Pilbara Minerals is great actually, it’s the result of one of the blindingly best mining deals in recent years. Once there was a lithium miner called Altura, financed in the last lithium mining boom of 2013/4. Which found lithium, developed the mine and was doing great right up to the day it went bust. The problem was that the financing costs ran away with them – the low lithium price by the time they came to market meant they just couldn’t afford having come to market. They were actually producing when they went bust too, positive operating cashflow even if I recall correctly.

The mine was bought out of bankruptcy for, again from memory, something like $130 million. Which is what became Pilbara Minerals, which now makes 50% margins on $2 billion a year of sales. Which really is one of those grand, grand bargains of mining history.

Note that those numbers are rough and from memory, the details don’t impact on the rest of this story.

Pilbara Minerals started in disaster but since then

So, why is Pilbara Minerals now the most shorted stock on the Australian market? As at 26/09/2023 that is. Well, one reason is that shorts have been making money these past few months.

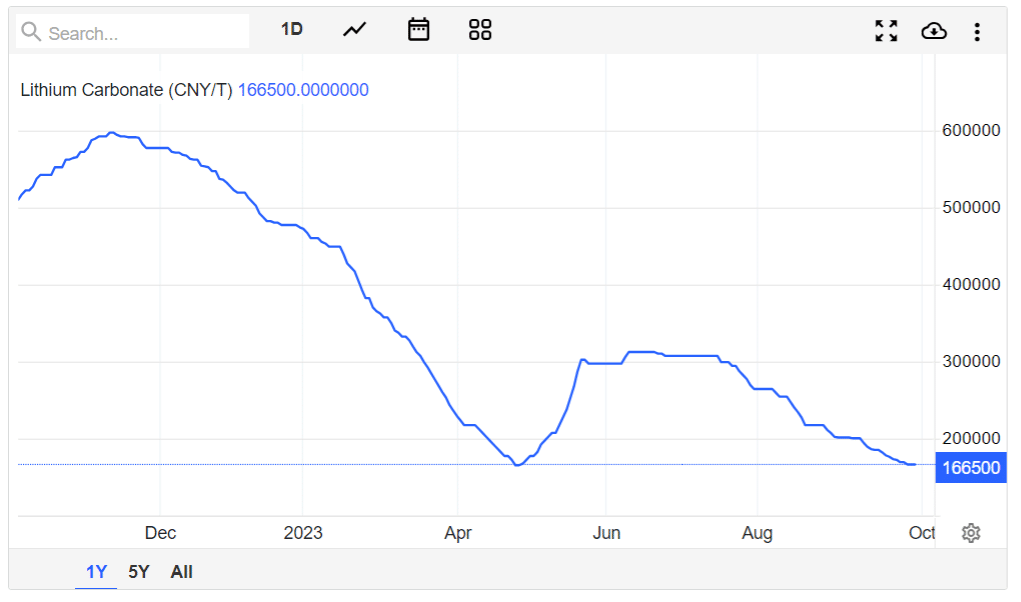

OK, so people will indeed follow a momentum trade. But it’s also true that lithium itself has fallen considerably in price. In fact, we can run that Pilbara price over the lithium price (this is lithium carbonate but it doesn’t matter which salt we use here, it’s lithium units changing in price) and see the connection.

Don’t worry that that’s in CNY either, not USD, that’s the way much lithium salt pricing does work and it’s again, the lithium unit price that’s moving, not the FX rate.

But the next question is will disaster come for Pilbara Minerals?

Which is where we can start to work out why Pilbara is that most shorted stock. The value of a miner is geared to the price of their output. Sure, the value of the mine – taking it over, or buying the exploration licence that sort of thing – will depend upon the price of the mineral output at that time. But once you’re up and running then your revenues vary with the global market for your production. All mines, that is – well, very nearly all – are commodity producers, they’re price takers in the market. You’re producing gold, iron ore, lithium, you get the global gold, iron ore, lithium price. But your costs do not vary according to that price. They vary according to the general inflation rate. So, changes in the price you get for your output move directly thought to the bottom line, the profits. Mining profits are geared, leveraged, to minerals prices that is.

Which is great when profits are going up – like when Pilbara bought the Altura mine. Not so good now that lithium output price is going down.

The economics of mining lithium really matters

Which is some half of the economics of mining companies. The other half is that there’s really no shortage of any mineral or element out there. The whole world is made of only the 90 same things. Which means that if we really want some more there’s plenty out there. Think of gold – we currently happily mine rock at 1 gramme, 2 grammes, per tonne. That’s 1 or 2 ppm, parts per million. There are very few elements that are less than that, on average, in the crust of the Earth.

So, we all want more lithium? Sure, there’s plenty out there. It’s a matter of finding it, effort, not base and general availability. Further, that recent price rise has meant that a lot of people think it worth going looking. As we’ve said before here, many have found it too.

Which is what then causes the cycle in mining. Demand changes – technology changes – and so prices rise. Often considerably, those currently mining that mineral for that element make fortunes. But as Adam Smith pointed out, easy profits encourage others to repeat the process, to copy. So, give it a few years and more of that same production comes online. At which point market prices fall and that gearing to profits of the market price goes into reverse. The usual end for a mining boom is as with Altura – entirely viable mines go bust because production revenues can’t keep up with finance costs. When a market becomes really oversupplied, not even with production costs.

Lithium mining is always about positions and trades, not investments.

What this means, in the end, is that it’s rare to find a mining investment. They’re all, always, trading positions. Yep, Pilbara Minerals really is one of the best, finest, deals ever done in the minerals industry. Still worth shorting it at the next point in the cycle.