There can be no denying that 2022 has proven to be a challenging year for all investors. For example, the FTSE All World Index has a 1-Year change of -17.26%. Similarly, the S&P Global 100 has a 1-Year change of -13.45%. (As at 10:30 on Friday, December 16th, 2022).

A similar tale of poor performance is to be seen across the government bond market as illustrated in Table 1.

Source: Bloomberg

Whilst Table 1 reveals that the days of easy money and QE are long gone what has been clear is that in the equity space many sectors have faced trouble in the last 12-Months. One area that has been struck by severe headwinds has been equities in the area of sustainables or environmental, social, and corporate governance, (ESG).

A key reason for this is that the Russian war with Ukraine has seen a shortfall in energy flows and a matching rise in prices. This has led to an adjustment in portfolio managers approach to their exposure and as oil and gas stocks have seen strong demand so the tilt toward sustainable equites has been compromised.

The worse hit has been dealt to strategies that solely sought exposure to hydrogen stocks. J.P. Morgan reported that many such once popular funds have fallen by over 40% from January to October 2022. Many of these stocks have a high cash burn and given they have yet to turn a profit their borrowing costs are highly sensitised to rising bond yields as shown in Table 1.

Don’t Turn Your Back on ESG

To make money in the markets, one must seek the undervalued gem. Simply jumping on the old bandwagon will not yield strong returns in 2023. Therefore, even with the recent difficulties, I believe there are several reasons why it would be unwise to totally abandon an interest in having another look at sustainable equities within a portfolio.

Iberdrola S.A.

Iberdrola S.A. is a Spanish multinational electric utility company based in Bilbao, Spain with a workforce of 34,000 employees serving around 31.67 million customers. At the end of September this year revenue was booked at EUR13.47 Billion, a gain of 45.7% on the year with Net Income at EUR1.03 Billion +17.3% with EBITDA at EUR2.83 Billion +14.54%

In November Iberdrola announced that it would increase its dividend from last year’s comparable payment on the January 19 to EUR0.1458. This means the dividend yield for the company will be 4.2%, which is fairly typical for the industry.

The company has committed to ensuring all its global facilities will deliver a net positive effect on the natural environment by 2030.

It is also the only European utility to be included in all 23 editions of the Dow Jones Sustainability Index. This should be taken as a positive sign given that from an initial universe of some 10,000 companies, only 10% of the listed companies with the best sustainability scores are finally selected.

Source: Pope Family Office

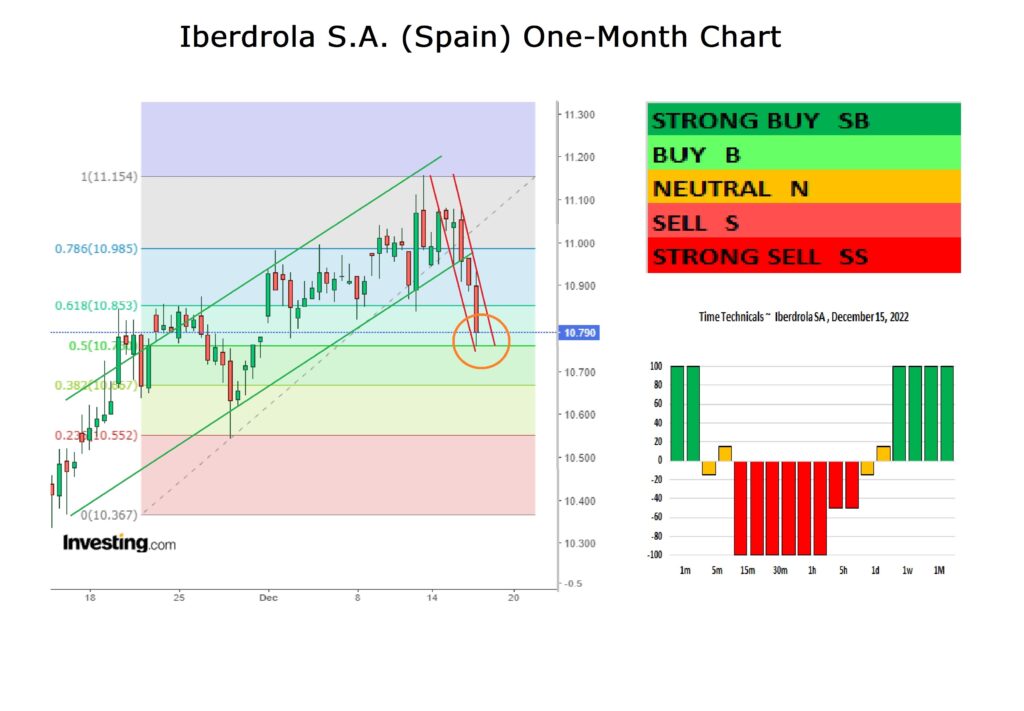

One can see that the technical sentiment is going to look gloomy until one hits the One-Week area. I am overlooking the initial positive sentiment as just a hope there will be a bounce at the 50% support line.

