Macroeconomic/ geopolitical developments

- The financial markets have once more been dominated by the Russian invasion of Ukraine, but with a shift towards more of a “risk on” theme through mid-March.

- This has been driven by hopes from minimally positive signals from the Ukraine/ Russia talks.

- And, although there have been some upsetting impacts on civilians, there has not been a majorly negative escalation, nor have Russian troops made significant progress in the conflict.

- Global commodity prices have continued their downside corrections from the aggressive surges seen from latter February into March.

- Markets remain worried about inflationary pressures from tight labour markets and surging commodity prices and the risks to global growth, with the threat of stagflation.

- The US Federal Open Market Committee (FOMC) interest rate decision, statement and press conference came on Wednesday and brought the expected lift off in interest rates, with a 0.25% rate rise and an indication that there will be a further 0.25% increase at each of the meetings through 2022.

- However, financial market reactions were muted, as this was priced in, with little surprises from the statement or press conference, though US yields did nudge higher.

- The Bank of England (BoE) also raised interest rates on Thursday, for the third time, now up to 0.75%, but again, the market impact was somewhat subdued, though Gilt yields have actually fallen.

Global financial market developments

- Global stock averages were significantly higher last week with markets closing strong on Friday and near to the weekly highs in many instances, with hoes from the Ukraine/ Russia talks and with the FOMC and BoE addressing inflation/ stagflation worries.

- US share indices were notably higher, led by the tech sector, with the Nasdaq posting a strong rebound after signalling a bear market the prior week.

- European and U.K. averages also produced significant recoveries building on the rebounds from the prior week.

- US higher yield pressures continued last week with the Fed rate hike and inflation/ stagflation fears.

- Despite US higher yield moves, the US Dollar retreated, and the US Dollar Index is threatening a topping pattern.

- “Risk/ commodity currencies” the Australian, New Zealand and Canadian Dollars have maintained a positive theme against the US Dollar with the “risk on” theme, despite the correction lower in commodity markets.

- Gold suffered notable losses again to confirm a short- and even intermediate-term blow-out top (after the latter February/ early March surge as the ultimate safe haven).

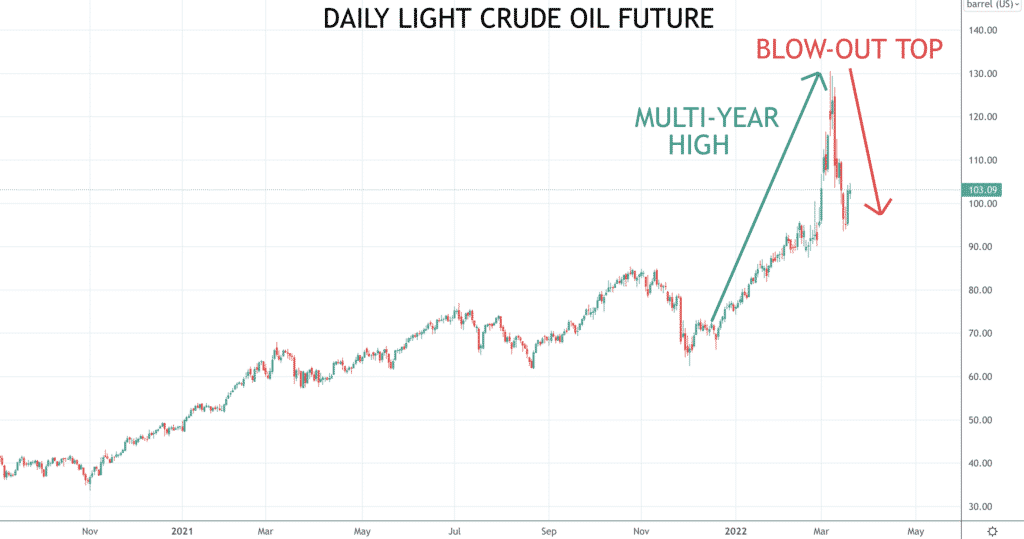

- Similarly, Oil suffered notable losses to confirm a short- and even intermediate-term blow-out top (after the early March surge), down from above $130 to push below $100 at one point.

- Copper rebounded last week to try to resume the early March, strong rally for a bullish breakout and to try to reject the subsequent setback as a breakout failure.

Key this week

- Geopolitical focus:

- Still closely monitoring potential for Ukraine/ Russia talks to improve and maybe for a ceasefire.

- Also watching for a possible military escalation in Ukraine.

Central Bank Watch: We get Fed Chair Powell speaking on Wednesday and the Meeting Minutes from the Bank of Japan (BoJ) on Thursday.

- Macroeconomic data: The key data points for the week will be the release of UK CPI and Retail Sales on Wednesday and Friday respectively, with the UK Spring Budget Statement also on Wednesday, plus global Markit Flash PMI and US Durable Goods Orders are all released on Thursday.

| Date | Key Macroeconomic Events |

| 21/03/22 | Nothing of note |

| 22/03/22 | Nothing of note |

| 23/03/22 | UK inflation data including CPI; UK Spring Budget Statement; Fed Chair Powell speaks |

| 24/03/22 | BoJ Meeting Minutes; global Markit Flash PMI; US Durable Goods Orders |

| 25/03/22 | UK Retail Sales; German IFO Survey |