Macroeconomic/ geopolitical developments

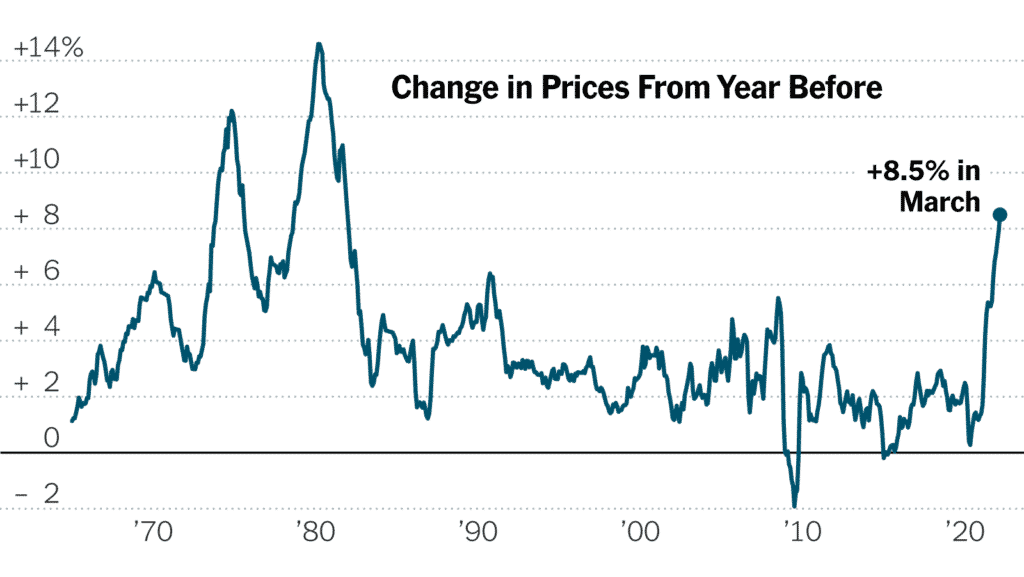

- US headline CPI data leapt by 1.2% in March, with the year-over-year rise at 8.5%, above consensus expectations to a four-decade high.

- More hawkish comments from Charles Evans of the Fed (historically a dove) regarding accelerated rate hikes echoed the comments the prior week from another dove, Lael Brainard.

- The European Central Bank (ECB) did not assume a more hawkish stance at its meeting on Thursday.

- Earnings season kicked off in the US, with the financials disappointing somewhat, J P Morgan leading the sector lower.

- The financial markets have continued to be less impacted by the Russian invasion of Ukraine.

Global financial market developments

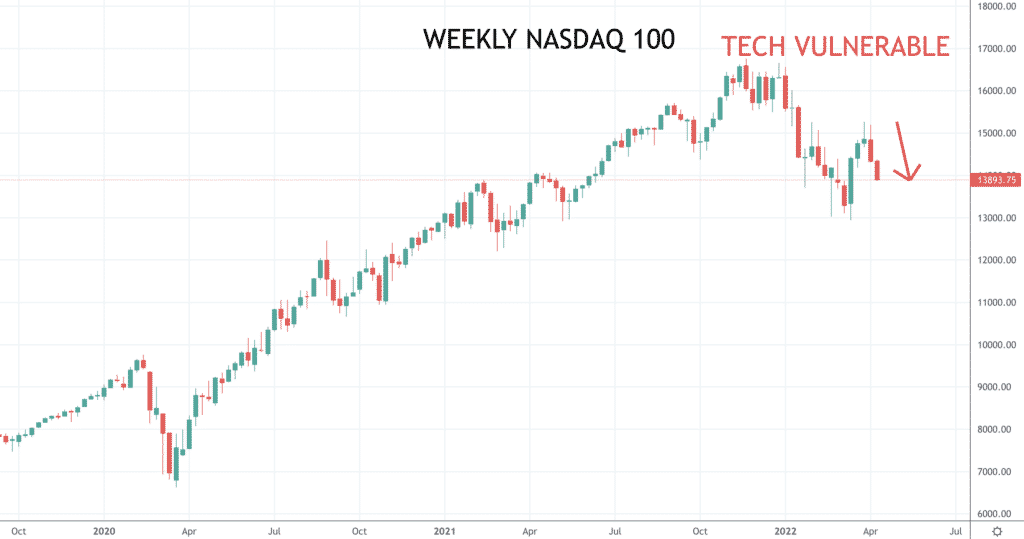

- The CPI data and ongoing hawkish comments from FOMC members saw (US and global) bond yields surge last week, and again after an initial rebound, growth/ tech stocks lead US stock averages lower, whilst value stocks held in.

