Macroeconomic/ geopolitical developments

- A hawkish turn from major central banks ahead of the Fed

- Major central banks the Reserve Bank of Australia (RBA) and the Bank of Canada (BoC) took markets by surprise with 25 basis points hikes on Tuesday and Wednesday respectively.

- Both banks cited stubbornly high inflation pressures which.

- Volatility continues to fall across financial market asset classes:

- the VIX Index (measuring volatility of the S&P 500) is below 14, its lowest since before the pandemic.

- the MOVE Index (measuring volatility of Treasury bonds) is at its lowest since February 2023.

- Forex volatility (from the Deutsche Bank Currency Volatility Index), has plunged to its lowest since February 2022.

Global financial market developments

- The major US stock averages, were sideway but positive higher with the S&P 500 hitting a new multi-month high and entering “bull market” territory, up over 20% from the October 2022 low.

- European indices stayed in con, mostly just lower last week.

- The Japanese benchmark, the Nikkei 225 hit another new multidecade high to levels not seen since the 1990s.

- US and European Bond marked time ahead of the Fed and ECB decisions this week.

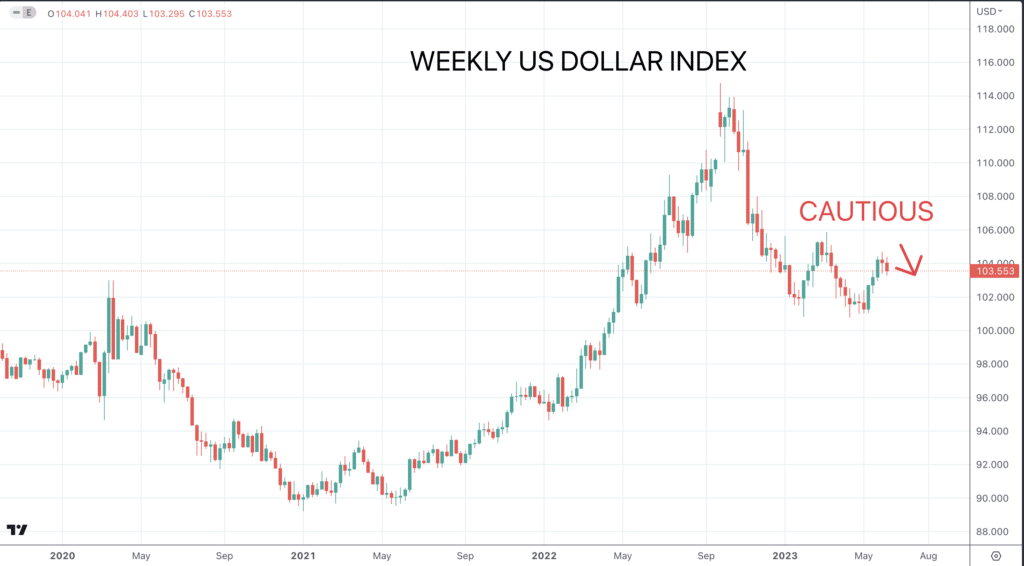

- The US Dollar Index faltered back from a multi-week high from the end of May.

- Gold was sideways but looks to be trying to build a base.

- Oil stayed in a range, unable to build on the prior leap after the OPEC+ supply cuts at the start of June.

Key this week

- Central Bank Watch: A huge week for central banks, with the FOMC decision on Wednesday, then we get the European Central Bank (ECB on Thursday and the Bank of Japan (BoJ) on Friday.

- Macroeconomic data: The US CPI inflation data is the main focus for the week on Tuesday, but that day we also get the UK Unemployment report and also the German ZEW Economic Sentiment Survey. Thursday sees Chinese Industrial Production & Retail Sales, plus the same from the US.

| Date | Key Macroeconomic Events |

| 12/06/2023 | N/A |

| 13/06/2023 | UK Unemployment and wage growth; German ZEW Economic Sentiment; US CPI |

| 14/06/2023 | UK monthly GDP; US PPI and Federal Reserve monetary policy |

| 15/06/2023 | Australian Unemployment; Chinese Industrial Production & Retail Sales; European Central Bank monetary policy; US Retail Sales & Industrial Production |

| 16/09/2023 | Bank of Japan monetary policy; Michigan Sentiment (prelim) |