Disenfranchised, can’t find your stock, or been burnt by a weak stop loss? It might be time to upgrade.

There comes a time in every millennial investor’s life when the time is just right. It’s like when you become a father and instantly retire those weekend skinny jeans in favour of faded beige shorts.

I’m talking, of course, about that point when you set aside your childish first investing app, which is apparently ‘free,’ and open an account with one of the legacy brands. This subject is perhaps particularly pertinent as Robinhood seeks to launch its UK offering.

As I freelance for one of these legacy brands, I may not have a completely unbiased opinion. I do freely recognise that the proliferation of the likes of Trading212, Freetrade, eToro et al have helped to spread investing to the masses and forced older brands to improve their offering.

Or in other words, market competition is working as intended.

But these apps have limitations that you should be aware of. Importantly, these limitations may or may not matter to you individually dependent on your own personal circumstances — and if so, it can be better to stick.

But as a general rule, the paid-for apps tend to become more attractive as your wealth grows, and as your investing confidence increases.

As a caveat, not all of these trip-ups apply to every free platform. This is not financial advice, do your own research, and remember that every platform has different advantages and drawbacks.

Let’s dive in.

15 free trading app issues

1. Voting rights — free apps apply their ‘best effort’ to allow you to vote with your shares. This is legally meaningless nonsense and will get you nowhere. Paid-for apps will offer proxy voting so that you almost never miss a vote. Clearly, this is going to matter more the more heavily invested you are in a company, and especially with early-stage stocks.

2. Customer service — many of the free apps offer 24/7 support, but there’s a difference between having a useless online chat, and an available phone number with someone who can actually help you with your enquiry.

3. Regulation — companies like Hargreaves Lansdown, IG etc are heavily regulated by Tier 1 regulators such as the FCA, SEC, and ASIC. Others are often regulated through a single regulator in Cyprus or the Bahamas, with no actual regulatory oversight. A key thing to check is whether client funds are segregated, and how that is monitored.

4. Safety — on a similar note, your funds are only protected up to £85,000 per banking licence by the FSCS scheme. This may seem like a lot (objectively, it is), but compound investing over the long term means many will comfortably exceed this limit in their ISA, and definitely in their SIPP. The solution is to open multiple accounts and keep balances below the limit, but you want to be completely sure your funds are as safe as can be.

5. ISA rules — free apps have a history of getting ISA regulation wrong. Two very recent examples include fractional trading, which is banned in ISAs as highlighted by HMRC, and clients being allowed to hold non-ISA qualifying stocks such as Polestar. Legacy brands have not made these mistakes. Further to this, the likes of IG and Vanguard offer flexible ISAs that allow you to withdraw without affecting your £20,000 annual allowance.

6. Advanced platforms — when you first start out, you want the most straightforward platform possible so you can get to grips with the basics. Thereafter, you may want to upgrade to more complex products, and these often aren’t available for free. Then there’s functionality — the paid-for platforms are usually just better from a UX perspective.

7. Instrument availability — as an example, IG offers trading in over 18,000 instruments, while eToro offers 3,000. That favoured FTSE AIM share or bond may simply not be available — which can be a pain when you realise this too late to take advantage of an opportunity.

8. Risk management tools — there are many ways to manage your risk, but not all are available on the free platforms. One of the most important is a ‘guaranteed stop loss.’ When you set a stop loss at a set price, you would think that you would automatically sell at this price. However, in volatile instruments (my favourite), this is not the case due to slippage caused by market gapping. A guaranteed stop loss order protects your position, at a premium, by guaranteeing to exit your trades at the exact price you specify, regardless of market volatility.

9. Research and education — research on the free apps is either non-existent or often fairly poor. This isn’t a criticism — there’s a reason why they are commission free. Dependent on your investing attitude this may or may not be relevant; if you plan on investing once a month into a FTSE 100 tracker, it’s unlikely to matter. If you’re actively day trading, it can be the edge that makes all the difference.

