Macroeconomic/ geopolitical developments

- The big data print came from US CPI on Wednesday with the headline number moving to 9.1% YoY, up from the 8.6% print in May and higher than consensus.

- There is now a growing anticipation from short-term interest rate markets that the Fed could raise rates by 1.00% at their meeting on 27th July.

- The US 2-10yr yield curve continues to further invert (a recession signal), last week moving to its most inverted since 2000.

- The Bank of Canada delivered a larger than expected 100bp rate hike, consensus was for 75bp.

- US earnings season kicked off with the financial sector, with JP Morgan and Morgan Stanley both disappointing, though Citigroup was a positive.

Global financial market developments

- The major US stock averages were lower last week but produced strong rebounds after initial weakness.

- European and Asian equity indices were also positive, still sending short-term bottoming signals.

- US 10yr yields were back below 3.00% into mid-month, with the lower yield activity since the mid-June FOMC Meeting still encouraging lower yield pressures.

- The US Dollar Index surged to yet another new multi-year high last week and stays bullish

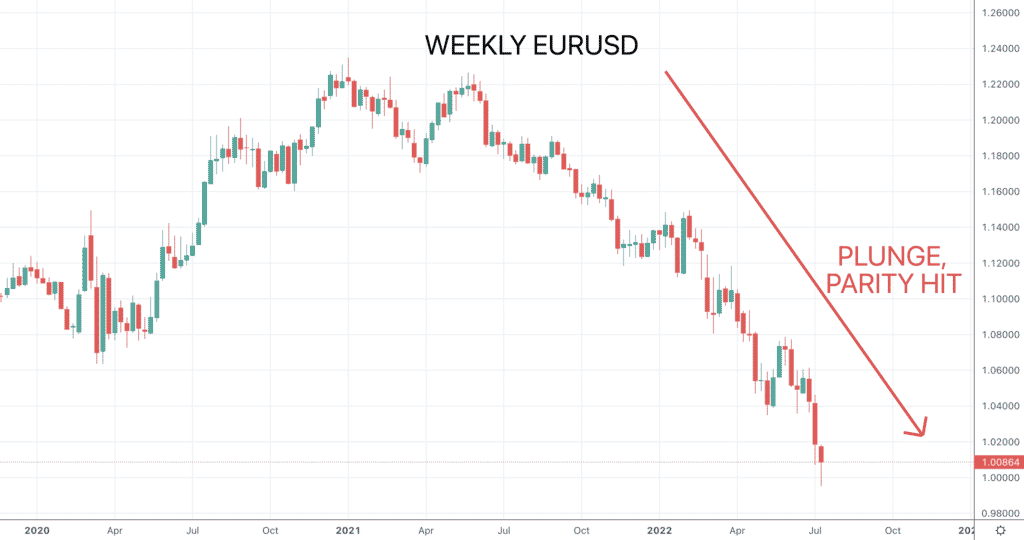

- EURUSD broke below the much-watched level of parity and then bounced, but remains vulnerable

- Gold plunged again and stays bearish.

- Oil was erratic once more last week, initially lower then rebounding, but with bigger risks skewed lower.

- Copper plunged even lower and stays negative.

Key this week

- Geopolitical focus: Still monitoring the war in Ukraine.

- Central Bank Watch: We get the Reserve Bank of Australia (RBA) Meeting Minutes Tuesday, the Peoples Bank of China interest rate decision on Wednesday and both the Bank of Japan (BoJ) and the European Central Bank (ECB) interest rate decisions, statements and press conferences on Thursday.

- Macroeconomic data: On the data front, the UK Employment report is released Tuesday, we get inflation reports from the EU Tuesday and from both the UK and Canada on Wednesday. Key data for the week will be the global Flash PMI data from S&P Global.

- Microeconomic data: US earnings season gets into full swing with Bank of America, IBM, Goldman Sachs, J&J, Netflix, Tesla and Twitter all reporting in the coming week.

| Date | Key Macroeconomic Events |

| 18/07/22 | Nothing of note |

| 19/07/22 | RBA Meeting Minutes; UK Employment report; EU inflation report |

| 20/07/22 | PBoC interest rate decision; UK inflation report; Canadian inflation report |

| 21/07/22 | BoJ and ECB interest rate decisions, statements and press conferences |

| 22/07/22 | Global Flash PMI from S&P Global; UK Retail Sales; Canadian Retail Sales |