Macroeconomic/ geopolitical developments

- More hawkish comments from various Fed policymakers, notably Bullard and Fed Chair Powell indicated even more aggressive interest rate hikes in 2022 and also in the near future, sending bond and stock markets lower in the US and globally.

- European Central Bank (ECB) hawks and doves have called for earlier and more aggressive than anticipated removal of monetary stimulus.

- Earnings season has continued in the US, with some financial stocks improving on the poor show from the prior week

- But poor subscriber numbers from Netflix saw the stock plunge 35/% and pulled the tech sector lower, despite solid numbers from Tesla.

- French President Macron was re-elected, which should be a positive relief for European markets.

Global financial market developments

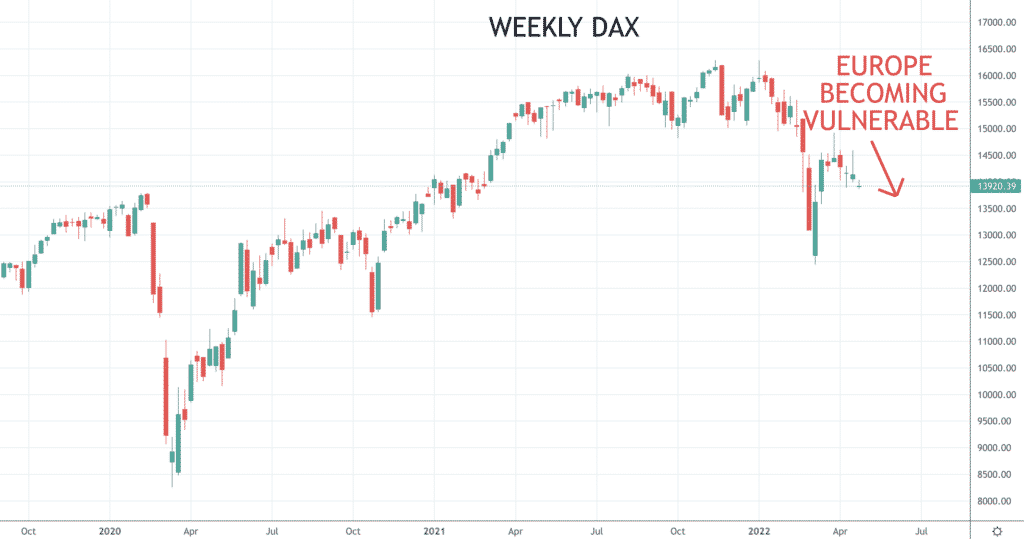

- Growth/ tech stocks lead US stock averages lower, but value stocks also joined the significant sell off.

- Global stock averages were lower too last week.

- US and global bonds sold off even further, to still lower yields.

