The shares of UK Product Group (LON: UKR) went up 62.5% on Thursday 17 March. This means absolutely nothing of any importance and is not something we could have made money out of trading. If we’d even tried to trade it, we would have lost money doing so.

This is an important lesson about trading in any market. We must think not only about share price moves – or the move of any instrument – but also about the twin issues of liquidity and spreads.

For it is true that the share recorded as moving the most that Friday – UKR at 62.5% – was not a money-making proposition.

The costs of trading really matter

The secret here is that we pay several different amounts to different people for being able to trade shares. There’s whatever our broker might charge us for their services. This might be minimised by using a CFD broker say, or there are commission free brokers out there these days. But we also pay the “spread”. The price at which we can buy something is not necessarily the same as the price at which we can sell something.

This is where liquidity and spread merge and meet. The more trade there is in something – the more liquidity – then the closer those buy and sell prices will be. In the market jargon we call his “bid” and “offer”. In some market that’s really, really, liquid, perhaps the FX market for $/€, or a small trade in something like Exxon (NYSE: XOM) we’ll find that bid and offer are in fact the same price. We can buy and sell the thing at the same price.

Almost never can we do this with the same person. But in one of those very liquid markets, we might be able to buy from one and sell to another at that same price. Of course, such a trade doesn’t do us much good, but it illustrates one of the costs of trading. That spread is the amount we’ve got to leave with the market for being able to trade on the market.

Or, if we prefer, it’s the market makers’ margin.

If very liquid markets have small to no spreads, then logically we would expect that the less trade there is going on – the less liquidity – then the wider the spread. This is also true and makes logical sense. If the market maker knows that there are only going to be a few trades a day, or even one every few days, then he’ll want a substantial turn or margin on his activities. Pennies are fine on each of thousands of transactions, but pounds are necessary if there are only a few.

This is what is true here in UK Product Group. There’s very, very, little trade in the company stock. Therefore, the spread is very wide. As it’s quotes as of my pixel time it’s 2.00 bid, 4.50 offer. That is, if we want to sell to the market maker then he’ll pay us 2 pence a share, if we want to buy from him then it’s 4.5 pence a share.

Some shares just aren’t for trading

The first thing we should note about this is that therefore UK Product is simply not a share for us to be trading. We’d in fact need an over 100% move in the share price before we could possibly profit, assuming we’re buying that is. 100% share price movements aren’t that common either if we’re honest about it.

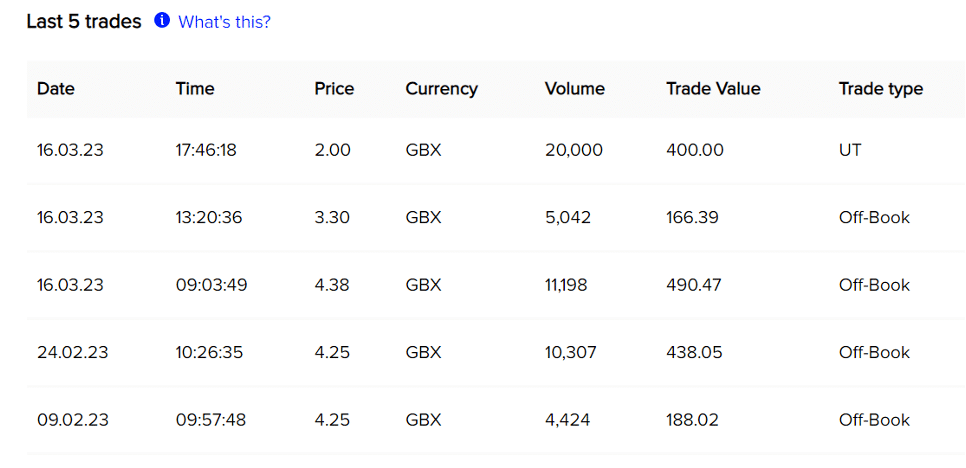

This also explains why that reported 62.5% move in the UKR share price just wasn’t something we could have traded at a profit – nor should have traded. It’s possible to go into further detail too. The stock exchange posts up the last few trades:

We can tell from those prices that there were only three trades on the day (and none for nearly a month before that). One was obviously a purchase, the second probably, given the prices, and the third a sale to the market maker. All for trivial sums, no more than £500. But, given the way that the quoted stock exchange price is calculated – on the mid-price – that gives us our large movement in the reported share price. There were two purchases, one sale, that weights the reported price to the higher end of the bid/offer spread. There has, in fact, been no real move in the prices at which we can buy and sell UKR at all. The 62.5% move is just an artefact of market reporting, no more.

Now, this is all trivia in a stock that no one trades and possibly only the Chairman’s mother cares about. But the lesson from it is hugely important.

The Bid Offer spread really matters

When we do go to trade one of the costs that we have is the spread. This is distinct from any brokers’ fee and is the amount that we pay to the market itself for the ability to trade. This difference between bid and offer prices will be higher the less trade there is in something, lower the more. So, whenever we start to predict or expect a price move our first question always has to be – will it be larger than the spread? If it isn’t then don’t bother.

Spreads matter, they’re an integral cost of buying and selling. If we ignore them, we’re going to leave all our money with the markets even if we do get market movements the right way around.