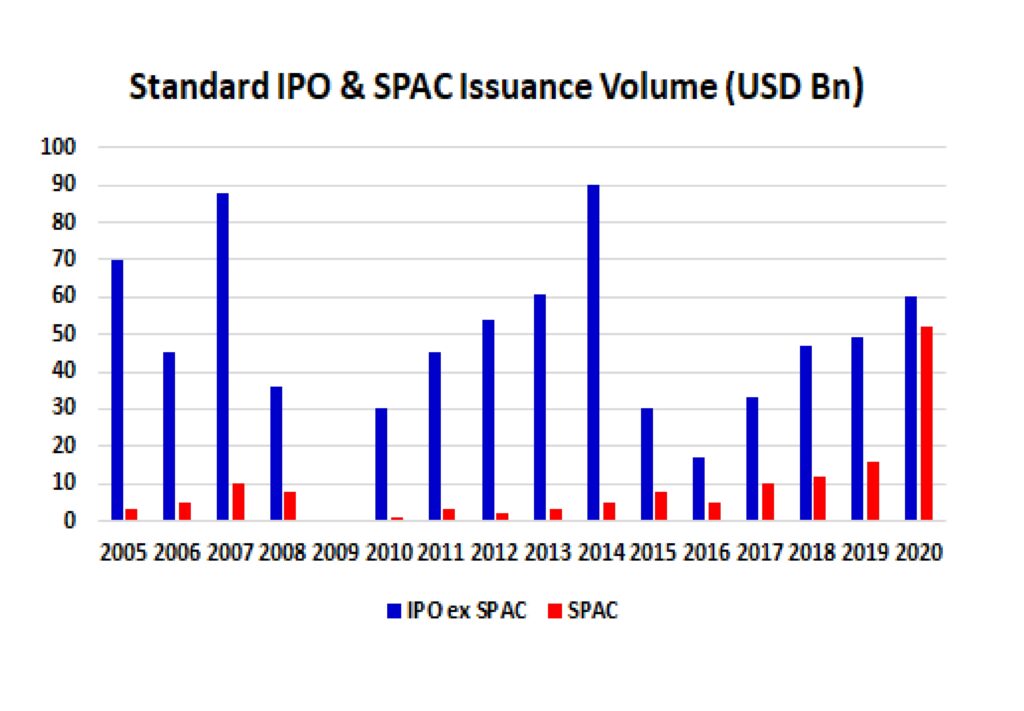

- SPAC issuance value almost matched IPO’s

- Listing process needs sensible and firm regulation

- Investors must evaluate each prospectus fully

- Collateralized SPAC funds of funds could arise

What Is a Special Purpose Acquisition Company (SPAC)?

A special purpose acquisition company (SPAC) is a company with no commercial operations that is formed specifically to raise capital through an initial public offering (IPO) with the intention of acquiring an existing private company.

They are sometimes called “blank cheque companies,” and just because they have recently hit the news headlines they are not a new an innovation.

SPAC’s have been around for decades, however, recently they have become popular for investors and have almost caught the new issue volume of mainstream floatation’s or IPO’s.

In 2009 there was just a single SPAC listing cf. 248 in 2020.

How does a SPAC work?

SPAC’s, in the main, are formed by investors, or sponsors, who possess expertise in a specific industrial sector. Their objective is to seek a privately held company operating in that area that can be acquired and hopefully grown.

It is usual for the creators of the SPAC i.e. the founders to have at least one acquisition target in mind. They will not disclose the target to avoid the need for extensive disclosures during the IPO process and for this reason they are often called “blank cheque companies”. That implies the investors at the time of capital raising have no clear picture as to what company they will be investing in. SPAC’s seek underwriters and institutional investors before offering shares to the public.

Usually money is raised by selling units worth USD10. These compromise one share and one warrant or partial warrant. The warrants allow investors to by a specified number of shares at a specified price at or after a specific future date.

Money raised by SPAC’s in an IPO is placed in an interest-bearing trust account that in turn invests in money market funds or short-term government securities. In some cases, some of the income earned from the trust can be used as the SPAC’s working capital. The sponsors then have between 18 and 24-months to acquire a company they believe has excellent potential. If no acquisition deal is made the SPAC will face liquidation.

