Macroeconomic/ geopolitical developments

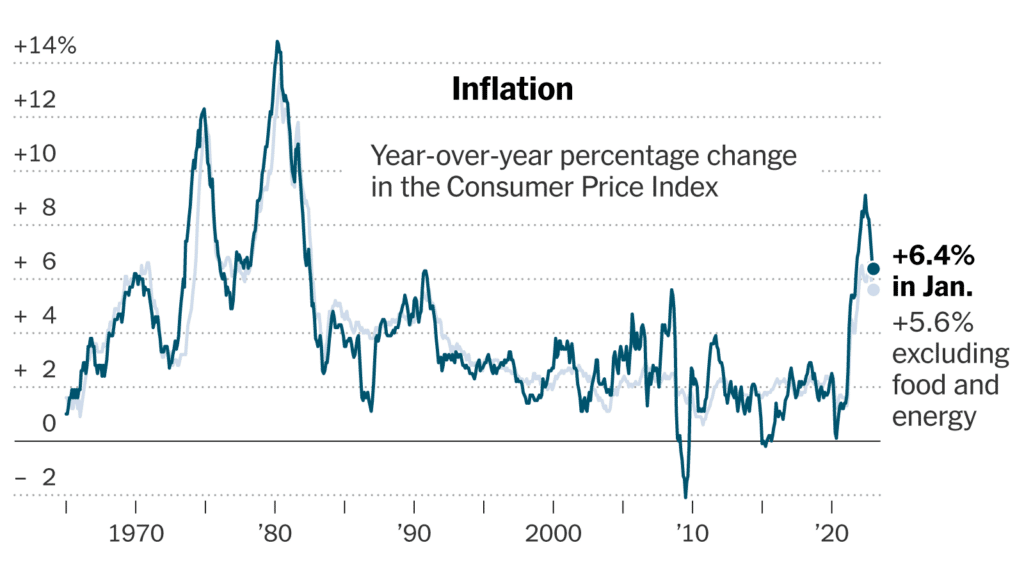

- The US Consumer Price Index (CPI) was the standout data on Tuesday and printed above consensus for both the headline and core data, with the headline CPI rising 0.5% for the month, with a YoY gain of 6.4% (expectations were for 0.5% and 6.2% according to Bloomberg). The core CPI (excluding food and energy) advanced 0.4% in January and was up 5.6% from a year earlier (consensus was for 0.4% and 5.5%, again according to Blomberg).

- These above consensus prints for inflation saw a reaction from Bond and money markets to price in a more hawkish tone from the FOMC, with yields rising across the US Treasury curve and interest rate markets signalling rates moving higher than previously expected and staying there for longer.

- This “higher for longer” theme was reinforced by comments after the data from various Fed officials.

- US Retail Sales data came in stronger than expected on Wednesday, again adding to expectations for a possibly more hawkish Fed.

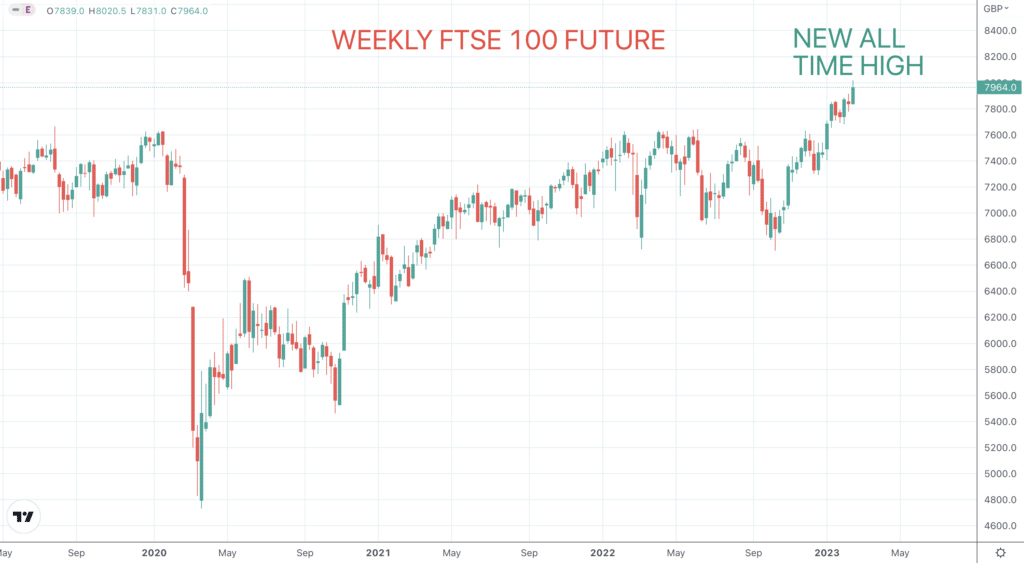

- In the UK, CPI data came in lower than expectations by various measures, headline and core, YoY and MoM, which saw UK yields fall, and saw the UK benchmark stock index, the FTSE 100 hit another new record level.

Global financial market developments

- The major US stock averages marked time last week, whilst European indices saw solid gains last week, reversing the corrective losses from early February.

- The UK index, the FTSE 100 hit another new record level and was joined by the French CAC benchmark average.

- US and European Bond yields were notably higher again last week.

- The US Dollar Index stayed solid last week and slightly extended gains since the strong early February rebound from a multi-month low.

- Gold stayed negative to reinforce the early February plunge from a multi-month high.

- Oil posted a negative consolidation of the earlier February surge from close to multi-month lows.

- Copper bounced after the earlier February sell off from near multi-month highs, for a still negative tone.

Key this week

- Geopolitical Events: Monday 20th February is US Presidents’ Day holiday, US equity and bond cash markets are closed. The equivalent US futures markets are partially closed.

- Central Bank Watch: Monday sees the People’s Bank of China (PBoC) interest rate decision and Tuesday brings the Reserve Bank of Australia (RBA) Meeting Minutes. Then Wednesday we get the standout Central Bank event for the week, the US Federal Open Market Committee (FOMC) releasing the Meeting Minutes from early February.

- Macroeconomic data: Tuesday sees the standout data for the week, the global S&P Global Flash Purchasing Managers Index (PMI) release, with German CPI Wednesday and US GDP and PCE data on Thursday also notable releases.

| Date | Key Macroeconomic Events |

| 20/02/23 | US Presidents day holiday, US equity and bond cash markets are closed; PBoC interest rate decision |

| 21/02/23 | RBA Meeting Minutes; global S&P Global Flash Purchasing Managers Index (PMI); Canada CPI and Retail Sales |

| 22/02/23 | German CPI; German IFO Survey; FOMC Meeting Minutes |

| 23/02/23 | EU CPI; US GDP and PCE |

| 24/02/23 | German GDP; US PCE |