Macroeconomic/ geopolitical developments

- In response to the US CPI report stock averages chop lower and bounce, with each of the three major U.S. stock indexes experiencing declines exceeding 1%. Bond prices plunged, leading to a surge in bond yields, as the CPI rose beyond forecasts.

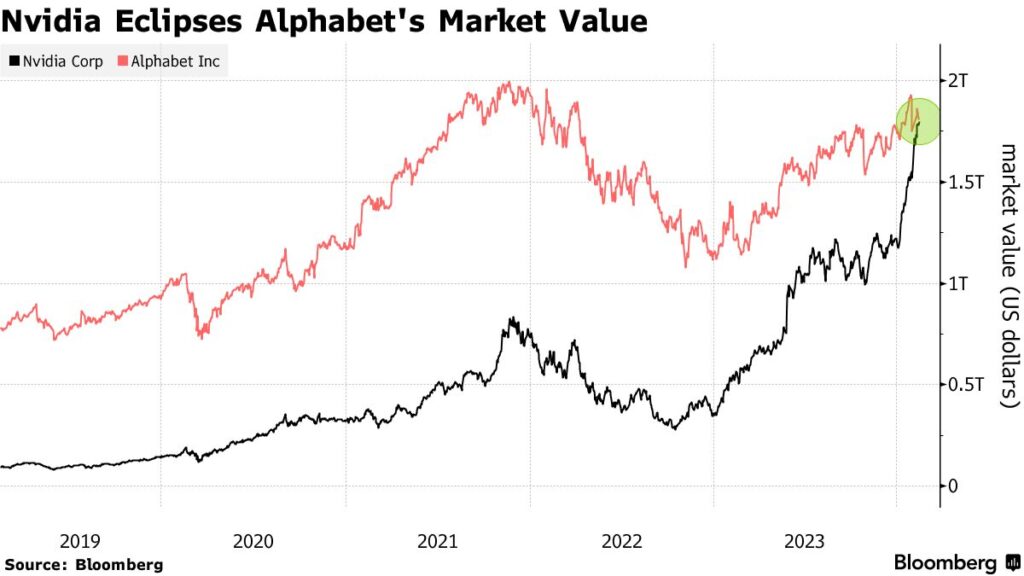

- Nvidia continues to climb higher, due to insatiable demand for its accelerators, which power data centres running AI applications. It overtook Amazon and Alphabet in market cap this week, becoming the world’s fourth-most valuable company.

- Nikkei hit a multi decade high, surpassing the 38,000 mark at the close of trade for the first time since 1990. Investor optimism has rallied due to stronger corporate governance and favourable earnings reports from major companies.

- US CPI came in warmer than expected, rising 3.1% year-over-year in January. On a monthly basis, the index recorded a notable increase of 0.3%, the most significant monthly rise since September.

- Markets have pared back Fed rate cut expectations following hotter than expected U.S. inflation. Odds for a rate cut in May have plummeted to about 32%, down from approximately 64% before the release of the inflation figures.

- US Retail Sales declined more than expected, with a 0.8% drop reported by the US Census Bureau. This was a far greater drop than the forecasted decrease of 0.1%.

Global financial market developments

- Global equity index futures sold off a rebounded last week though the US CPI data

- US and European moved to higher yields.

- The US Dollar Index surged after the US CPI data, then retraced.

- Gold futures broke lower to the lower end of the intermediate-term range.

- Oil futures rebounded further to the upper end of a border range.

Key this week

Holidays: As Asian markets return from the Lunar New Year holidays last week, the US President’s Day holiday is on Monday 19th February.

Central Bank Watch: A relatively quiet week for central banks, but we do see the PBoC Interest Rate Decision Tuesday.

Macro Data Watch: The focus this week will be global manufacturing, services and Flash PMI data Wednesday. We will also see EU CPI release Wednesday.

Earnings Watch: Most of the US earnings calls, but this week sees Walmart and Home Depot Tuesday and Nvidia on Wednesday.

| Date | Major Macro Data |

| 02/19/2024 | Nothing of note |

| 02/20/2024 | PBoC Interest Rate Decision |

| 02/21/2024 | EU Consumer Confidence |

| 02/22/2024 | Global Manufacturing, Services and Composite Flash PMI, EU CPI (MoM, YoY) |

| 02/23/2024 | UK Consumer Confidence; Germany GDP (QoQ, YoY) |