- Global stock averages were mixed last week, with growth/ tech stocks vulnerable and again in the US, as the Nasdaq was a significant underperformer.

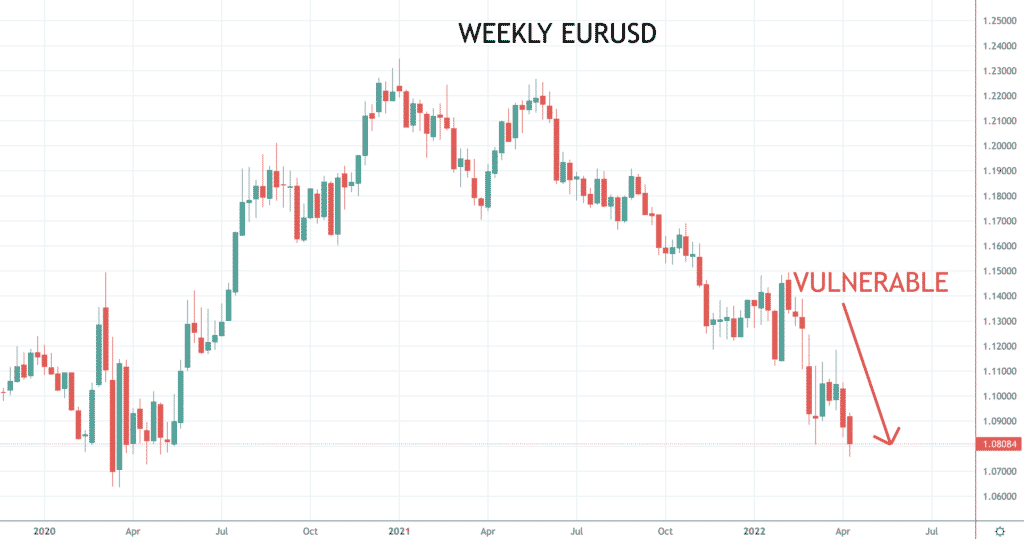

- European shares posted modest gains with relief that the ECB was not more hawkish and assisted by weakening currencies as the Euro lost ground.

- US and global bonds sold off even further to lower yields led by the US Bond market.

- The US Dollar surged again across the board, notably within G3, versus the Yen and Euro.

- But the “risk currencies”, the Australian, New Zealand and Canadian Dollars have also lost ground and are vulnerable versus the greenback.

- Gold has broken out of the top of the consolidation range and looks more bullish.

- Oil rejected a more bearish tone and looks more positive enow in a range phase.

- Copper stayed within its erratic consolidation range.

Key this week

- Geopolitical focus:

- Monday 18th April is the Easter Monday holiday, with markets closed in the UK and Europe, but the US is open.

- Closely watching for potential for Ukraine/ Russia talks to improve and maybe for a ceasefire.

- Also monitoring for a possible military escalation in Ukraine.

- Central Bank Watch: We get the Reserve Bank of Australia (RBA) meeting minutes on Tuesday and the People’s Bank of China (PBoC) interest rate decision on Wednesday. The Fed Chair, Jerome Powell speaks on Thursday and the Bank of England Governor Bailey speaks on both Thursday and Friday.

- Macroeconomic data: The standout data releases will be the S&P global Flash PMIs Friday.

- Earnings data: Earnings season continues in the US, with companies to watch including: Bank of America, J&J, Netflix, Tesla, P&G and Verizon.

| Date | Key Macroeconomic Events |

| 18/04/22 | Easter Monday holiday, markets closed in the UK and Europe, the US is open; China GDP and Retail Sales |

| 19/04/22 | RBA Meeting minutes |

| 20/04/22 | Canadian CPI |

| 21/04/22 | New Zealand CPI; Fed’s Powell speaks; BoE’s Bailey speaks |

| 22/04/22 | UK Retail Sales; S&P global Flash PMIs; BoE’s Bailey speaks |