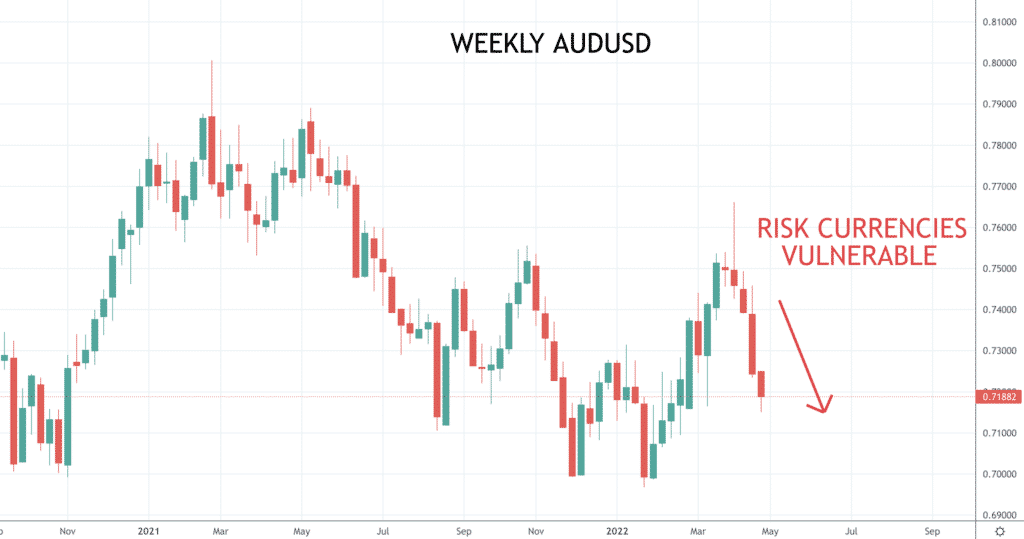

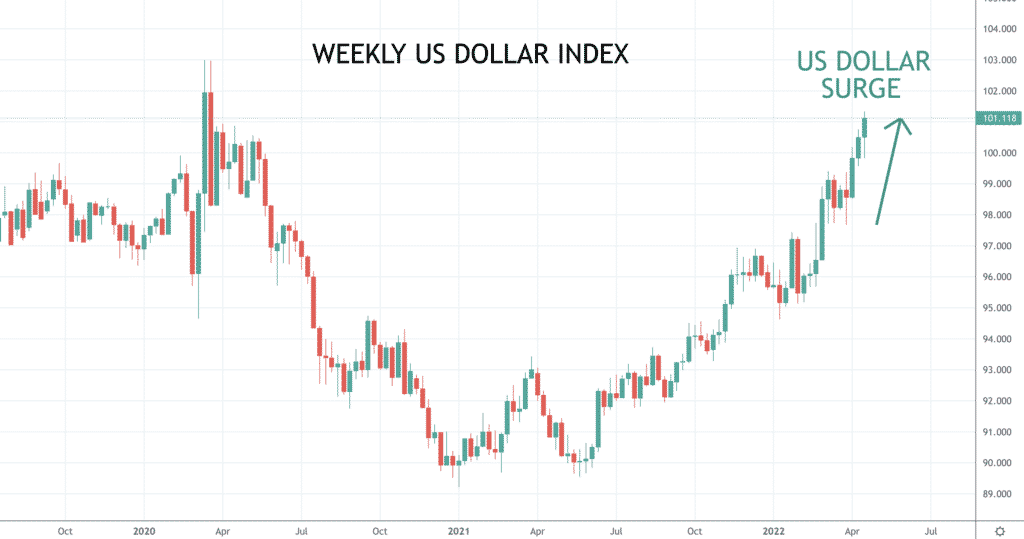

- The US Dollar surged again across the board, notably versus the “risk currencies”, the Australian, New Zealand and Canadian Dollars, but also significantly against the Pound.

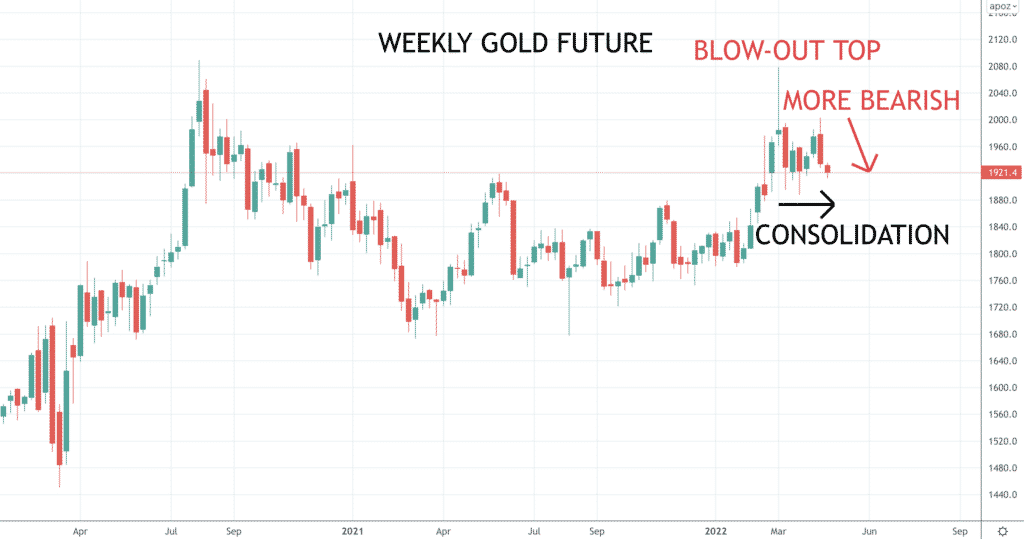

- Gold sold off, rejecting the prior week’s bull breakout from the top of the consolidation range, and now looks more negative.

