Macroeconomic/ geopolitical developments

- In a holiday-shortened week, the S&P 500 and Nasdaq Composite reached record highs, driven by growth shares and favourable interest rate expectations, while lighter trading volumes and a positive June employment report further boosted market optimism.

- The US ISM Service PMI fell in June, indicating a contraction and raising economic concerns, while European PMI data showed more stability, despite some manufacturing sector struggles.

- The Federal Reserve’s June meeting minutes indicated that while inflation is decreasing, it is not falling fast enough for rate cuts, with officials requiring more consistent data before lowering rates and maintaining a cautious stance amidst economic slowdown concerns and internal disagreements on policy adjustments.

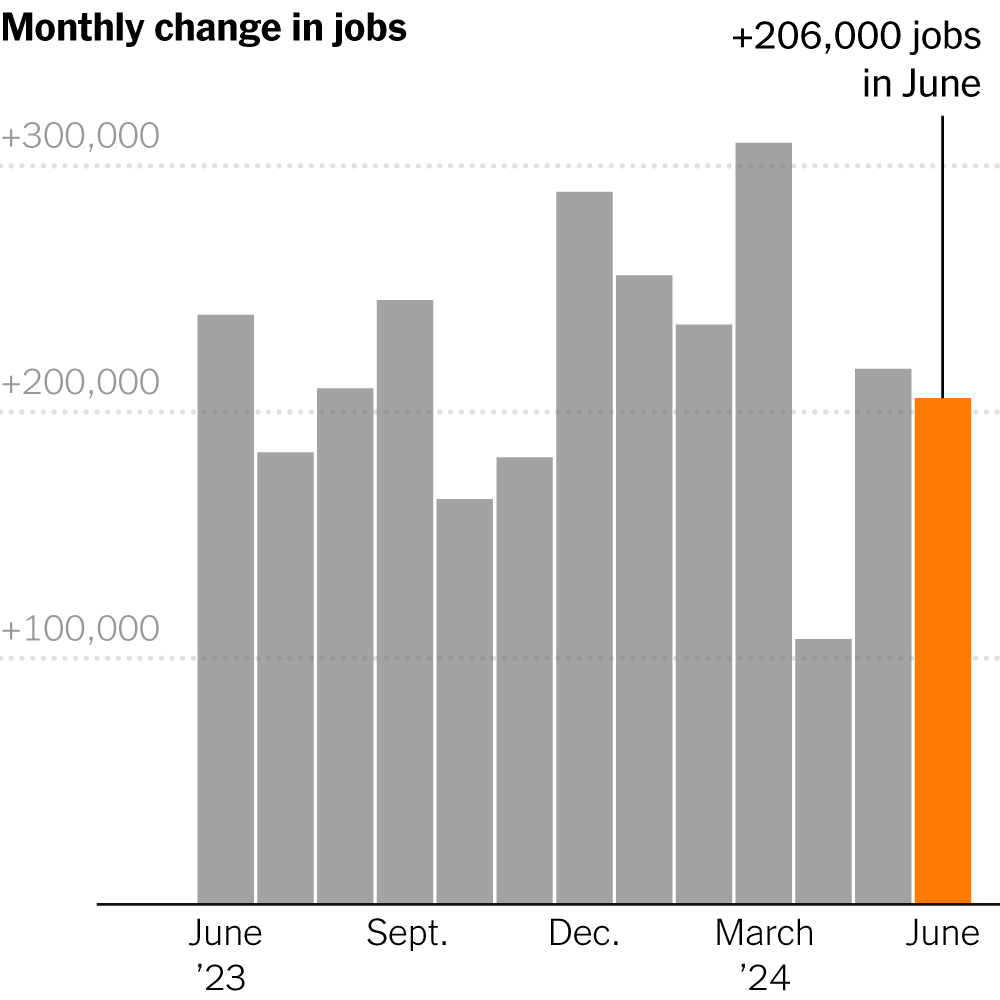

- June’s deceleration in U.S. job growth, with 206,000 positions added and the unemployment rate rising to 4.1%, prompted a drop in Treasury yields and modest gains in stocks, bolstering expectations for potential Federal Reserve rate cuts later this year.

- In the UK, Labour secured a significant parliamentary majority, ending the Conservatives’ 14-year rule, as Keir Starmer became the next prime minister, with Prime Minister Rishi Sunak conceding defeat and subsequently resigning as Conservative Party leader.

Global financial market developments

- US and global equity averages extended higher, with US indices at record levels

- US bond yields were notably lower on the week

- The US Dollar Index sold off with the lower US yields.

- Gold futures rallied, with the weaker US Dollar.

- Oil futures nudged higher to multi-week highs.

Key this week

Central Bank Watch: Fed Chair Powell testifies to Congress on Tuesday. The only other central bank activity of note is the Reserve Bank of New Zealand Interest Rate Decision and Monetary Policy Statement on Wednesday.

Macro Data Watch: The main macro data release this week is the US CPI data on Thursday. Other releases of note are the Chinese CPI data on Wednesday, UK GDP data and German CPI data on Thursday, then US PPI data on Friday.

| Date | Major Macro Data |

| 07/08/2024 | Nothing of note |

| 07/09/2024 | Fed Chair Powell testifies; UK Retail Sales |

| 07/10/2024 | Chinese CPI; RBNZ Interest Rate Decision and Monetary Policy Statement |

| 07/11/2024 | German CPI; UK GDP; US CPI |

| 07/12/2024 | German Retail Sales; US PPI; Michigan Consumer Sentiment Index |