Macroeconomic/ geopolitical developments

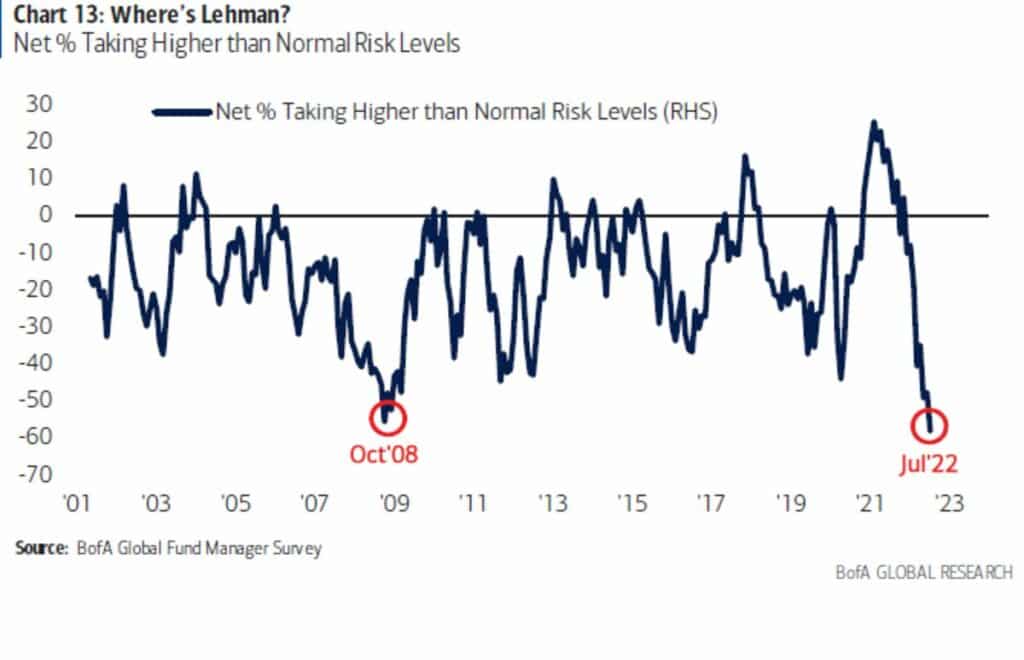

- The Monthly Fund Manager Survey from Bank of America showed that funds’ cash holdings are at their highest levels since 9/11, and equity exposure at the lowest levels since the 2007–2009 global financial crisis and recession.

- This can be viewed as a contrary indicator, meaning that there is plenty of cash to be put to work with possible moves from underweight back towards neutral equity exposure as stock markets rally.

- A more robust earnings season than foreseen so far was typified by Netflix reporting this past week, they had lost fewer subscribers than anticipated in Q2 and predicted resuming subscribers this year. Netflix shares rose by about 15% last week!

- The European Central Bank (ECB) raised interest rates for the first time in over a decade by 0.5%, and announced the Transmission Protection Instrument, which is a new bond-buying tool introduced to counter the possible surge in borrowing costs, particularly for the “periphery” members of the Eurozone.

