Macroeconomic/ geopolitical developments

- The financial markets have been less dominated by the Russian invasion of Ukraine, as a lack of any significant escalation has seen a further shift towards more of a “risk on” theme for global risky assets (notably stocks) since mid-March.

- This has also been assisted by hopes from the Ukraine/ Russia talks and also from reported setbacks suffered by Russian troops.

- Global commodity prices have been mixed over the past week but have to some extent resumed some upside price pressures after their downside corrections from mid-March.

- Markets are still concerned about inflationary pressures from tight labour markets and elevated commodity prices, pointing to a threat of stagflation.

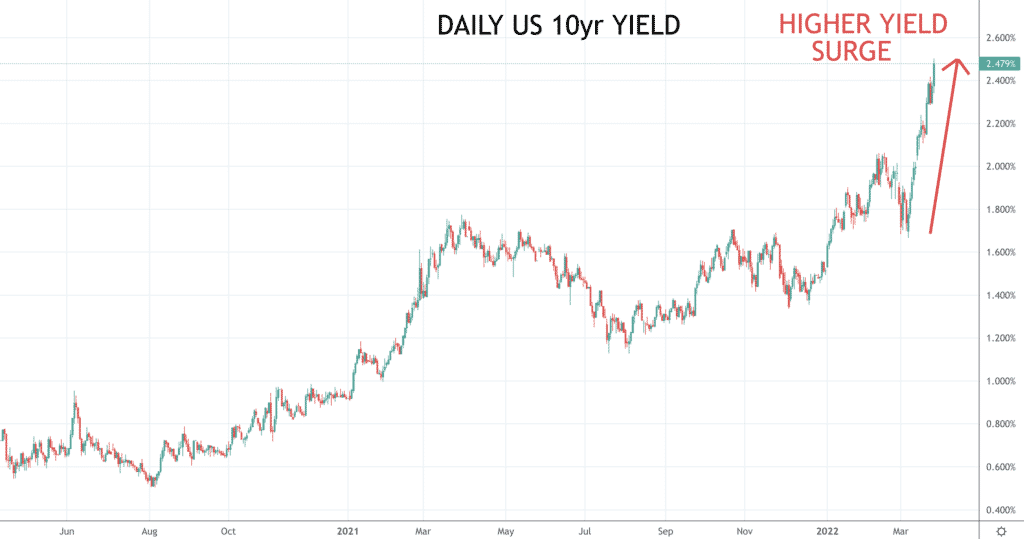

- A hawkish tone from Fed speakers (notably Chairmen Powell hinting at a 0.50% rate rise possibility) has been seen since the mid-March FOMC meeting that delivered a 0.25% interest rate rise, which has kept US and global bonds markets in bear mode, pushing yields higher.

- US President Joe Biden was on a tour of Europe and met with NATO, the EU and G7, and again delivered a strong message to Putin, with sanctions on Russia tightened and with the US agreeing a further 15 billion cubic meters of liquified natural gas in 2022, in order to of reduce the EU’s dependence on Russia.

- The important global data was mixed last week, but showing still positive signs, despite the conflict in Ukraine, and although US Durable Goods Orders missed expectations, the global Markit Flash PMI data were overall higher than expected.

- UK inflation hit a 30-year high in February, as CPI rose at a 6.2% annual rate, above market consensus.

- In the U.K., the Spring Statement provided little that was not expected, with modest cuts in national insurance contributions and fuel duty.

Global financial market developments

- Global stock averages were mostly higher last week with US markets being led higher by the tech sector and again positing strong closes on Friday.

- US and global bonds contoured their sell offs to higher yields with a more hawkish tone from Powell and ongoing fears of inflation and even stagflation.

- The US Dollar has been mixed – sideways versus the Euro, surging against the Japanese Yen and notably lower versus the “risk/ commodity currencies” (the Australian, New Zealand and Canadian Dollars).

- Gold has rebounded after suffering notable losses through mid-March, to indicate a more positive tone, although we do not foresee a renewed bull them to aim at the recent multi-year high.

- Similarly, Oil has rebounded after notable losses through mid-March to signal a more positive tone, with risk for a renewed bull theme to aim at the recent multi-year high.

- A cautious probe higher for Copper last week after the rebound through mid-March, again to try to resume the early March, strong bullish breakout rally.

Key this week

- Geopolitical focus:

- Monitoring for a possible military escalation in Ukraine.

- Also closely watching for potential for Ukraine/ Russia talks to improve and maybe for a ceasefire.

- There is an OPEC+ Meeting on Thursday.

- Europe has switched to Daylight Saving Time, so the differential to the US is back to normal.

Central Bank Watch: A light week for Central Bank activity, we get Governor Bailey of the Bank of England speaking on Monday and some Fed speakers through the week.

- Macroeconomic data: The key data points for the week will be the release of US GDP and PCE data on Wednesday and Thursday, the US Employment report Friday and the Global Markit and US ISM PMI data also on Friday.

| Date | Key Macroeconomic Events |

| 28/03/22 | BoE Governor Bailey speaks |

| 29/03/22 | Australian Retail Sales |

| 30/03/22 | German CPI; US ADP Employment Change; US GDP and PCE |

| 31/03/22 | UK GDP; German Retail Sales and Unemployment; OPEC Meeting; US PCE |

| 01/04/22 | Global Markit and US ISM PMI; US Employment report |