Brine, pegmatites, clay, spodumene, carbonate, hydroxide; these terms are quite simple to understand if you can spare five minutes.

As an investor and analyst in battery metals, commodities, and equities, a very common question in my inbox is whether it is possible to invest directly into lithium. You can physically buy gold, silver, and copper; trade oil and gas futures, and if you really wanted to, buy a passel of lean hogs.

You might think that it stands to reason that you could directly buy lithium, or at the very least trade the underlying commodity. This will likely become a possibility at some point in the future — but there are several hurdles to cross before this can happen. At the moment, you’re limited to blue chip lithium shares or the small caps.

Let’s dive in.

Lithium: speciality chemical

To start with, I have covered the bull cases for lithium, alongside copper and graphite, in depth.

To please Google: Can you invest in lithium directly? The short answer is NO. You cannot directly invest in lithium, or the underlying commodity.

Lithium is very different to other commodities. Like uranium, it is extremely reactive — if your science teacher ever demonstrated what happens when a lump of sodium gets dropped into a bucket of water — then you get the general idea.

Lithium usually has to be stored in an inert substance, often oil. Overall, it’s extremely expensive to mine, store, and transport. For context, stockpiles of pig iron in Ukraine will happily sit in a field for years without much damage.

In addition to this issue, lithium from different sources is completely non-fungible. Fungibility essentially means that all of a certain item are mutually interchangeable; one pound sterling can be swapped for another, or one Bitcoin can be swapped for another — they are both fungible.

Gold and copper are also fungible — you can mine gold in an Australian mine, pan for gold in a river in the US, or dig a nugget out of a field in Africa, and the gold will be chemically close to identical.

By contrast, different sources of lithium are non-fungible, leading many analysts to characterise the silvery-alkali metal as a ‘speciality chemical’ rather than a commodity.

Lithium comes from three primary sources (excluding recycling):

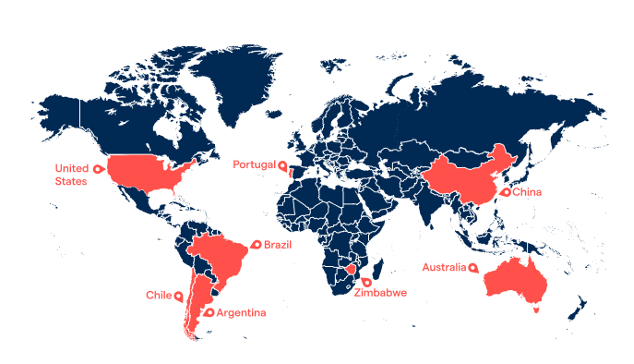

- Lithium-rich brine — a concentrated saltwater solution, found where ancient seas have evaporated over millions of years leaving behind concentrated lithium salts. The most significant deposits are found in the South American lithium triangle, covering Argentina, Chile, Brazil, and Bolivia.

- Lithium-bearing pegmatite — an igneous hard rock formation (spodumene is the usual lithium-bearing mineral found in pegmatites). Significant deposits are found in Australia, DROC, and Zimbabwe.

- Lithium clay deposits — which hold lithium minerals such as jadarite and hectorite. This is less popular, but a notable deposit is the Jadar deposit in Serbia.

As you can see, not only are there three different types of deposits, but there are also different types of lithium-bearing minerals, from which you extract different types of lithium.

The two key types of lithium sold at market are:

- lithium carbonate

- lithium hydroxide

Lithium hydroxide vs lithium carbonate

The next few concepts absolutely critical to understanding lithium and the lithium markets.

- Lithium hydroxide is the ‘premium’ product that the market wants. While lithium is used in dozens of products from antidepressants to heat resistant glass, the vast majority is used and will be used within batteries for EVs.

- And it is lithium hydroxide that the market wants because for complex chemical reasons, it’s far better for battery manufacturing than lithium carbonate.

- Lithium extracted from spodumene, and other hard rock sources, can usually be turned into either carbonate or hydroxide, while lithium extracted from brine must first be turned into carbonate before being converted into hydroxide.

