Echoes of early 2022 whisper across time into the wheat markets. What happens next?

On 24 February 2022, Russia invaded Ukraine. Or, more accurately, a war that has been raging since at least 2014 intensified. Putin’s failed attempt to take Kyiv within days would likely have had little effect on the commodities markets if he had succeeded.

Instead, when it became apparent that the war would become a protracted affair, the commodities markets went haywire. Gold, copper, iron, oil, gas, nickel, platinum, palladium — Russia is a globally important exporter of almost every important hard commodity — rocketed, and a combination of two-way sanctions and export uncertainties hit the markets hard.

In early March 2022, the benchmark Chicago Wheat, a key indicator of wheat prices, experienced a sharp increase, reached a then record high of $13.63 per bushel — to put this into perspective, the benchmark was trading at under $8 per bushel in mid-February and was as low as $5 per bushel in mid-August 2020.

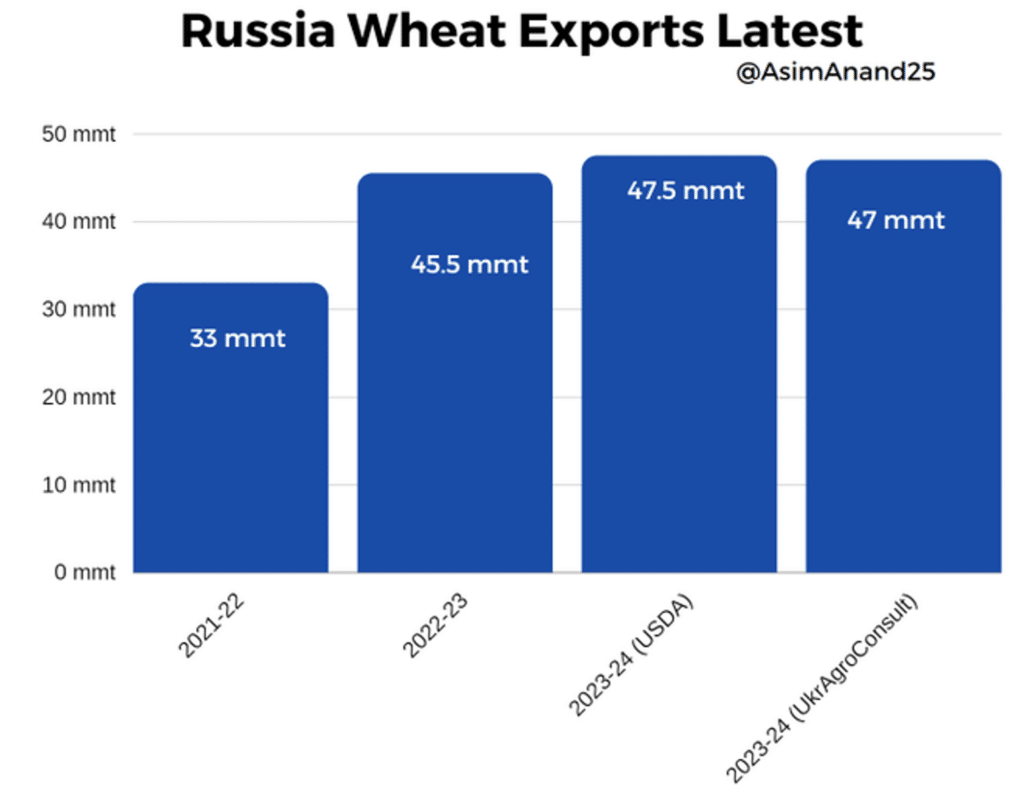

Even before Ukraine, wheat prices had already been exacerbated by inflationary pressures triggered by the pandemic. But overnight, Russia, the world’s leading exporter of wheat (accounting for 20% of global exports at 39.1 million tons), had its exports throw into doubt. And Ukraine, which itself contributes another 10% to the global wheat export market, also saw its exports threatened.

Initially, the closure of ports in Ukraine and Russia’s military actions heavily disrupted grain shipments, leading to a general shortage and hence the price pressures. The situation was further worsened due to a squeeze on short positions held before the war began in Ukraine. AgResource reported a wheat short squeeze, forcing importers to use up their domestic wheat stocks and search for alternative supply sources from April/May 2022.

Egypt, a significant importer of wheat, had to cancel two orders due to overpricing and multiple companies refusing to sell their supplies — and India, which would normally have stepped up exports, was simultaneously experiencing a year of drought and flood collapsing production.

The crisis had even more severe implications for African nations heavily dependent on Ukrainian and Russian wheat, which collectively imported $4 billion worth of agricultural products from Russia in 2020, with 90% of this being wheat.

Moreover, the closure of the Black Sea corridor hugely impacted on the fertiliser market as well. Russia is also a major producer of potash, phosphate, and nitrogen-containing fertilisers, and was faced with restrictions on exporting them. This was compounded by insurers’ refusal to cover Russian exports, out of fear of future embargoes.