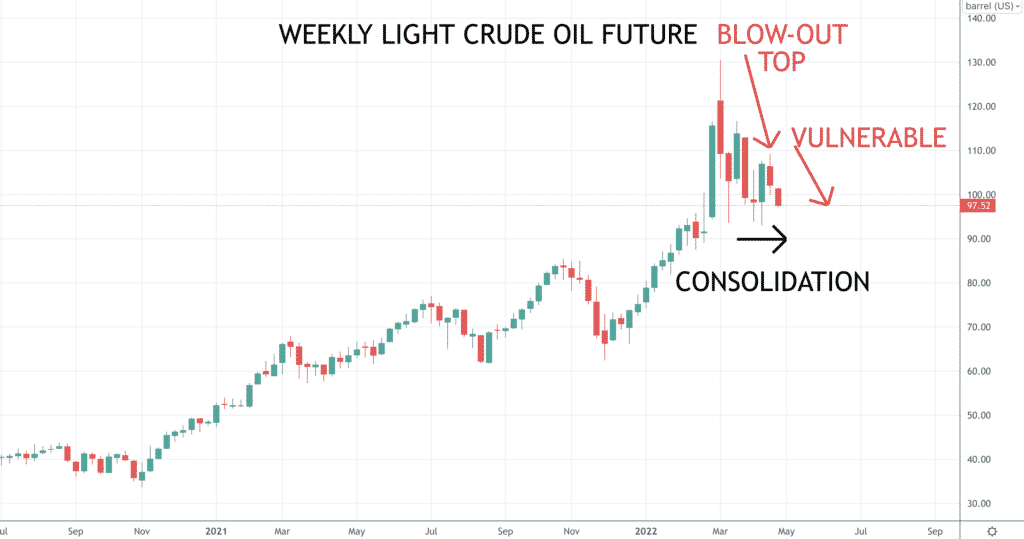

- Oil has also moved back lower, rejecting a more positive tone and sets up more negative in a range environment.

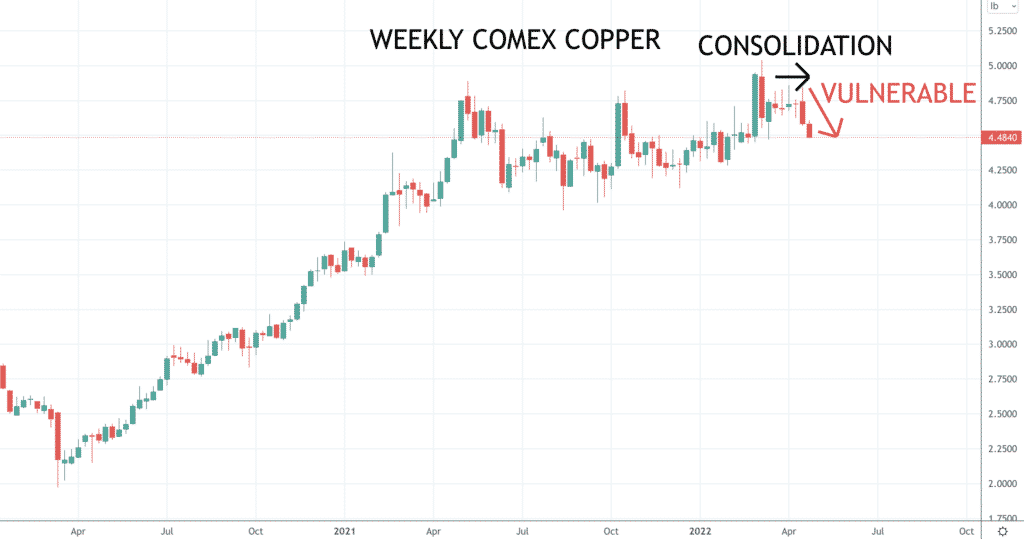

- Copper has plunged lower through the lower end of its erratic consolidation range.

Key this week

- Geopolitical focus: Closely watching the situation in Ukraine

- Central Bank Watch: A light week for Central Banks, we get the Bank of Japan (BoJ) interest rate decision, statement and press conference on Thursday.

- Macroeconomic data: The standout data releases this week will be the US GDP and PCE data on Thursday and Friday.

- Earnings data: Earnings season continues and a busy week for tech in the US, with companies to watch for including Microsoft, Google, Meta, Apple and Amazon.

| Date | Key Macroeconomic Events |

| 25/04/22 | German IFO business climate survey |

| 26/04/22 | US Durable Goods Orders; US Consumer Confidence |

| 27/04/22 | Australian CPI; ECB’s Lagarde speaks |

| 28/04/22 | BoJ interest rate decision, statement and press conference; German CPI; US GDP and PCE |

| 29/04/22 | German GDP; EU GDP; US PCE; Canadian GDP |