Macroeconomic/ geopolitical developments

- We got the US Federal Open Market Committee (FOMC) interest rate decision, statement and press conference on Wednesday and although markets moved initially to a “risk on” theme after the statement, the press conference saw a “risk off” shift, as, markets interpreted comments from Fed Chair Jerome Powell as opening the door to an even more hawkish tone than markets had previously anticipated.

- The Fed has prepared markets for a March move higher in interest rates and Powell stated that “there’s quite a bit of room to raise interest rates without threatening the labor market”, which saw money markets and interest rate futures price in five rate hikes for 2022.

- The “risk off” environment has also been impacted by ongoing tensions from the threat of conflict as Russia continues to amass troops on the Ukrainian border, although in the very short-term a diplomatic solution is being sort.

- Earnings season has continued in the U.S. with Microsoft and Apple providing some strong data for Q4 2021 and positive guidance, whilst Tesla’s numbers were very positive, the forward guidance warned of ongoing supply chain concerns.

Global financial market developments

- Global stock averages were extremely erratic last week, led by the US indices and in particular the tech sector.

- However, most indices avoided moving below the lows set earlier in January and posted resilient rebounds on Friday, hinting at potential for basing patterns and recovery into February

- Higher yield pressures from early January have eased, with US (and global) Bond consolidating, though the US Yield Curve has flattened, which is of concern.

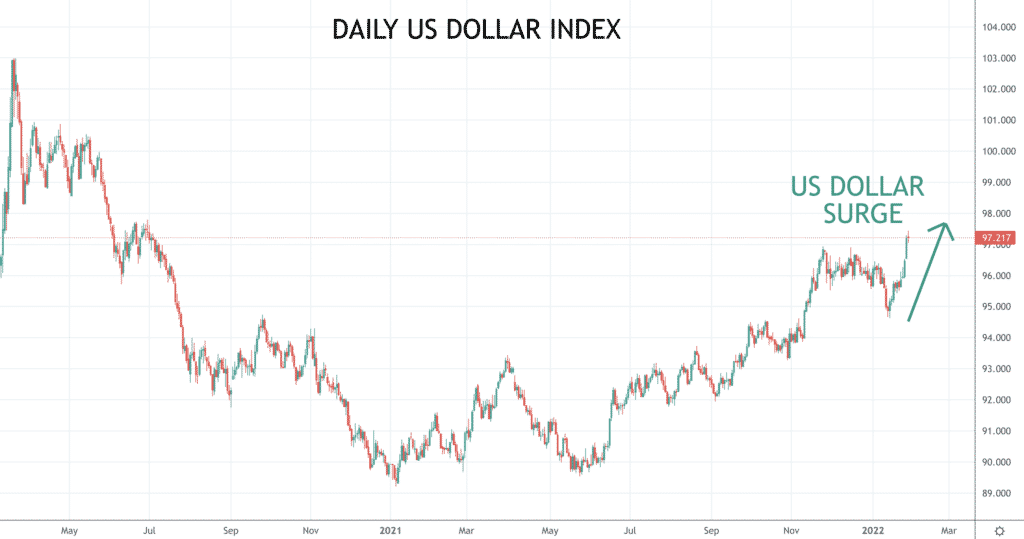

- The US Dollar and has further strengthened in the “risk off” environment, assisted by the more hawkish tone from the US Federal Reserve.

- Commodity currencies, the Australian, New Zealand and Canadian Dollars were once again notably weaker versus the greenback, with the antipodean currencies moving to multi-month lows.

- Gold set a more aggressively negative tone, driven by the stronger US Dollar.

- Oil further extended its late 2021 rally into 2022 to a new multi-year high.

- Copper now has a negative tone within a broader range, driven by the US Dollar strength.

Key this week

- Geopolitical focus:

- The Chinese Lunar New Year see Chinese markets closed all next week, Monday 31st January-Friday 4th February.

- Watching the potential for military or diplomatic developments regarding the Ukrainian/ Russian tensions.

- Central Bank Watch: We get the Reserve Bank of Australia (RBA) interest rate decision, statement and press conference on Tuesday and the same from the Bank of England (BoE) and European Central Bank (ECB) on Thursday.

- Macroeconomic data: An extremely busy data week with German and EU Retail Sales, EU GDP and CPI, global Markit and US ISM Manufacturing, Services and Composite PMIs, and the US and Canadian Employment reports.

- Earnings data: US earnings season continues with standouts being Google (Alphabet), Exxon Mobil, Meta, Amazon, and Merck.

| Date | Key Macroeconomic Events |

| 31/01/22 | Chinese Lunar New Year, Chinese markets closed all week; EU GDP; German CPI |

| 01/02/22 | RBA interest rate decision, statement and press conference; German Retail Sales; global Markit and US ISM Manufacturing PMI |

| 02/02/22 | EU CPI; US ADP Employment Change |

| 03/02/22 | Global Markit and US ISM Services and Composite PMI; BoE and ECB interest rate decisions, statements and press conferences |

| 04/02/22 | EU Retail Sales; US Employment report; Canadian Employment report |