Additionally, Russian gas, a crucial component for fertiliser manufacturing, experienced record prices and also faced the threat of future sanctions. As a result, fertiliser prices surged, putting further strain on agricultural sectors — not only could countries not get hold of wheat, they also couldn’t get fertiliser to grow their own.

The solution was a UN-Turkey brokered deal made in July 2022, which allowed both Russian and Ukrainian wheat exports to sail out of Black Sea ports under a ‘white flag.’ This seriously calmed wheat down — but the crop may be about to come a crop once more.

Ukraine grain deal expires

While the deal was extended multiple times, has now expired. Russia had requested:

- reconnection of the Russian Agricultural Bank to the SWIFT payment system

- being able to launch the Togliatti-Ofessa ammonia pipeline

- having Russian ships be allowed to enter foreign ports

- removal of restrictions on Russian grain

Given that these terms have not been granted, the war has entered an even bloodier phase — but the battlefield deaths could be dwarfed by a genuine food crisis.

The Black Sea grain corridor remains a crucial route for transporting wheat to countries facing acute hunger, such as Ethiopia, Yemen, and Afghanistan. The UN’s World Food Programme heavily relied on this corridor, and Ukraine provided over half of the programme’s wheat over the past year.

But Russia’s is now treating ships heading for Ukrainian ports as potential military targets. Over the past three nights, Russia has launched attacks on Ukraine’s grain facilities in port cities including Odesa. Dealing more death and destruction, an estimated 60,000 tonnes of grain has been destroyed, alongside key parts of Ukraine’s grain export infrastructure.

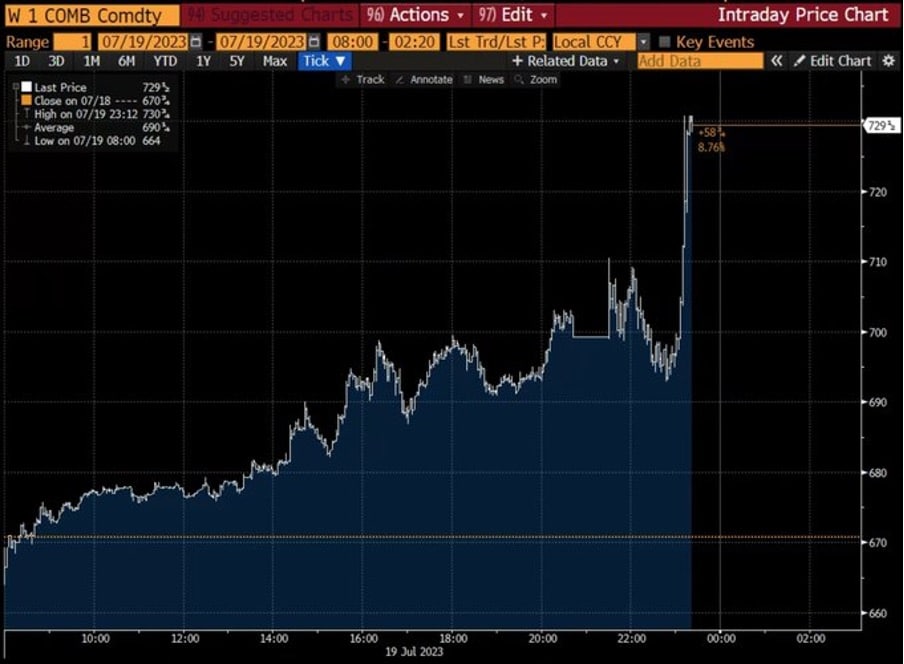

With Ukrainian ports forcibly closed, wheat prices on the European stock exchange soared by 8.2% in a single day, reaching €253.75 per tonne, while corn prices rose by 5.4%. In the United States, wheat futures experienced an 8.5% jump, marking the highest daily rise since Russia’s invasion of Ukraine in February 2022. It’s worth noting that corn usually marks in lockstep with wheat, as it is substitutable in many cases.

And Russia has also been engaging in further airstrikes targeting Ukrainian cities, further escalating the crisis with even more civilian deaths. With India, China, and Midwest US all experiencing climate-related production issues, unless a new deal can be struck, and fast, there are three potential problems:

- potential famine across multiple poorer countries

- mass migration from these countries on an unprecedented scale

- elevated wheat prices, alongside other soft commodities such as corn and lean hogs

Of course, I always believed the deal would elapse eventually — and I was right about orange juice too.

Yes, there’s always a chance that Putin is long on wheat and plans to reverse his bet when ready to resume the agreement.

But that would be insider trading.

This article has been prepared for information purposes only by Charles Archer. It does not constitute advice, and no party accepts any liability for either accuracy or for investing decisions made using the information provided.

Further, it is not intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.