Macroeconomic/ geopolitical developments

- Mixed data saw stocks lower and then rebound last week as durable goods orders posted their steepest decline since the April 2020 pandemic shutdowns.

- Whilst the Institute for Supply Management (ISM) Manufacturing Purchasing Managers’ Index (PMI) pushed higher in February for the first time since May 2022, and Services PMI fell less than consensus expectations, and indicated a modest expansion at 55.1.

- Fed speakers continued their mantra of “higher for longer”, notably from Kashkari and Waller through the middle of the week.

- But Raphael Bostic, Atlanta Federal Reserve President stated that he supported a 0.25% rate hike at the Fed’s March meeting, adding that the “Fed could be in position to pause by mid to late summer.”

Global financial market developments

- The major US stock averages dipped and rebounded last week, as did European indices, which retain a more bullish tone than their US counterparts.

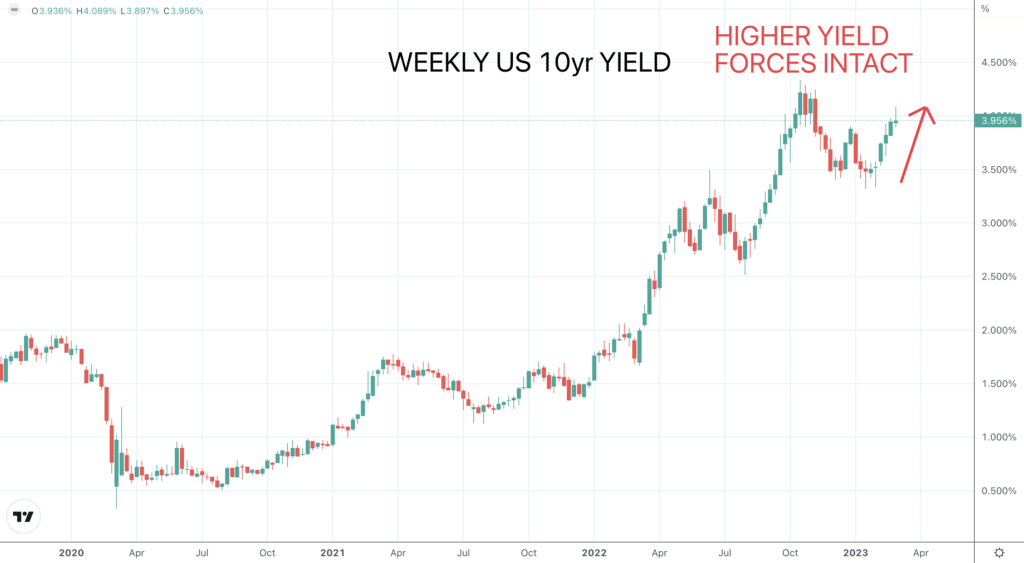

- US and European Bond yields were yet again notably higher last week, with the US 10yt breaking through the 4% level, but Bonds did revery to slightly lower yields on Friday.

