Macroeconomic/ geopolitical developments

- The financial markets have again been dominated by the Russian invasion of Ukraine, with shifts between “risk on” and “risk off” themes.

- Further punitive sanctions including the US barring Russian oil imports has increased the threat to global trade and global economic growth.

- Global commodity prices have again risen aggressively, but also plunged back lower, with wheat, nickel and energy prices still in focus.

- Ongoing inflation pressures from surging commodity prices and the potential for a negative impact on growth rates has raised the spectre of stagflation.

Global financial market developments

- Global stock averages were erratic last week with markets closing weak and near to the weekly lows in many instances, given the developing conflict in Ukraine alongside stagflation worries.

- US share indices were mostly lower, led by the tech sector, with the Nasdaq Composite at its intraday low on Tuesday falling to 22% below its record peak from November 2021, through the 20% level that indicates a bear market.

- European and U.K. averages also suffered significant damage early in the week, though did recoup much of those losses by the end of the week.

- Higher yield pressures increased last week as safe-haven pressures from the Russia/ Ukraine conflict gave way to stagflation fears.

- The US Dollar surged against the Euro, Pound and Japanese Yen.

- “Risk/ commodity currencies” the Australian, New Zealand and Canadian Dollars were more cautious as the surging commodity rally stalled.

- Gold surged again as the ultimate safe haven, but also suffered notable losses for a a likely short-term (at least) blow-out top.

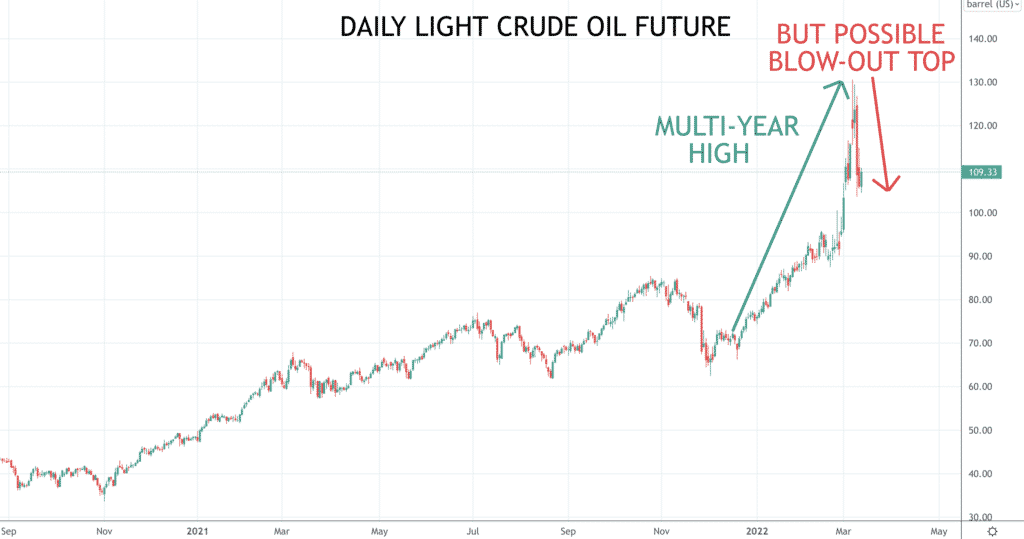

- Similarly, Oil surged to another new multi-year high, just above $130, but also suffered notable losses for a likely short-term (at least) blow-out top.

- Copper reversed the prior, strong rally for a bullish breakout (from within a broader range to a multi-year high), for a potential breakout failure.

Key this week

- Geopolitical focus:

- Still closely monitoring the military escalation in Ukraine.

- Also watching for potential for talks to improve and maybe a ceasefire.

- The US moved to Daylight Savings Time on Sunday 13th March.

- Central Bank Watch: We get the Reserve Bank of Australia (RBA) Meeting Minutes on Tuesday and the Federal Open Market Committee (FOMC) interest rate decision, statement and press conference on Wednesday and the same from the Bank of England (BoE) on Thursday and the Bank of Japan (BoJ) on Friday.

- Macroeconomic data: The key data point for the week will be the release of US Retail Sales on Wednesday.

| Date | Key Macroeconomic Events |

| 14/03/22 | Nothing of note |

| 15/03/22 | RBA Meeting Minutes; China Retail Sales; UK Employment report; German ZEW Survey; US PPI |

| 16/03/22 | US Retail Sales; Canada CPI; FOMC interest rate decision, statement and press conference |

| 17/03/22 | New Zealand GDP; Australia Employment report; BoE interest rate decision, statement and press conference |

| 18/03/22 | Japan CPI; BoJ interest rate decision, statement and press conference; Canada Retail Sales |