- This is the reason why China wants lithium from Australia and Africa — domestic Chinese brine-sourced lithium from Sichuan is costly to process into battery-quality product. Spodumene lithium requires one round of processing, so is much cheaper.

It’s worth noting that there are huge technological strides being made in an attempt to bridge this gap, but the fundamental chemistry means that at present, hard rock producers’ costs are less than half that of brines — and deliver a product which is cheaper to manufacture into batteries.

This explains the power that Australia has in the lithium market — while it has less lithium than in the South American triangle, virtually all of Australia’s lithium is derived from spodumene — and China remains relatively happy to buy at premium prices. At least, until African mines start delivering.

Understanding SC6 and lithium hydroxide

Spodumene concentrate 6 (or SC6), is a high-purity lithium ore with circa 6% lithium content, produced as a raw material. SC6 quality can be as low as 5.5%, but no lower.

It generally takes about 7.5 tonnes of SC6 to create one tonne of lithium hydroxide. Hydroxide sells for circa 10-11x more than SC6, so there is a healthy profit margin for large-scale processors. SC6 is commercially valuable because it is currently scarce, and the higher purity means a processor can create more lithium hydroxide more economically.

The takeaway is that if you are looking for the best battery-grade lithium, its SC6 from a hard rock mine.

Lower grades, such as SC4, are not worthless — but higher processing costs to get the correct hydroxide quality cut into margins, and the end result is often simply not as good.

Can lithium be replaced?

While there are efforts being made to create mass market hydrogen-powered cars, these will likely take many years to come online. It is true that some EVs still use nickel, as lithium shortages and the expense of manufacture make the metal much cheaper to use.

However, neither nickel nor any other element is likely to replace lithium. If you assume that the EV revolution is unstoppable — and not everyone agrees with this — then only lithium will work. Even though nickel batteries last for more charging cycles and can be recycled profitably, the chemical reality is essentially impossible to change.

Lithium is the least dense metal, and by far the most effective for conducting electricity. Lithium-ion batteries charge much faster, and their maximum charging capacity is less affected after each charge.

Nickel has almost half as much energy density, so altogether this means much more is needed to power an EV. It also gets hot quickly so can only operate with a cooling system — another weight problem.

Will there be a lithium spot price eventually?

I think so — especially as more producers come online and traders clamour for a way to lose money quickly.

For context, oil is now thought of as fungible and therefore it is very easy to trade oil in myriad different ways. However, in practice different types of oil vary hugely in chemical makeup, grading, sulphur, viscosity, lightness, sweetness, refinement needs, and usability.

Consumers can blend different grades to achieve a desired standard mixture, and benchmark prices have created an integrated pricing structure in the international markets that means most view one barrel of oil as good as any other.

As lithium gains in popularity, it’s not hard to see an enterprising individual looking to set up a spot ETF that somehow tracks lithium similar to Yellow Cake’s tracking of uranium. Further forward, money always finds a way.

The window of opportunity

Even after the recent correction, lithium prices remain elevated. With demand for the metal — and in particular spodumene — set to soar, lithium shares and ETFs will likely continue to rise in value.

However, just as with oil, the cure for high prices is high prices. There is going to be a period of perhaps five years where lithium spikes again and investors get huge payouts. However, the majors are finally onto the case now, and increasing supply in the later 2020s could see lithium fall in price as supply catches up to demand.

This article has been prepared for information purposes only by Charles Archer. It does not constitute advice, and no party accepts any liability for either accuracy or for investing decisions made using the information provided.

Further, it is not intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.

Hi Charles, great, informative article, thank you. Are there some companies that you recommend taking a look at??

have a great day,

Billy Betlach

847-601-5855

Hi Billy,

Blue chips: Pilbara Minerals and Albemarle

Mid-tier: Ioneer

Small-caps: Premier African Minerals, Kodal Minerals, & First Class Metals — though many more on the watchlist.

You can find my portfolio with all my work at charlesarcher.co.uk — with coverage of many of the most popular lithium shares. I suggest you check out investingstrategy.co.uk as a first port of call.

Not financial advice.