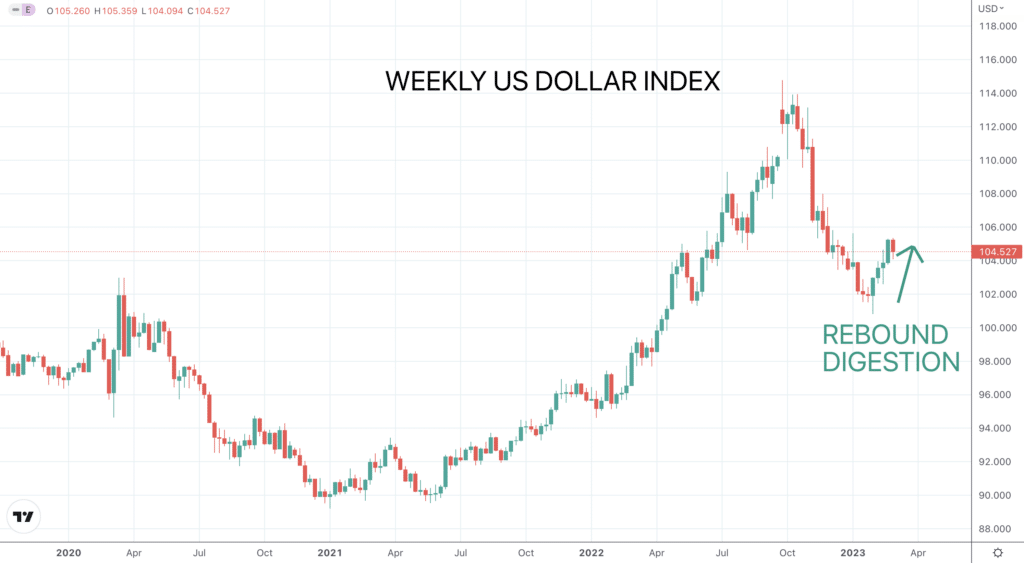

- The US Dollar Index dipped last week, consolidating gains since the strong early February rebound and rally from a multi-month low.

- Gold bounced after the February plunge from a multi-month high.

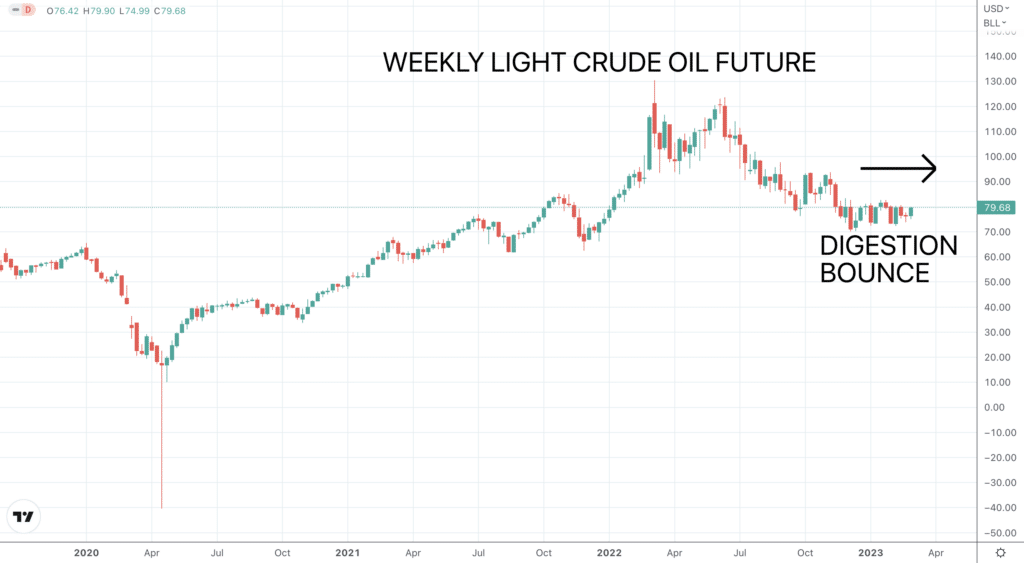

- Oil posted a positive consolidation.

Key this week

- Central Bank Watch: Key focus this week will be Jerome Powell’s testimonies to Congress on Tuesday and Wednesday. We also get the Reserve Bank of Australia (RBA), the Bank of Canada (BoC) and the Bank of Japan (BoJ) interest rate decisions on Tuesday, Wednesday and Friday respectively.

- Macroeconomic data: Friday sees the notable data release with the US Employment report, with German CPI also a standout on Friday, alongside UK GDP, Manufacturing and Industrial Production.

| Date | Key Macroeconomic Events |

| 06/03/23 | EU Retail Sales |

| 07/03/23 | RBA interest rate decision; Jerome Powell testimony to Congress |

| 08/03/23 | German Retail Sales; EU Employment and GDP; ADP Employment Change; Jerome Powell testimony to Congress; BoC interest rate decision |

| 09/03/23 | Japan GDP; China CPI |

| 10/03/23 | BoJ interest rate decision; UK GDP, Manufacturing and Industrial Production; German CPI; US Employment report; Canada Employment report |