Macroeconomic/ geopolitical developments

- Global financial markets stayed in “risk off” mode through mid-December as encouraging inflation data was dismissed, whilst other economic data disappointed and the Fed reiterated that ongoing rate increases are likely

- The much-awaited US Consumer Price Index (CPI) for November was released on Tuesday, with headline inflation rising 0.1% from October, with the YoY gain at 7.1%, the lowest level since December 2021 and below consensus expectations. Core CPI (less food and energy) rose 0.2% to 6.0%, also both below what the market had anticipated.

- On Wednesday the US Federal Reserve announced 0.50% increase in the federal funds target rate, as expected a slowdown in its pace of rate increases

- In the policymakers’ summary, the median projection for the federal funds rate in 2023 is now at 5.1%, above the 4.6% from September, and notably above the peak being priced in by the futures markets.

- Also, the futures markets are continuing to price in a rate cut into the end of 2023, which the Fed is not indicating.

- Thursday saw US Retail Sales released for November, which declined 0.6%, below consensus and the prior two months of data were revised lower.

- Last week we also had four major European central banks in play

- The Bank of England (BoE) hiked for a ninth consecutive increase by 0.5%, to 3.5%, a 14-year high. The European Central Bank (ECB) hiked by 0.5%, to 2.0%, but indicated a higher peak in rates.

- The Swiss and Norwegian central banks also raised rates, by 0.5% and 0.25% respectively.

Global financial market developments

- The major US stock averages fell again last week, having moved initially higher on the encouraging inflation data, but faded through Tuesday’s session. They then plunged on the still relatively hawkish Fed and the fading Retail Sales data, with growing recession fears for 2023.

- European equity indices were also even lower last week, with a still hawkish ECB and BoE.

- US Treasury yields marked time near recent multi-month yield lows, but European yields moved significantly higher after eh ECB.

- The US Dollar Index moved to new multi-month lows but did bounce at the end of the week.

- Gold was erratic and again consolidated the November to a multi-month high but is looking vulnerable to a correction.

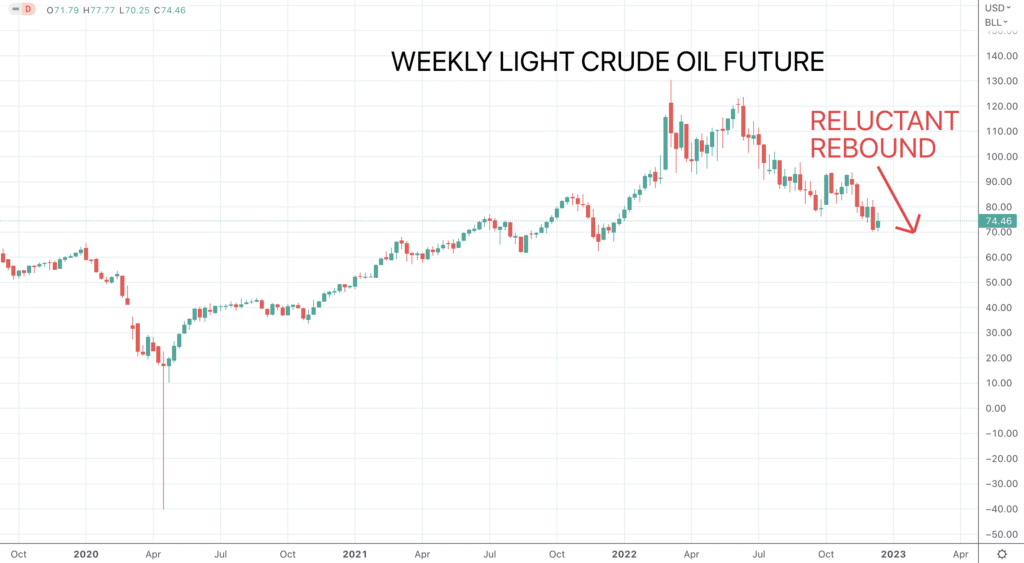

- Oil prices rebounded from a new 2022 low the prior week but rolled back lower into the end of the week, retaining bigger negative pressures.

- Copper saw a notable setback and sets up more negative in a broader range phase.

Key this week

- Central Bank Watch: We get the Reserve Bank of Australia (RBA) Meeting Minutes, the People’s Bank of China (PBoC) interest rate decision and the Bank of Japan (BoJ) interest rate decision, statement and press conference, all on Tuesday.

- Macroeconomic data: A relatively light data week, US GDP and PCE data are the standouts towards the end of the week.

This will be the last MacroWatch report for 2022. Happy holidays to you all, Merry Christmas and wishing you a great trading and investing year for 2023!

| Date | Key Macroeconomic Events |

| 19/12/22 | German IFO Survey |

| 20/12/22 | RBA Meeting Minutes, PBoC interest rate decision; BoJ interest rate decision, statement and press conference; Canada Retail Sales |

| 21/12/22 | Canada CPI |

| 22/12/22 | UK GDP; US GDP and PCE |

| 23/12/22 | US PCE and Durable Goods Orders; Canada GDP |