Macroeconomic/ geopolitical developments

- US equities retreated from record highs on Friday as rising Treasury yields, persistent inflation concerns and geopolitical uncertainty weighed on sentiment, erasing much of the week’s earlier gains. Despite the late sell-off, the S&P 500 still rose 0.1% for the week, while the Nasdaq fell 0.1% and the Dow Jones Industrial Average declined 0.2%, with strength in energy stocks partially offsetting weakness in growth sectors.

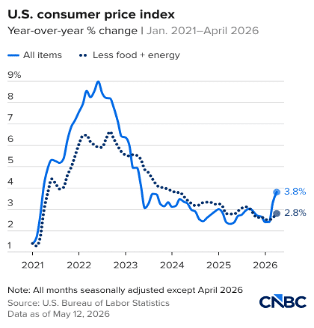

- US inflation remained a key market concern after April CPI rose 0.6% month-on-month and 3.8% year-on-year, marking the highest annual inflation reading since May 2023. Strong producer price data and resilient retail sales added to that narrative, pushing Treasury yields higher as the 10-year rose to 4.59% and the 2-year climbed to 4.09%, further reducing expectations for near-term rate cuts.

- Geopolitical developments remained in focus as the Trump-Xi summit helped ease near-term trade tensions, with both leaders signalling a commitment to stable economic relations despite limited concrete policy outcomes. Meanwhile, progress in the Middle East remained muted, as stalled US-Iran negotiations and ongoing uncertainty around the Strait of Hormuz kept risks to energy prices, inflation and broader market sentiment elevated.

- Investors will closely watch Nvidia earnings this week, with results and guidance expected to provide a key test for AI-driven market optimism and broader spending trends across data centres and hyperscalers. Attention will also turn to the latest Minutes from the Federal Reserve and global flash PMI data, which should offer fresh insight into the interest rate outlook and whether economic growth remains resilient amid higher energy prices and ongoing geopolitical uncertainty.

Global financial market developments

- US and global equity averages were mostly, slightly lower.

- US and European bond yields were notably higher on the week

- The US Dollar Index moved to a multi-week high.

- Gold futures slipped towards a multi-week low.

- Oil futures prices rallied through the week, close to a multi-year peak.

Key this week

Central Bank Watch: Central banks will be in focus this week, with the release of the Minutes from the latest Federal Open Market Committee Meeting on Wednesday likely to attract the most attention. Investors will also monitor the Reserve Bank of Australia Meeting Minutes Tuesday and the People’s Bank of China Interest Rate Decision Wednesday.

Macro Data Watch: Macro data will be in focus this week, with Global Flash PMI releases on Thursday expected to provide the clearest read on economic momentum across major economies. Investors will also be watching Chinese Retail Sales on Monday, UK Employment reports Tuesday, UK Inflation figures Wednesday and UK Retail Sales Friday.

Earnings Watch: US first quarter earnings season enters its final stretch this week, with Nvidia, the final member of the ‘Magnificent Seven’ to report on Wednesday. Investors will also be watching retail updates from Home Depot on Tuesday and Walmart on Thursday.

| Date | Major Macro Data |

| 05/18/2026 | EU G7 Meeting; Chinese Retail Sales and Industrial Production |

| 05/19/2026 | EU G7 Meeting; Japanese GDP; RBA Meeting Minutes; UK Employment reports; Chinese CPI; US Pending Home Sales |

| 05/20/2026 | PBoC Interest Rate Decision; UK CPI, PPI and RPI; FOMC Minutes |

| 05/21/2026 | Global Flash PMI; German PPI; EU Consumer Confidence; US Building Permits, Housing Starts and Philadelphia Fed Manufacturing Survey |

| 05/22/2026 | UK Consumer Confidence and Retail Sales; Japanese CPI; German Consumer Confidence and GDP; Canadian Retail Sales; US Michigan Consumer Sentiment and Consumer Inflation Expectations |