In the cases where an acquisition is made the SPAC and target company are merged into a publicly traded company listed on one of the major stock exchanges. This is what is known as the “De-SPAC” process and once complete, investors can decide if they wish to stay invested and see their investment rise or fall in the broad market. However, they can liquidate their holding at this stage.

Advantages of a SPAC

Selling to a SPAC can be an attractive option for the owners of a smaller company, which are often private equity funds. The main advantages are:

- To bypass traditional IPO demands

- Acquisition by a SPAC offers a faster IPO process with guidance of an experienced partner

- Selling to a SPAC can add up to 20% to the sale price cf. a typical private equity deal

- It increases price certainty

- Investors are attracted to the early opportunity to invest

Reputation and Regulation

SPAC’s have on occasion earned a bad reputation as not every investment works out, however, that is true for many primary (new) and secondary market investment decisions.

In the year to date (2021), as detailed by SPAC Research, there have been more than 300 listings, cf. 248 in all of 2020. Within those SPAC listings the PYMNTS/SPAC Tracker indicates that to April 9, there have been 13 banking/financial services IPOs, and 11 payment-related issues.

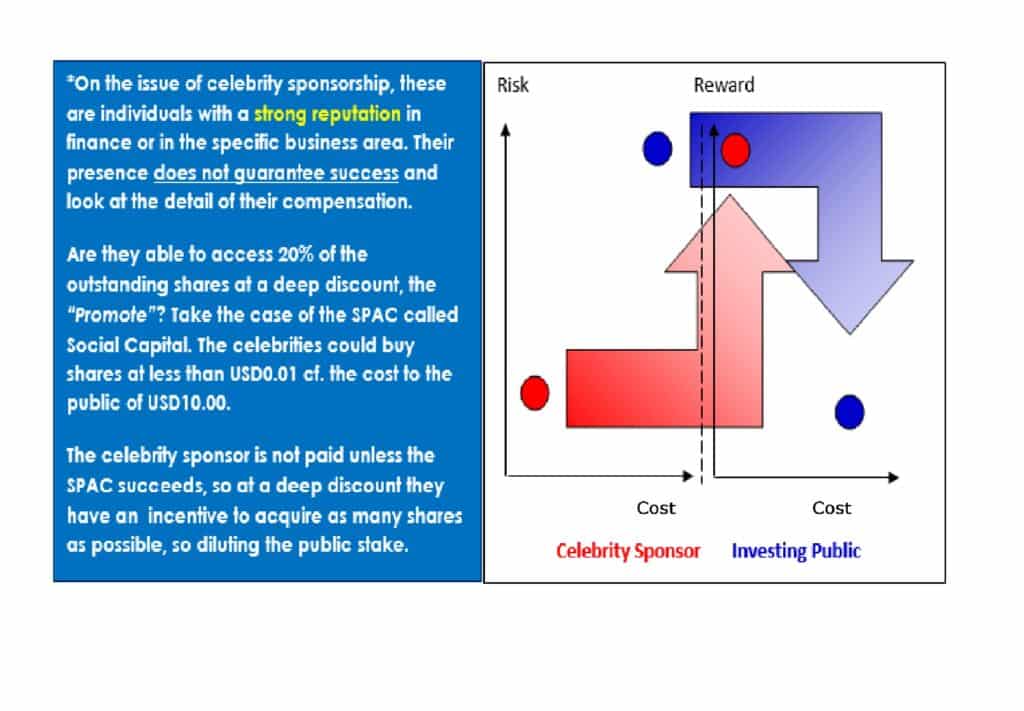

On the subject of concern, the most often raised issues include fee risk, conflicts of interest amid the sponsors*, compensation for sponsors, sponsorship by celebrities and the risk to the retail investor enticed by unjustified hype. In short, the amount of capital that has been drawn to SPAC’s, has also drawn a regulatory spotlight.

