Macroeconomic/ geopolitical developments

- US equities rebounded during the holiday shortened week, with the Dow Jones Industrial Average rising 1.97%, the Nasdaq gaining 2.12% and the S&P 500 advancing 1.76%, as weaker than expected employment data eased concerns over further Federal Reserve tightening. Investors now look ahead to the start of the second quarter earnings season and the release of the Federal Minutes.

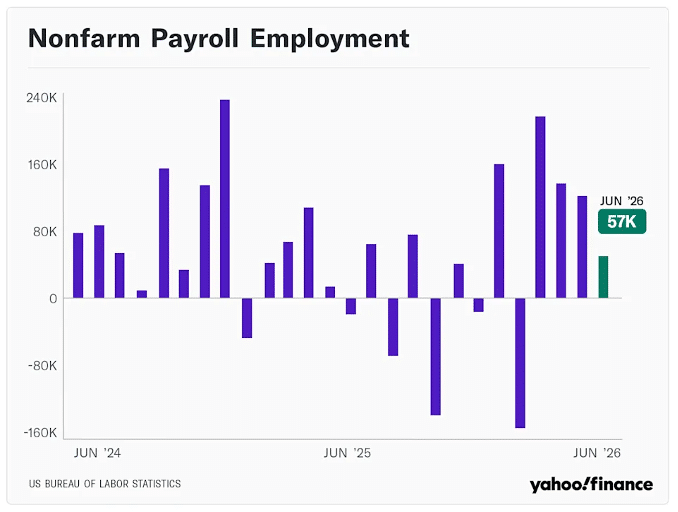

- US economic data weakened during the week as June’s Employment report showed slower than expected job creation and softer labor market momentum, while the ISM Manufacturing PMI also missed forecasts despite remaining in expansion. Attention now turns to Monday’s ISM Services PMI release, which will provide a further indication of the strength of US economic activity.

- Federal Reserve Chair Kevin Warsh reaffirmed the Fed’s commitment to returning inflation to its 2% target during the ECB’s Sintra conference, maintaining a hawkish stance while avoiding any guidance on the future path of interest rates. His remarks reinforced expectations that policymakers are likely to keep monetary policy restrictive until there is clearer evidence that inflation is moving sustainably lower.

- Investors’ attention will centre on Wednesday’s Federal Reserve Meeting Minutes for further insight into policymakers’ interest rate outlook, while Monday’s US ISM Services PMI will provide an important update on the strength of the US economy. The second quarter earnings season also begins this week, with results from Levi Strauss, PepsiCo and Delta Air Lines expected.

Global financial market developments

- US and global equity averages were mostly higher.

- US and European bond yields were higher on the week.

- The US Dollar Index moved lower on the week, down from a multi-month high.

- Gold futures were up for the week from a multi-month low.

- Oil futures prices nudged power to another multi-month low.

Key this week

Central Bank Watch: Attention this week will center on Wednesday’s release of the FOMC Meeting Minutes, which may provide further insight into the Federal Reserve’s policy outlook.

Macro Data Watch: The macroeconomic calendar is headlined by Monday’s US Services and Composite PMI releases, with investors also watching EU Retail Sales on Monday, China’s CPI data on Thursday, and Canada’s Employment Reports on Friday.

| Date | Major Macro Data |

| 07/06/2026 | German Factory Orders; EU Investor Confidence, PPI and Retail Sales; US Service and Composite PMI |

| 07/07/2026 | German Industrial Production; UK Financial Stability Report |

| 07/08/2026 | FOMC Minutes; Japanese Current Account |

| 07/09/2026 | Chinese CPI and PPI; German Trade Balance; US Initial Jobless Claims and Existing Home Sales Change |

| 07/10/2026 | German HICP and Canadian Employment Reports |