10. Fees — while commission free apps are usually cheaper, there are often other fees that add up. Overnight fees and account inactivity fees are the classics, in addition to withdrawal fees — eToro currently charges $5. These can be more expensive than just paying for trades elsewhere, but this does depend on your individual activity.

11. Gamification — Robinhood has got into hot water stateside not only for its PFOF model (which is banned in the UK), but also for its casino-like app, which encourages risky trading. One of the key things to understand is that the more trades you make, the more money the platform makes — while the opposite is usually true for clients, excluding professionals. The FCA is already cracking down on gamification, but it’s important not to get suckered in. There is a difference between high risk investing and gambling.

12. Building on this, copytrading is rare on paid-for platforms and common on the free ones. It may seem like a good idea to copy the most successful investors, but this is often a fallacy as they are usually taking huge risks and will eventually make a big mistake. Copytraders are financially incentivised to get people to copy their trades, and you probably won’t get the same risk warnings as you get from me. Beyond this, you never get the full picture — my ISA account looks incredibly risky, but my SIPP is extremely boring.

13. Push to CFDs/spread bets — as share dealing is expensive for platforms and generates little revenue, many free offering will aggressively market leveraged trading with no checks to ensure you understand the risks. As a general rule, circa 70% of clients lose money when trading with CFDs, and as a consequence, Spain has just banned them entirely for non-professionals. Legacy brands do of course offer leverage but are perfectly happy for you to continue simple investing as you are paying for the service.

14. Aggregating orders — free trading platforms will often aggregate orders where necessary. This isn’t common with highly traded blue chips like Tesla or Lloyds but is fairly regular with AIM shares. This means that when you buy or sell a volatile and/or low volume share, your order gets aggregated with other customers until there are enough to make the trade worthwhile for the platform — during which time the price you actually buy/sell at is different to what is achieved in your account. This is less common with paid-for accounts.

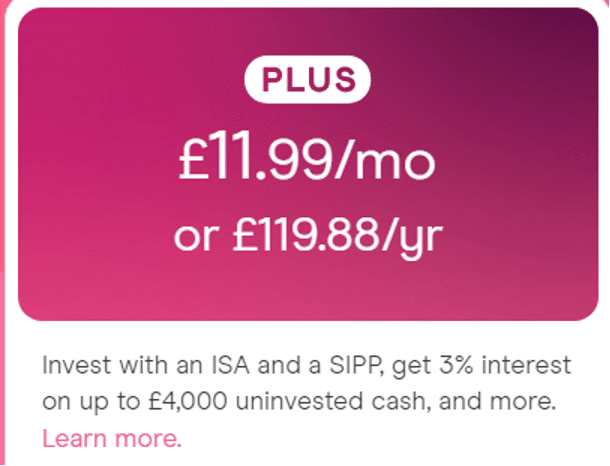

15. Is it really free? — Most of the free trading platforms charge a fee for ISA and SIPP products, and these tax shelters are essentials for almost every UK investor. Freetrade charges 11.99/month for access to both through their Plus plan, and this can be more expensive than accounts at legacy platforms. The ISA alone costs £5.99/month — so it’s not really ‘free.’ Similarly, eToro’s ISA is managed by Moneyfarm, and is certainly not free either. The difference between ‘freemium’ offerings and legacy brands can be much smaller than you think.

Is it time to switch?

Again, this is not financial advice. But if you’re starting to trade more regularly, understand the basics, can define the difference between sales and revenue, calculate a P/E ratio, or want to trade more exotic instruments, it may be time to upgrade.

While this piece may feel like an attack on free platforms, it’s really not. They have their place; they’re great for people who are investing a set amount each month into an index tracker, for those getting started, and in general for those for whom investing is maybe not their ‘thing.’

But once you get started with a paid-for platform, the difference can be night and day.

This article has been prepared for information purposes only by Charles Archer. It does not constitute advice, and no party accepts any liability for either accuracy or for investing decisions made using the information provided.

Further, it is not intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.