Macroeconomic/ geopolitical developments

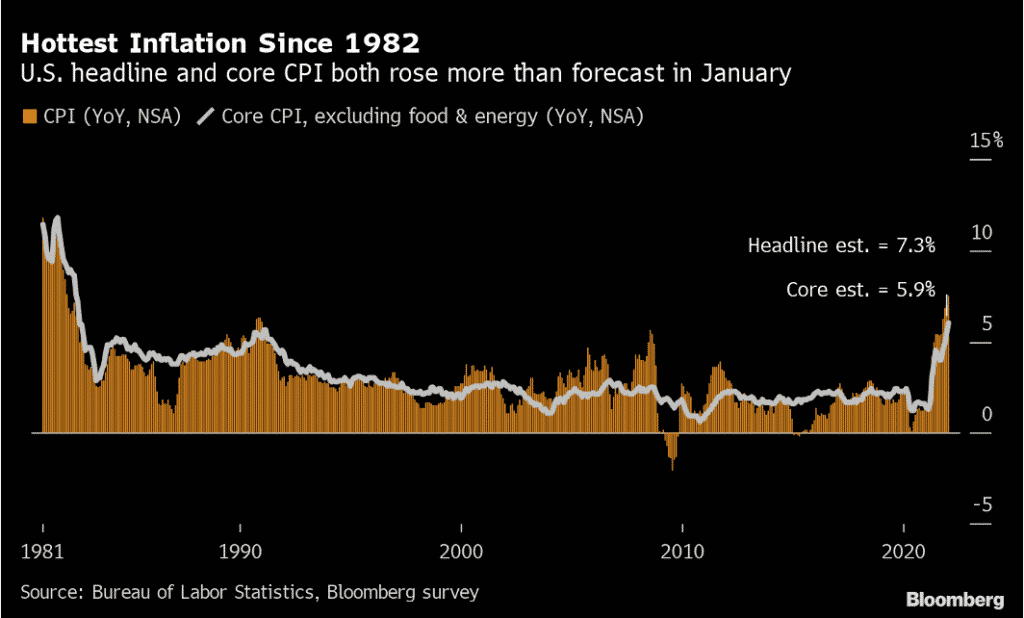

- Another inflationary shock to the upside with the release of the US CPI data on Thursday that saw a print of 7.5% on an annual basis, above consensus estimates and at its highest level for 40 years, since 1982.

- The surging inflation data from the US (and globally so far in 2022) has reinforced the expectations of an even more hawkish reaction from the major, global central banks.

- The more hawkish members of the FOMC are now indicating a possible 0.5% increase at the March meeting with Goldman Sachs now predicting 7 rates hikes this year, one at each meeting in 2022.

- Although the European Central Bank and President Christine Lagarde pivoted towards a tightening stance at their early February meeting, in subsequent comments ECB members including Lagarde have tried to calm market fears of a significantly more hawkish shift.

- The end of last week saw a “risk off” theme reinforced by indications from the US that conflict between Russia and Ukraine could be imminent.

Global financial market developments

- Again, global stock averages were extremely erratic last week, but concerns over the possible conflict between Russia and Ukraine, alongside global yields spiking higher saw a weak close to the week, led by the US indices and in particular the tech sector.

- Higher yield pressures extended through last week, with US Treasury yields at multi-year highs and the US 10yr Note breaching the psychological 2% level, though yields did fall on Friday with a safe haven bond rally given worries over the possible conflict between Russia and Ukraine.

- The US Dollar rallied, undoing some of the prior week’s losses, with a safe haven bid, plus benefiting from the higher US yields and wider yield differentials.

- Gold surged, even with a firmer US Dollar, as a safe haven and inflation hedge.

- Oil again extended its rally into 2022, to yet another new multi-year high.

- Copper tried to breakout to the upside, but fell at the end of the week, but has a more positive bias in broader range.

Key this week

- Geopolitical focus: Closely watching for military developments on the Ukrainian/ Russian border.

- Central Bank Watch: The only Central Bank activity of note are the release of the RBA and FOMC Minutes on Tuesday and Wednesday respectively.

- Macroeconomic data: the UK Employment and CPI data, alongside US Retail Sales are the standout data points for the week.

| Date | Key Macroeconomic Events |

| 14/02/22 | Nothing of note |

| 15/02/22 | RBA Minutes; Japan GDP; UK Employment report; EU GDP; German ZEW survey; US PPI |

| 16/02/22 | UK CPI; US Retail Sales; Canada CPI; FOMC Minutes |

| 17/02/22 | Australia Employment report |

| 18/02/22 | Japan CPI; UK Retail Sales; Canada Retail Sales |