To counter the negative connotations national securities exchanges have responded with new rules that frame the process by which SPAC’s are listed.

The Securities and Exchange Commission (SEC), warned investors in a report released in March:

“…not to make investment decisions related to SPAC’s based solely on celebrity involvement. … celebrities, like anyone else, can be lured into participating in a risky investment or may be better able to sustain the risk of loss. …”

At the end of March, the SEC issued statements on the considerations for examination by private companies that were contemplating a SPAC transaction with a high focus on accounts and records that would prove pertinent to an eventual distribution of assets or particulars related to transactions.

The SEC wrote :

“…It is critical that the board of directors, audit committee, management, and auditors of these operating companies fully understand and fulfil their respective professional responsibilities so that companies meet their obligations under the federal securities laws and investors are provided with high-quality financial reporting at the time of the merger and on an ongoing basis in subsequent periods. …”

It not only in the US that there is concern. On March 31, the Financial Conduct Authority (FCA), the UK’s financial supervisory authority confirmed it will be consulting in the near future on amendments to rules and regulation pertaining to SPAC’s.

The “Listing Rules” and related guidance will be revised to strengthen protections for investors, according to the FCA.

“…Where such protections are in place, we consider that the existing presumption of suspension of the listing for such companies at the point of announcement of an acquisition target is no longer required and we, therefore, intend to consult on this basis, aligning this element of our rules more closely with other major jurisdictions …”

The FCA will consider structural features and enhanced disclosure, including a minimum market capitalisation and a redemption option for investors, required to provide a suitable level of investor protection.

Of course, investors cannot expect regulation to be a sweeping safety net. They must conduct due diligence and bear three key facts in mind before committing capital.

- Management Team…there are no assets, no product or track record and what is the promote

- If a target company is identified, is it a good option?

- Look at the opportunity costs

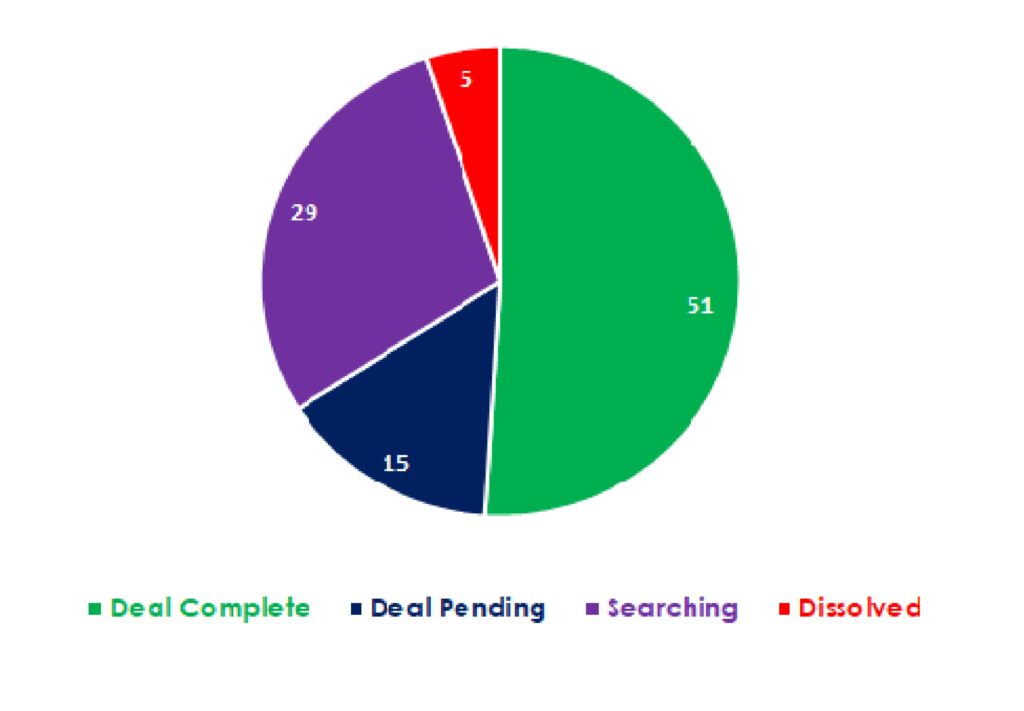

In considering a SPAC and opportunities elsewhere one should bear in mind data that was published last year showing the recent success rate of “De-SPACing”.