So, this is not a stock to buy today, (December 15), rather it is worth looking at just before the markets close down for Christmas and New Year. Get n ahead of a potential January push. I would expect prices to return to the initial positive channel and on that basis, I look for initial gains to 11.15 and 12.14.

This is driven by the fact that to reduce dependency on Russian fuel while also meeting climate objectives, Europe needs to reshape how it sources and uses energy, and fast. That means Europe will see an accelerated rollout of lower priced renewable projects. Clean energy investment is accelerating in Europe as a response to the European Union’s (EU’s) “REPowerEU” plan. This will allocate EUR 300 Billion in investment by 2030 to help reduce the EU bloc’s dependence on Russian fossil fuels. If this takes too long to work through my stop loss is 10.30.

Glencore Plc

Glencore Plc is a Swiss multinational commodity trading and mining company with headquarters in Baar, Switzerland. Glencore’s oil and gas head office is in London and its registered office is in Saint Helier, Jersey. The current company was created through a merger of Glencore with Xstrata on 2 May 2013 and it trades on the U.K. stock exchange as GLEN.

One may say this is an odd choice when I am wearing my ESG hat, however, Glencore expects to shut down 12 coal mines over the next 12-Years even as it is booking strong profits because of high coal prices.

Glencore’s coal business is expected to generate about USD16.7 Billion in earnings before interest, tax, depreciation and amortisation next year, more than half the company’s total.

However, its coal production is expected to be flat between 2022 and 2025, with guidance of roughly 110 Million tonnes a year, down from Glencore’s previous estimate, according to an investor update published on December 6.

I am also attracted by the fact that analysts at JPMorgan Cazenove have named Glencore as their overall top pick for 2023 in a European Metals & Mining sector review.

Source: Pope Family Office

Here is another chart that suggests strong buying will begin to materialise in a week from now. I would start snapping this stock up earlier than that as it has a good tailwind behind it. Any drift into the lower half of the impulsive channel is a buy signal for me. I am looking for a push into January that will see a 38.2% extension in the featured range to 645.64. Stop loss set at 380.00.

Pearson Plc

Pearson Plc is a British multinational publishing and education company headquartered in London, England. It was founded as a construction business in the 1840’s but switched to publishing in the 1920’s. It is the world’s largest education company. The company provides educational and learning technologies like e-learning and computer-based testing and Pearson was a definite winner during the COVID-19 lockdown but as the restrictions were lifted it did relinquish many of its prior gains.

This is not an exhausted story as it does a lot more than help traditional educational establishments. Online learning allows institutions to offer their services far and wide beyond their campus setting. People, on a global basis are developing lifelong learning habits, particularly as the world is becoming more complex and more interconnected, and new ways of working emerge.

Pearson is well laced to exploit the opportunities for certification, up-skilling, and retraining that are rapidly becoming essential in today’s workplace.

CEO Andy Bird said on November 6:

“…It’s very much the beginning of our journey . . . of what could be explosive growth…”

Cevian, the activist shareholder with a 10% equity holding has cited the groups pool of high-quality assets that are cash cows, and it applauded the strategic plan to cut costs by GBP100 Million in 2023. Partner Martin Oliw said the company had a “…compelling vision…” and a strong foundation for profitable growth.

Source: Pope Family Office

A similar pattern of technical sentiment is seen here, however, I am looking to be buying on any dip that is seen as the impulsive channel looks strong and I am looking for new highs to be seen on a rolling 12-Month basis with 1101 and 1160 very much in my sights. I will have a stop loss set at 750.

Investment Takeaway

The clear signal we see here is that as the Fed, European Central Bank and Bank of England still have a firm rate policy in mind, so the markets will be reacting to every snippet of news from actual rate decisions, minutes and commentary. That is why these three equities do show clear buying signals until a week from now. Apart from the case of Iberdrola S.A. I think hesitation will prove a costly error.

Whilst sustainable equities as a sector have had a rough 2022, they are still very much in mind and look to be undervalued and as such offer a good chance of low-price entry. Miners, and the fossil fuel entities do not superficially chime with ESG, however, the facts are that they are cleaning up their operations and still are able to generate strong cash flows.

It is also a given that the world is increasingly competitive and as such upskilling on top of general education are the keys for success into 2023 as we look to increase critical thinking and logic when making decisions and interacting with people.