Macroeconomic/ geopolitical developments

- Central Banks were front and center last week, with the Swiss National Bank (SNB), US Federal Reserve (Fed), European Central Bank (ECB), Bank of England (BoE) and Bank of Japan (BoJ) all in play.

- First, the ECB held an ad hoc, emergency meeting on Wednesday to deal with surging bond yields for European periphery government bonds, evident since the ECB announced an end to their Quantitative Easing (QE) program, the Asset Purchase Program (APP) and pivoted to a more hawkish stance the previous Thursday (9th June).

- Then, the Fed interest rate decision, statement and press conference on Wednesday brought a 0.75% interest rate hike, as the market had quickly priced in and anticipated after the prior Friday’s US CPI data showed inflation still running hot.

- Further, on Thursday the SNB unexpectedly hiked interest for the first time in 15 years from -0.75% to -0.25% and indicated further tightening may be needed. A hawkish pivot.

- The BoE also hiked rates on Thursday, again by 0.25%, their fifth successive rate increase and indicated more was needed.

- Finally, the BoJ adhered to a still very dovish tone on Friday.

Global financial market developments

- The major US stock averages plunged lower, with the S&P 500 confirming a bear market, down over 20% from the early 2022 record high (nearly 24%) and posted its worst weekly fall since March 2020.

- European and Asian equity indices also posted significant losses, with European averages now looking increasingly vulnerable (having outperformed their US counterparts on the bear move).

- US 10yr yields surged through the May high yield peaks as European bond markets led the way to higher yields, BUT the US 10yr did reverse to significantly lower yields after the FOMC meeting, possibly signaling a blow-out yield top…

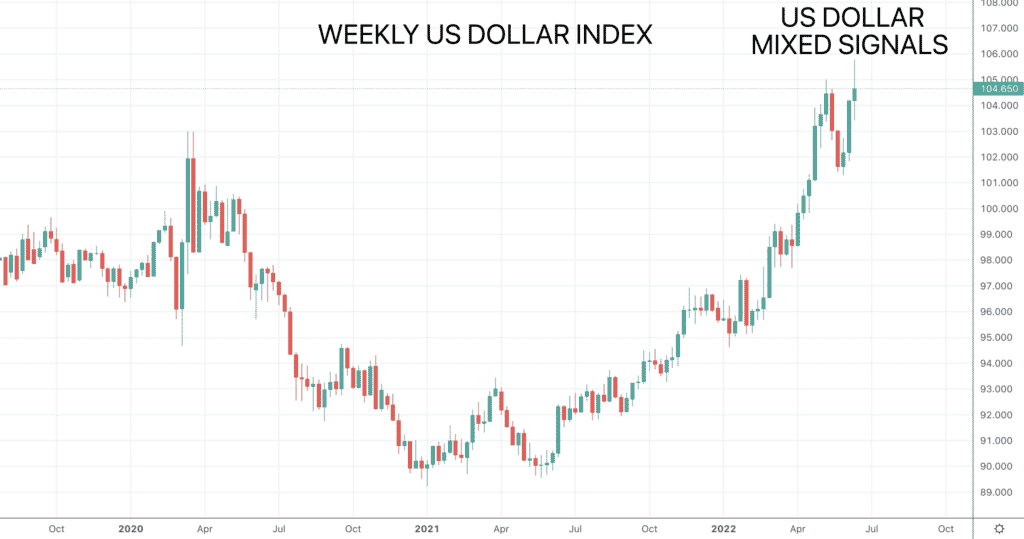

- Similarly, the US Dollar Index posted a strong advance to push through the May peak, but a reversal back lower after the Fed decision indicates a potential bullish failure.

- Gold setback and rebounded with the USD rally and setback, still trying to form a base.

- Oil plunged lower for a short-term top, flipping risks lower.

- Copper plunged below the May low, rejecting a base and setting risks lower.

Key this week

- Geopolitical focus: Still closely monitoring the war in Ukraine

- Holidays: Monday 20th June is theUS Juneteenth holiday, cash markets closed, partial days for futures markets.

- Central Bank Watch: For Central Banks, we get the Peoples Bank of China (PBoC) interest rate decision on Monday, Reserve Bank of Australia (RBA) and Bank of Japan (BoJ) Meeting Minutes on Tuesday and Wednesday respectively, then Fed Chair Powell testifies to Congress on Wednesday and Thursday.

- Macroeconomic data: UK inflation data Wednesday and Retails Sales are notable releases, but the standout data points for the week are the Global S&P Flash PMI on Thursday.

| Date | Key Macroeconomic Events |

| 20/06/22 | US Juneteenth holiday, cash markets closed, partial days for futures markets; PBoC interest rate decision |

| 21/06/22 | RBA Meeting Minutes; Canada Retails Sales |

| 22/06/22 | BoJ Meeting Minutes; UK inflation data; Canada CPI; Fed Chair Powell testifies to Congress |

| 23/06/22 | Global S&P Flash PMI; Fed Chair Powell testifies to Congress |

| 24/06/22 | UK Retail Sales; German IFO |