Is the boom slowing?

The pace of SPAC issuance has certainly been impressive, however, there are signals that investors are increasingly willing to take a longer, harder look before committing capital.

The market capitalisation of Virgin Galactic (NYSE:SPCE) has fallen from USD13.0 Billion on February 11 to USD5.34 Billion at the close on April 29. In another example Opendoor Technologies Inc. (NASDAQ: OPEN) has its value decline from USD 20.69 Billion on February 11 to USD 12.02 Billion at last nights close.

There is also a rise in the number of short sellers in SPAC’s as the market grows sceptical and following a vigorous start to the year one sees a mere USD 2.5 Billion has been raised since the end of March. We may be through the froth and hype and starting to see this vehicle maturing.

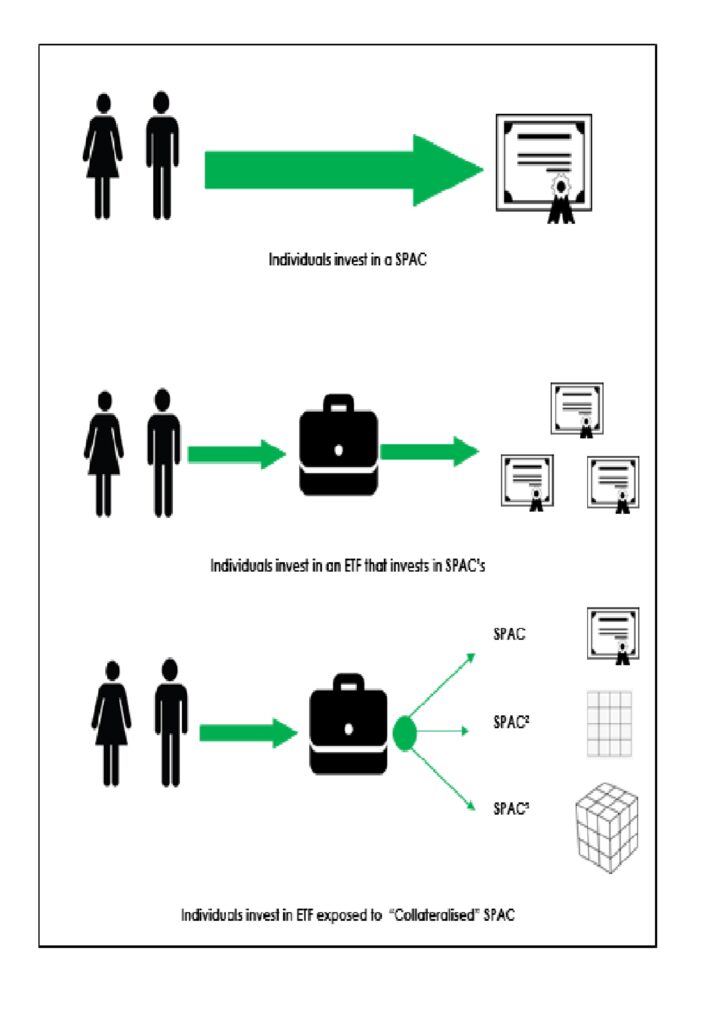

A possible danger

One can use an exchange-traded fund (ETF) to gain exposure to SPAC’s. These funds typically include a range of companies that recently went public by merging with a SPAC and SPAC’s that are still searching for a target to take public.

At Spotlight we have a slight concern as in the attempt to spread a wide net and perhaps enhance returns could we see a situation where the progression is scaled up as was the case in the mortgage market in the early years of this century in the hunt for enhanced returns.

This idea may not be so far fetched as funds of funds are popular investment vehicles. However, at a time when regulation is catching up with SPAC issuance this could be a potentially dangerous step. So, as always, one has to stress “Caveat Emptor”…”Buyer Beware”.