Global debt has soared to a record $307 trillion, rising by a staggering $100 trillion over the past decade, and now represents 340% of world GDP. This is why there is no easy escape from the upcoming recession. The salve to bring economies back after a drop in asset prices and contraction in growth has always been for governments to ramp up deficit spending and for central banks to print a massive amount of new money to flood the banking system with credit while at the same time bringing down borrowing costs significantly. However, the global economy is already debt disabled and is also coming off one of the worst concurrent battles with inflation ever suffered. For example, the US and Europe had official inflation near 10% and actual inflation near 20%. Therefore, borrowing and printing even more money to combat a recession this time around may not cause interest rates to fall for very long, if at all. There is a significant risk they will soar on the long end of the yield curve instead.

Some market gurus claim that public debt and deficits do not matter. But they are wrong. Onerous debt and deficits are a tax on future consumption and lead to higher rates of inflation and lower rates of growth. But of course, the US will always be able to find buyers for its debt—even if it must buy it all itself; but the question is at what interest rate? The US has the world’s reserve currency and the most liquid bond market–even though both conditions are now being challenged. However, having the world’s reserve currency did not stop the benchmark Treasury Note from soaring to 15% in 1980. Inflation and credit risks can cause US rates to skyrocket. It has happened before, and it will happen again.

- The US will be spending $1 trillion on interest payments on the National debt in 2025. In 2007 the total deficit was just $160 billion

- 1/5th of all revenue spent on interest

- Total US debt/GDP is now 123%. It was 60% of GDP pre-GFC.

- National Debt is 725% of revenue. Adding 40% of all yearly revenue to the debt this fiscal year alone

Artificially-low interest rates lead to massive debt accumulation and asset bubble formation.

Home prices are now 47% higher than in early 2020, with the median sale price five times the median household income. Home Prices continue to jump; they increased by 6.3% y/y in April.

CNBC reports that half of all renter households — more than 22 million — spent more than 30% of their income on housing, which is considered “cost burdened” by Harvard Joint Centers for Housing Studies. Twelve million of those households spend more than half their income on rent. For homeowners, 20 million are considered cost-burdened by their monthly payments. All of those cost-burdened levels represent records. Maintenance, taxes, and insurance costs are also surging, with insurance up by over 20% from 2022-2023 alone.

The massive bubble in stock prices is abundantly clear. The Price-to-sales ratio of the S&P 500 is close to 3. This ratio was 1.5 just prior to the GFC in 2008, and the median figure is 1.5. The total market cap of equities as a percentage of GDP is 192%. This ratio was just 106% prior to the GFC.

The private credit bubble is daunting as well.

- Private credit loans to businesses that cannot get a loan from a bank or issue corporate debt- totaled $100 billion pre-GFC in the US. That number is now $1.7 trillion, up 1,600%

- Corporate Debt is now $13.7T, which is a 100% increase since 2007 and a record 49% of GDP.

- CLOs, which are securitized pools of leveraged loans, were $300 billion in 2008 but are now $1.4 trillion today—a 366% increase!

Hence, we have three massive bubbles: credit, housing, and equities—a triumvirate of bubbles all at records and existing simultaneously.

The economy is now broadly weakening, and yet the only thing that seems to matter to Wall Street, at least up until a few days ago, is that NVDA is adding the valuation of an MCD to its market cap each day. Or that NVDA is worth more than the entire market cap of German equities. NVDA is up 140% this year while the broader market, as represented by the Russell 2000, is actually down slightly on the year, and the equal weight S&P 500 is up just 4%.

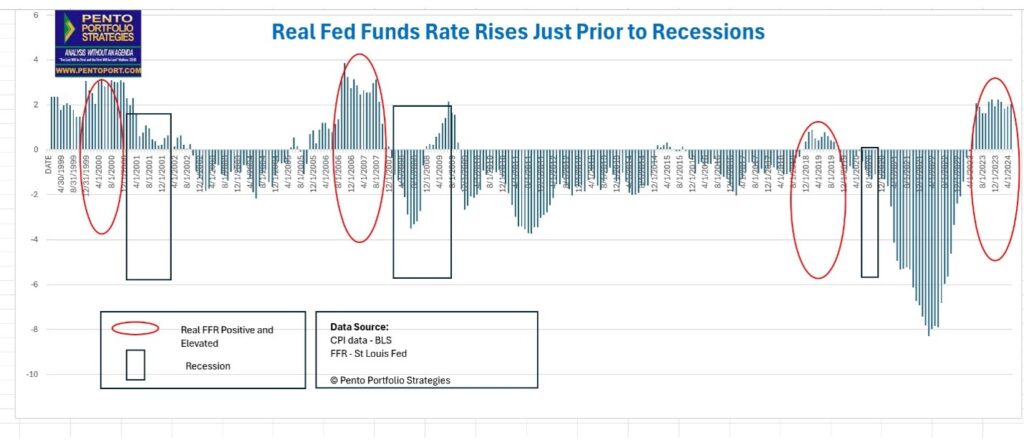

This is the narrowest bull market in history. All such narrow rallies have ended badly, such as the Nifty fifty and the NASDAQ bubble eras. However, this AI-led bull has brought the market to the most expensive level ever on so many metrics. For more proof, the equity risk premium is now in negative territory. This means that the earnings yield of stocks is less than the risk-free return from owning treasuries. This is a very rare phenomenon. Simply owning a basket of stocks that mirrors the S&P 500 now offers investors more risk and less return than owning bonds. That is why it is imperative to hold a significant portion of your portfolio in Treasury bonds (in the correct duration) while also owning the right stocks with the appropriate beta profile, given today’s unstable backdrop. The Fed wants to start cutting rates as soon as possible but cannot do so quickly or significantly, given that inflation remains sticky and well above its target. This means the level of the real FFR will remain near 2% for an even longer time, which will send the economy into a recession just as it always has done so in the past.

By the way, the same dynamic applies to the yield curve inversion, which has now been upside down for the longest duration in history. PPS remains long the market while vigilant for the early warning recession signs that will trigger our plan to try and protect and profit from the next bear market. Having a model and a plan is critical now more than ever.