedIn post is “lashing out”. Which isn’t, again, quite what we expect from someone running a public company.

There’s no easy solution to the THG problem

The problem from the point of view of investing here is that there’s a blocking majority on what is the obvious – short term – solution. Which is a change of ownership and with it a change in management. But the current management – Moulding – is that blocking majority. So that standard solution really just isn’t available, As the rejection of the private equity bid from Apollo shows. The only alternative is that the business actually starts to hum along in generating a decent pr0ofit. Which, well, opinions are divided on how that’s going to go.

It is possible to think that it’s all work out and that thus the current share price is just a buying opportunity. But that the price is so low is also evidence that an awful lot of other people don’t think so. What is almost certainly true is that there’s not going to be a swift change in this situation. That’s just the way it works if we can’t hope for a bid or change of control but have to wait for the business performance to shine through – if it does.