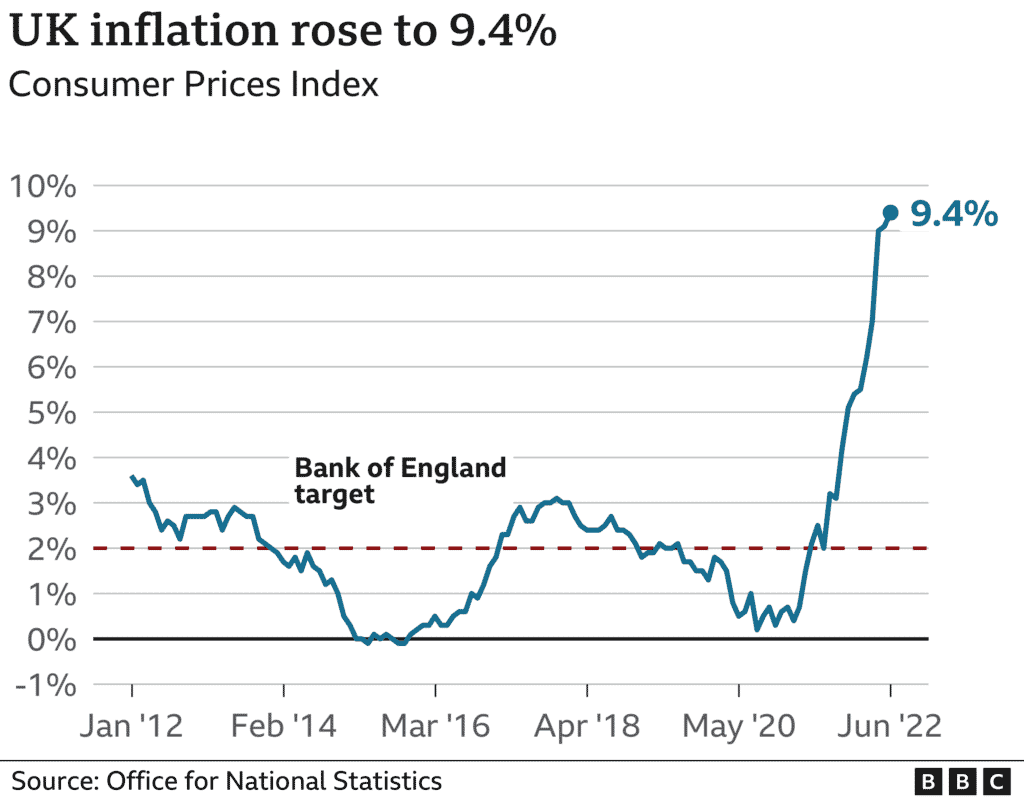

- UK CPI data hit another new 40-year high at 9.4% YoY in June, above forecasts and up from 9.1% in May.

Global financial market developments

- The major US stock averages were higher last week and produced bullish technical signal, pushing above notable resistance barriers, reinforcing bases from June and aiming still higher.

- European and Asian equity indices were also positive, sending intermediate-term bottoming signals.

- US 10yr yields tracked still further below 3.00% close to May yield lows, with lower yield activity since the mid-June FOMC Meeting still encouraging lower yield pressures.

- The US Dollar Index sold off from the mid-July multi-year high and signals a top, with risk shifting lower.

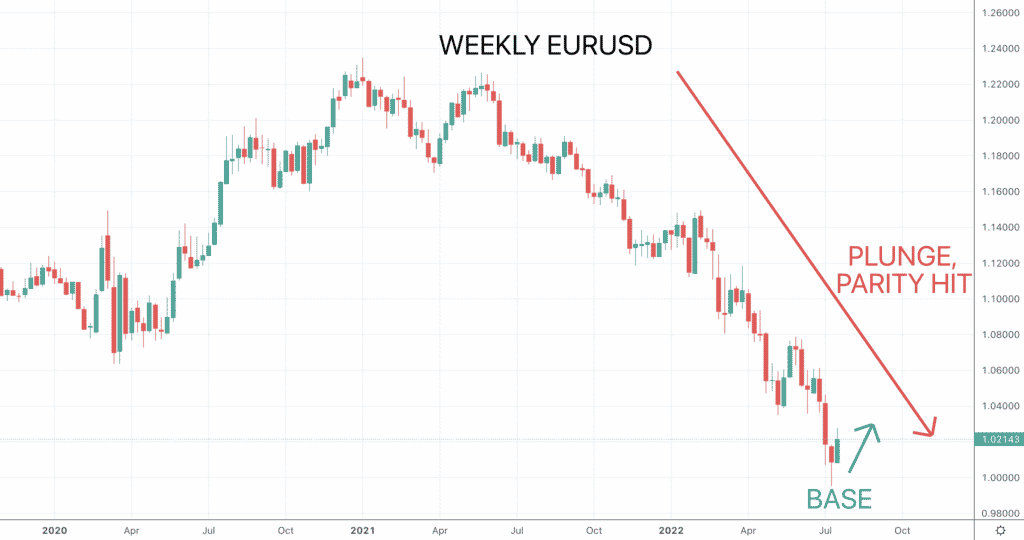

- EURUSD has rebounded having broken below the much-watched level of parity (1.0000) and is basing, aiming higher.

- Gold plunged again and the bounced from 2021 supports, hinting at a basing pattern and upside risks.

- Oil consolidated last week unable to build on the prior week’s rebound, with bigger risks still skewed lower.

- A cautious rebound effort for Copper after the plunge from June and although hinting at a base, for now stays negative.

Key this week

- Geopolitical focus: Still monitoring the war in Ukraine.

- Central Bank Watch: We get the Federal Open Market Committee (FOMC) interest rate decision, statement and press conferencs on Wednesday.

- Macroeconomic data: On the data front he German IFO Survey and CPI, US Consumer Confidence, Durable Goods and Personal Consumption Expenditure (PCE) data are the standouts for the week.

- Microeconomic data: US earnings season is in full swing with Big Tech in the focus, as Microsoft, Alphabet (Google), Meta (Facebook), Boeing, Apple, Amazon, Exxon Mobil and P&G all report in the coming week.

| Date | Key Macroeconomic Events |

| 25/07/22 | German IFO Survey |

| 26/07/22 | US Consumer Confidence |

| 27/07/22 | Australian CPI; US Durable Goods; Fed interest rate decision, statement and press conference |

| 28/07/22 | Australian Retail Sales; German CPI; US GDP & PCE |

| 29/07/22 | Japan CPI, Unemployment, Industrial Production and Retail Trade; German GDP and Unemployment; EU GDP; US PCE |